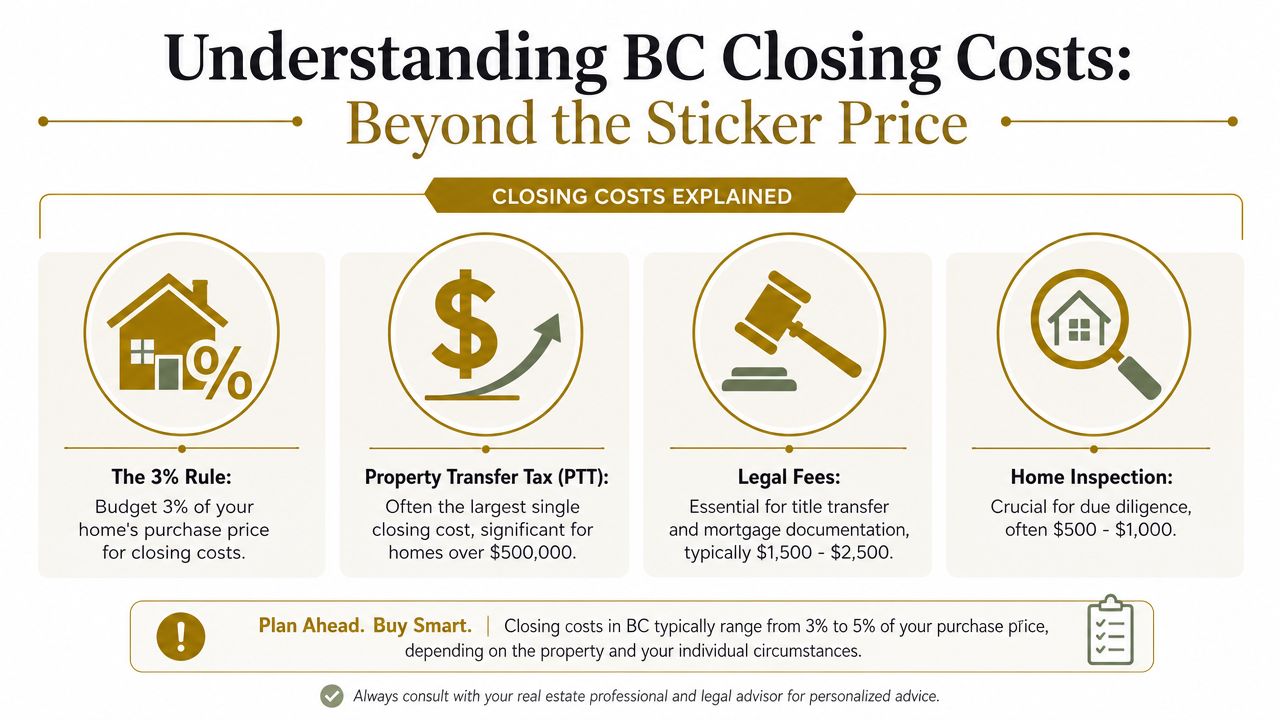

In BC, buyers should budget 3% to 5% of the purchase price for closing costs, not the lower figure people often see in generic Canadian guides, and for a $900,000 home that can mean $18,000 to $35,000 in cash before move-in. In Maple Ridge, where prices often sit near or above the current exemption cutoffs, that gap matters a lot more than most first-time buyers expect.

A common version of this starts with a good day. You find a townhome near Kanaka Creek or a detached place in Cottonwood with enough yard for the dog, a short drive to school drop-off, and easy access to Golden Ears Way for the morning commute. Your mortgage pre-approval is in place, your down payment is saved, and then someone says, “Don't forget closing costs.”

That's usually the moment the mood changes.

Closing costs are the extra expenses you pay to complete the purchase. They're separate from your down payment. Some are taxes. Some are legal and administrative. Some are adjustments between buyer and seller. In BC, the biggest surprise is that these costs are often much higher than buyers expect, especially if they've been reading broad national articles that don't reflect how purchases work in Maple Ridge, Albion, Silver Valley, West Maple Ridge, or Pitt Meadows.

If you're researching closing costs when buying a home in BC, the most useful thing you can do is stop thinking in rough national averages and start looking at the actual local numbers that apply on completion day. That's where good planning saves stress.

The Reality of Closing Costs When Buying in Maple Ridge

A buyer finds a family home in Cottonwood. The layout works, the backyard is big enough for a play set, and the school run feels manageable. After a weekend of second-guessing, they write the offer, negotiate subjects, and start picturing furniture in the living room. Then the lawyer or notary sends over the estimate.

That's when closing costs stop being an abstract phrase and start feeling very real.

What buyers usually mean when they ask about closing costs

In plain language, closing costs are the cash expenses tied to finalising the purchase. They show up after your offer is accepted and before you get the keys. They aren't part of the price you negotiate for the home itself.

For first-time buyers, that distinction is where the confusion starts. Buyers often spend so much energy getting pre-approved and building the down payment that they treat the rest like a small side bill. In Maple Ridge, it usually isn't small.

You can afford the monthly payment and still get caught short on completion day if you haven't set aside separate cash for the closing statement.

Why the timing matters as much as the amount

The hard part isn't just the total. It's when these costs are due. Most of them need to be paid in cash through your lawyer or notary as the deal closes, which means your budget has to be organised before moving week starts.

That timing becomes even more important when dates are tight. If you're coordinating financing, subject removal, possession, and moving trucks, a practical guide on managing home closing timelines can help you think through the sequence before little details turn into last-minute pressure.

Buyers in Maple Ridge also deal with neighbourhood-specific trade-offs that don't show up in generic advice. A newer townhome in Albion may come with strata-related items to review. A detached home in Hammond or West Maple Ridge may raise more inspection questions. A newer build near Silver Valley can bring a different tax conversation than an older resale house. If you're still early in the process, this local guide to buying a home in Maple Ridge is a useful next step.

Why BC Closing Costs Are Higher Than You Think

In BC, closing costs aren't a rounding error. They're a serious part of the cash you need to buy.

The number I want buyers to remember is simple: budget 3% to 5% of the purchase price. That guidance is especially important because many buyers come across articles from elsewhere in Canada using much lower averages and assume the same math applies here. It often doesn't.

The BC rule of thumb that actually fits local buyers

According to this BC closing cost breakdown, buyer closing costs in British Columbia typically range from 3% to 5% of the purchase price, which is significantly higher than the 1.5% average often cited elsewhere in Canada. The same source notes that for a $900,000 home, closing costs excluding down payment and mortgage default insurance range from $18,000 to $35,000, with PTT alone at $16,000, paid in cash on completion and not added to the mortgage.

That last point is what catches people. Buyers tend to focus on what the lender will finance. Closing costs are the money the lender usually won't cover in the same way.

Why generic calculators cause problems in Maple Ridge

A national calculator may be fine for broad education. It's not enough for a buyer comparing homes in Maple Ridge, Pitt Meadows, or the Fraser Valley where price points often sit in the range where BC taxes hit hard.

Here's what works better:

- Start with the local price, not a national average: A condo near downtown Maple Ridge and a detached home in Kanaka Creek can create very different closing-day cash needs.

- Separate mortgage affordability from cash-to-close: Your lender may confirm the payment works. That doesn't mean your completion funds are fully covered.

- Expect BC-specific taxes to drive the number: This is why local advice matters more than a broad “Canada-wide” estimate.

If you've also been trying to sort out BC tax rules that buyers hear about online, this plain-language article on the foreign buyers tax in BC helps clear up one of the more commonly misunderstood topics.

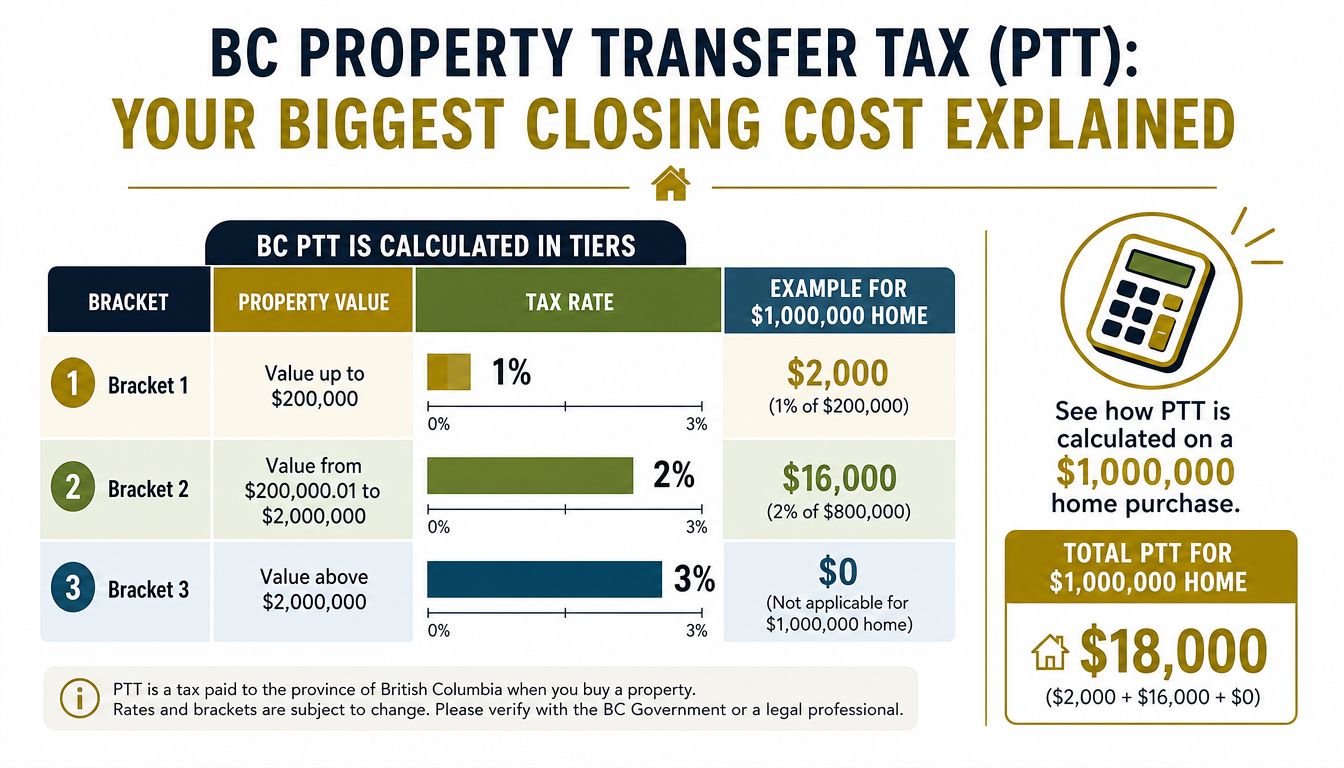

Property Transfer Tax Explained Your Single Biggest Cost

A lot of first-time buyers in Maple Ridge feel comfortable right up until we run the closing numbers. Then PTT shows up, and the budget changes fast.

If there is one closing cost that deserves its own conversation in BC, it is Property Transfer Tax, or PTT. In many Maple Ridge purchases, it is the largest cash expense after the down payment, and it has to be planned for early.

How PTT is calculated in BC

BC charges PTT in brackets. The province applies 1% on the first $200,000 of the purchase price and 2% on the portion from $200,000 to $2,000,000. The calculation is straightforward once you break it into pieces.

For example, on a home at $860,000, the tax works out like this:

- 1% of the first $200,000 = $2,000

- 2% of the remaining $660,000 = $13,200

- Total PTT = $15,200

That is the part generic advice often misses. Buyers hear “land transfer tax” and assume it is a small line item. In Maple Ridge, where many purchase prices sit well above the first bracket, the number gets large quickly. The Province of British Columbia explains the tax rates, exemptions, and filing rules on its Property transfer tax page.

The 2024 exemption change matters more in Maple Ridge than many buyers realize

The 2024 update to the BC first-time home buyers program changed the math for some entry-level buyers. Full relief may be available on qualifying homes with a fair market value up to $835,000, with a partial exemption above that threshold up to $860,000, based on the provincial rules outlined by BC.

That matters here because Maple Ridge often sits right around those price points. A buyer at $825,000 may qualify for a very different result than a buyer at $865,000, even though the monthly payment might look similar on paper. In practice, a small jump in price can mean a sharp jump in cash needed on completion.

That is one reason I tell buyers not to shop right to their approval limit without checking the tax consequences first.

What that means in real life

PTT is usually paid at closing through your lawyer or notary. It is a required part of completing the transfer, and buyers should not assume it will roll into the mortgage by default.

This is also where local strategy matters. If you are choosing between two similar Maple Ridge homes, one priced inside an exemption threshold and one just above it, the lower-priced option may leave you in a stronger cash position after closing. That can matter more than buyers expect, especially if the property also needs paint, flooring, or immediate repairs.

For buyers who want a plain-language overview of the concept itself, this article on what a land transfer tax is gives useful background.

A short explainer video can help if you prefer to see the concept visually:

One practical tip. Ask your conveyancer for a draft statement before completion if you want fewer surprises. Services such as Automated title document checking can also help buyers review title-related paperwork more carefully before funds are due.

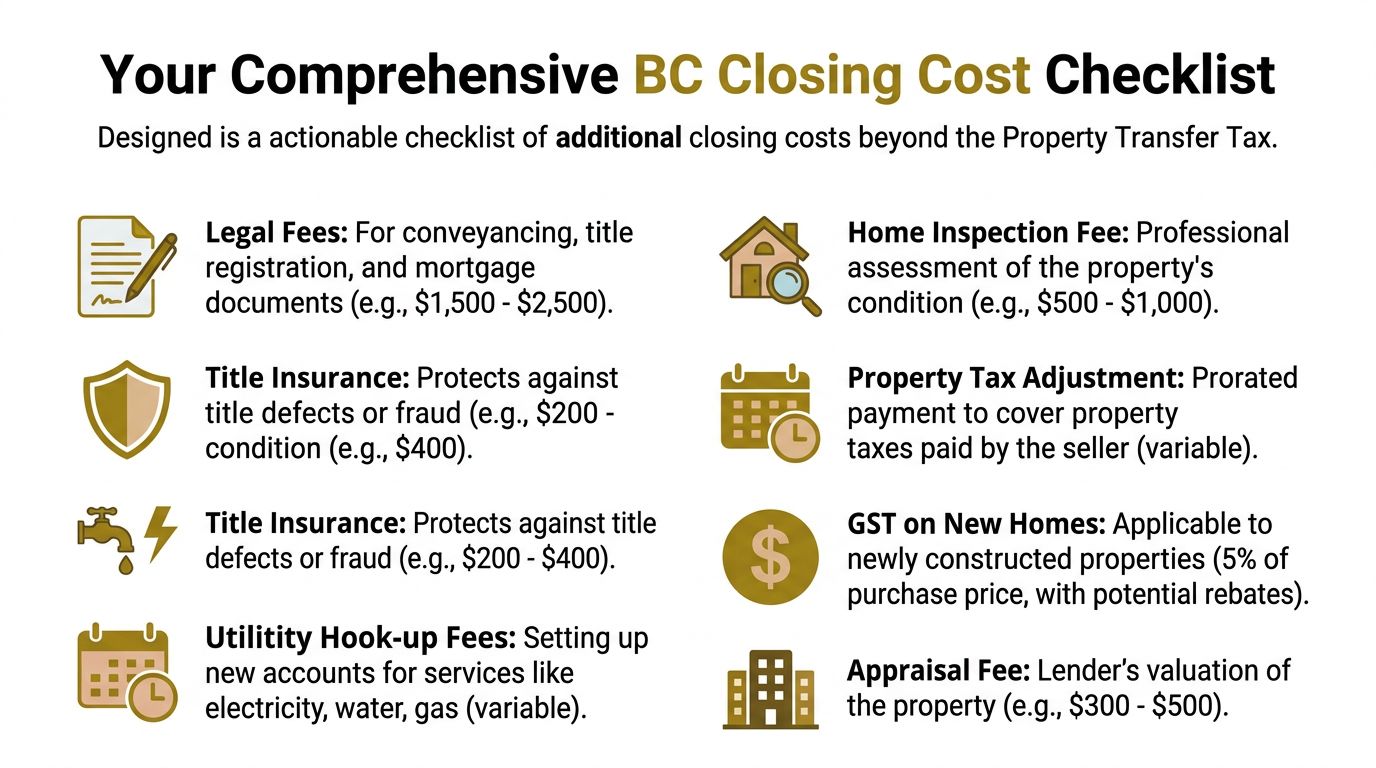

The Complete Checklist of Other BC Closing Costs

A lot of Maple Ridge buyers get past the down payment and PTT, then find out there are still several smaller charges stacked on top at the last minute. That is usually the point where the budget starts to feel tighter than expected.

These costs are not usually as large as Property Transfer Tax, but they arrive at the same time and they are paid in cash. On an older detached home in Hammond, Silver Valley, or West Maple Ridge, I often tell buyers to leave more room than they think they need. Legal work, inspections, lender-related charges, and building-specific fees can add up quickly, especially if the home also needs immediate work after possession.

The line items most buyers should expect

The exact total depends on the property type, the lender, and whether you are buying resale or new construction. In Maple Ridge, these are the items I tell buyers to check early:

- Legal fees and disbursements: Your lawyer or notary handles the conveyance, title transfer, mortgage registration, and closing documents. The BC Financial Services Authority explains that legal fees and disbursements are a standard part of closing costs for buyers in the province, and final pricing varies by transaction and provider. See the BCFSA home buying cost overview here: https://www.bcfsa.ca/public-resources/real-estate/home-buying-closing-costs.

- Home inspection: On detached homes, especially older Maple Ridge properties with original roofs, aging drains, or deferred maintenance, an inspection is often money well spent before subject removal. Consumer Protection BC outlines what home inspectors do and why buyers use them during due diligence: https://www.consumerprotectionbc.ca/consumer-help/home-inspections/.

- Strata move-in or document fees: Condo and townhouse buyers should review the strata documents carefully. Some buildings charge move-in fees, elevator booking fees, or administrative charges, and those costs can vary from one complex to another. The Condominium Home Owners Association of BC has a useful plain-language guide to common strata costs and documents: https://choa.bc.ca/owners/understanding-stratas/.

- Lender appraisal fee: Some lenders require an appraisal, particularly with insured mortgages, private financing, or unusual properties.

- Adjustments: Property taxes, strata fees, and some utility-related items may be prorated between buyer and seller based on the completion date. The exact amount depends on what has already been paid.

One cash cost first-time buyers regularly miss

If your down payment is under 20%, mortgage default insurance usually applies. Buyers often know the premium exists. What they miss is that the sales tax on that premium is typically paid upfront and cannot be added to the mortgage balance.

That matters in Maple Ridge entry-level purchases, where buyers are already stretching to cover the down payment, deposit, and moving costs. A lender or broker can usually estimate your cash to close early in the process. Ask for that number well before you remove subjects, not just the projected monthly payment.

New construction needs a separate check

New builds need extra attention because GST can change the math in a hurry. The Canada Revenue Agency sets out the rules for GST on newly built homes, including when a rebate may apply and when it may not: https://www.canada.ca/en/revenue-agency/services/forms-publications/publications/rc4028/gst-hst-new-housing-rebate.html.

That is one area where BC-wide articles can be too general. In Maple Ridge, buyers comparing a resale townhome with a new-build unit in the same price band can see a very different cash requirement at closing, even before they get into appliances, blinds, or upgrade costs. The 2024 PTT exemption changes helped some buyers on qualifying homes, but they did not remove GST on new construction. Buyers still need to run the full numbers.

Before closing, it also helps to review title and conveyancing paperwork carefully. If you want another layer of review on dense documents, Automated title document checking is one option buyers can use before signing.

If you want a quick estimate before you talk to your lawyer, this BC closing costs calculator for buyers is a practical starting point.

Decoding Your Statement of Adjustments

The Statement of Adjustments sounds more intimidating than it is. In practice, it's just a fairness document.

The easiest way to think about it is like settling shared household bills when one person moves out and another moves in. If the seller already paid for something that covers time after the closing date, you reimburse their share. If not, you don't.

What usually appears on it

In Maple Ridge purchases, the most common adjustments are:

- Property taxes: If the seller prepaid taxes beyond the completion date, the buyer reimburses the seller for the portion that belongs to the buyer's period of ownership.

- Strata fees: For condos and townhomes, monthly strata payments are often split based on the closing date.

- Utilities or municipal charges: Depending on the property and what has been prepaid, there may be smaller prorated items.

These aren't surprise fees in the same sense as taxes or legal costs. They're accounting entries that make sure both sides pay their fair share for the period they owned the property.

Why buyers sometimes misread this document

Buyers often see a larger total on the closing statement and assume every line is a new charge. It usually isn't. Some entries are reimbursements to the seller because they paid ahead.

That's why I tell buyers to read the statement in two passes. First, identify the true costs of buying. Then look at the adjustments separately. Once you split those two categories in your mind, the statement becomes much easier to understand.

If a seller prepaid something that benefits you after completion, reimbursing them isn't a penalty. It's the bookkeeping that keeps the closing fair.

If you've ever wondered who pays what in the broader transaction, this article on who pays realtor fees helps clear up another part of the cost conversation that buyers and sellers often mix together.

Putting It All Together A Maple Ridge Closing Cost Scenario

A Maple Ridge buyer usually feels the pinch on closing day, not when they first run the mortgage payment.

Take a first-time buyer purchasing a $950,000 townhome in Silver Valley. This is a common local step-up choice. You get family-friendly space, newer strata stock, and easier access to parks and trail networks than many buyers can find closer to Vancouver. The catch is that the cash needed to complete is often higher than expected, especially once Property Transfer Tax is added back into the picture.

At $950,000, this example sits above the current first-time buyer exemption range. That matters. Under BC's Property Transfer Tax rates published by the province, the tax on a $950,000 purchase works out to $17,000. The formula is 1% on the first $200,000 and 2% on the remaining $750,000, as set out by the BC Government Property Transfer Tax overview.

For Maple Ridge buyers, the 2024 rule changes matter in real life. A lot of broad BC articles stop at the old threshold discussion, but in local price bands like Silver Valley, Albion, and parts of Cottonwood, a home can land just above the exemption cutoffs and change the cash requirement by thousands. I see buyers focus hard on the monthly payment, then realize their closing funds need a second look.

Here is a practical budget for this scenario:

| Cost item | Maple Ridge scenario |

|---|---|

| Purchase price | $950,000 |

| Property Transfer Tax | $17,000 |

| Legal fees and disbursements | $1,000 to $2,000 |

| Home inspection | $400 to $800 |

| Strata move-in fee | $150 to $300 |

| Adjustments for taxes or strata | Varies by completion date and seller prepayments |

That table does two jobs. It gives you a realistic cash target, and it shows which numbers are fixed versus which ones still need to be confirmed by your lawyer or notary.

The trade-off with a townhome is straightforward. The purchase price may be more manageable than a detached home in West Maple Ridge, but you still need to budget for strata-related items and any prorated reimbursements on completion. If the seller has prepaid property taxes or strata fees, those amounts can push the final funds required a bit higher than buyers expect.

This is why I tell first-time buyers to separate closing money from everything else early. Keep it in its own account. Don't mix it with your down payment buffer, furniture budget, or post-move emergency fund. That one habit prevents a lot of last-minute stress when your lawyer sends the final amount needed to close.

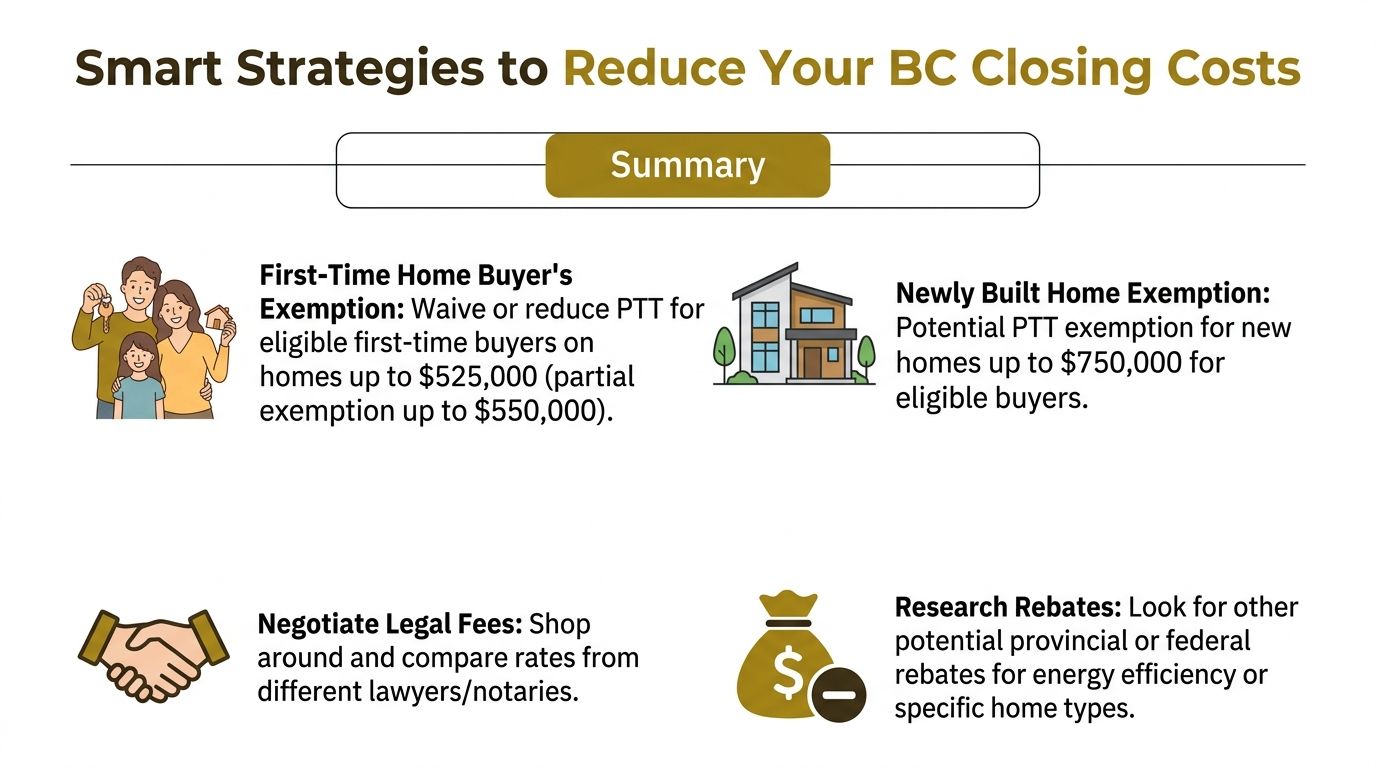

How to Reduce Your Closing Costs in 2026

A buyer in Maple Ridge finds a place that feels right, gets pre-approved, and then hits the last question that catches people off guard. How much cash is needed on closing day?

That answer often comes down to planning before the offer, not after accepted subjects.

The biggest place to look for savings

The first place I look is Property Transfer Tax. The April 1, 2024 rule changes matter here more than many buyers realize, because Maple Ridge prices often sit near the updated first-time buyer exemption cutoffs. A home that falls on one side of that line can require thousands less in cash than a similar home a street or two away.

BC has outlined the current first-time home buyers' exemption rules and thresholds on the provincial website: Property transfer tax exemptions for first time home buyers. If you are shopping near those limits, confirm the tax result before you write, not after you have mentally committed to the home.

That is especially relevant in Maple Ridge. Buyers looking at entry-level detached homes, newer condos, or townhomes in areas like Albion, Cottonwood, and parts of Silver Valley can end up very close to the price points where the exemption changes.

What tends to work

- Check your exemption status early: First-time buyer rules, residency requirements, and price thresholds need to be confirmed before you set your search range.

- Shop with an after-closing number in mind: Do not stop at down payment and monthly payment. Ask your lender, lawyer, or realtor for a realistic cash-to-close estimate tied to the homes you are viewing in Maple Ridge.

- Compare legal quotes properly: A low headline fee is not enough. Ask what is included, what disbursements are extra, and whether bank fees, title charges, and registration costs are estimated clearly.

- Keep closing funds separate from the rest of your savings: Buyers who park this money in a separate account are less likely to chip away at it for movers, furniture, or repairs right before completion.

- Review strata documents for added charges: In condos and townhomes, move-in fees, document costs, and prepaid strata amounts can change the final number.

Where buyers lose money

The expensive mistakes are usually ordinary ones. Using an old blog post with outdated PTT thresholds. Assuming a national closing-cost estimate applies cleanly in BC. Writing an offer at the top of the budget without checking how the tax treatment changes at that purchase price.

I also see buyers underestimate adjustments. If the seller has already paid property taxes, utilities, or strata fees, you may need to reimburse the seller for the unused portion. That is normal, but it still affects how much your lawyer asks you to send before completion.

The cheapest way to handle closing costs is to price them out early and leave yourself room.

If you're buying or selling in Maple Ridge or Pitt Meadows and want help working through the numbers before you write an offer, Royal LePage Brookside Realty Property Management can help you map out the local costs, neighbourhood trade-offs, and timing so there are fewer surprises on closing day.