If you’re considering buying a home in certain parts of British Columbia, you’ve likely heard whispers about the foreign buyers tax. So, what exactly is it? In simple terms, it's a 20% additional property transfer tax that applies to foreign nationals, foreign corporations, or taxable trustees who are purchasing residential real estate in specific areas of BC, including the Vancouver area and the Fraser Valley.

This tax is paid on top of the general property transfer tax everyone pays. It was introduced by the provincial government as a way to help cool down the red-hot housing markets in high-demand areas and improve affordability for local residents.

Understanding The Foreign Buyers Tax

It’s best to think of the foreign buyers tax not as a separate fee, but as an extra layer added to the usual closing costs when buying a home in places like Metro Vancouver or the Fraser Valley. Officially, it’s called the Additional Property Transfer Tax, and its creation was a direct response to the sky-high home prices that were becoming the norm. The main goal was to slow down demand from international investors and bring some stability back to the local market.

The tax specifically targets residential property purchases made by individuals or companies that the province considers "foreign." This includes:

- Foreign Nationals: Anyone who is not a Canadian citizen or a permanent resident of Canada.

- Foreign Corporations: Companies that are not incorporated in Canada or are controlled by foreign individuals or entities.

- Taxable Trustees: This applies to a trust where at least one of the beneficiaries is a foreign national or a foreign corporation.

The Purpose Behind the Tax

The government didn't just create this tax out of thin air. It was a major policy move aimed squarely at the housing affordability crisis. In the years before the tax was introduced, places like Vancouver and the surrounding Fraser Valley experienced explosive price growth, driven in part by a surge of global investment.

In fact, a 2022 report from the Business Council of British Columbia confirmed that Metro Vancouver is still one of North America's least affordable places to buy a home. The tax was one of several tools designed to give local buyers a fighting chance in a competitive market.

The Additional Property Transfer Tax is fundamentally a demand-side measure. By making it more expensive for non-residents to purchase property, the policy aims to curb external demand and cool an overheated market, creating more stability for local buyers.

How It Impacts Your Purchase

For an international buyer, this tax has a huge and direct impact on the final cost of a property. It's calculated based on the fair market value of the home. To put it in perspective, on a $1,000,000 property, the foreign buyers tax adds an extra $200,000 to your closing costs. That's a serious number.

Trying to navigate this complex tax landscape on your own can be daunting. This is where working with experienced real estate professionals like James and Nicole Isherwood makes all the difference. Their deep knowledge of the Vancouver and Fraser Valley markets means they can help you understand all your obligations, and just as importantly, see if you qualify for any potential exemptions right from the start. Understanding the complete process of buying a home in BC is the first step toward a successful transaction.

Where The Foreign Buyers Tax Applies in BC

First things first: the foreign buyers tax doesn't apply everywhere in British Columbia. This is a common misconception. The tax was strategically rolled out in specific high-demand real estate markets to help cool things down and improve housing affordability for locals.

So, if you're looking at property in the Vancouver area or Fraser Valley, your very first step is to confirm whether the home falls within one of these designated zones. Getting this wrong can be a very expensive mistake.

Key Taxable Regions

The government has zeroed in on several key regional districts, which basically cover the province's most populated and sought-after metropolitan areas. You'll want to pay close attention if your dream home is in any of these spots.

Below is a quick-reference table outlining the major regional districts where the 20% tax is in effect.

Regions Subject to the BC Foreign Buyers Tax

This table covers the big ones, but it’s always best to verify the exact municipality. A property might feel like it’s part of a major city but could technically fall just outside the official boundary of a taxable regional district. That small difference can completely change the financial outcome of your purchase.

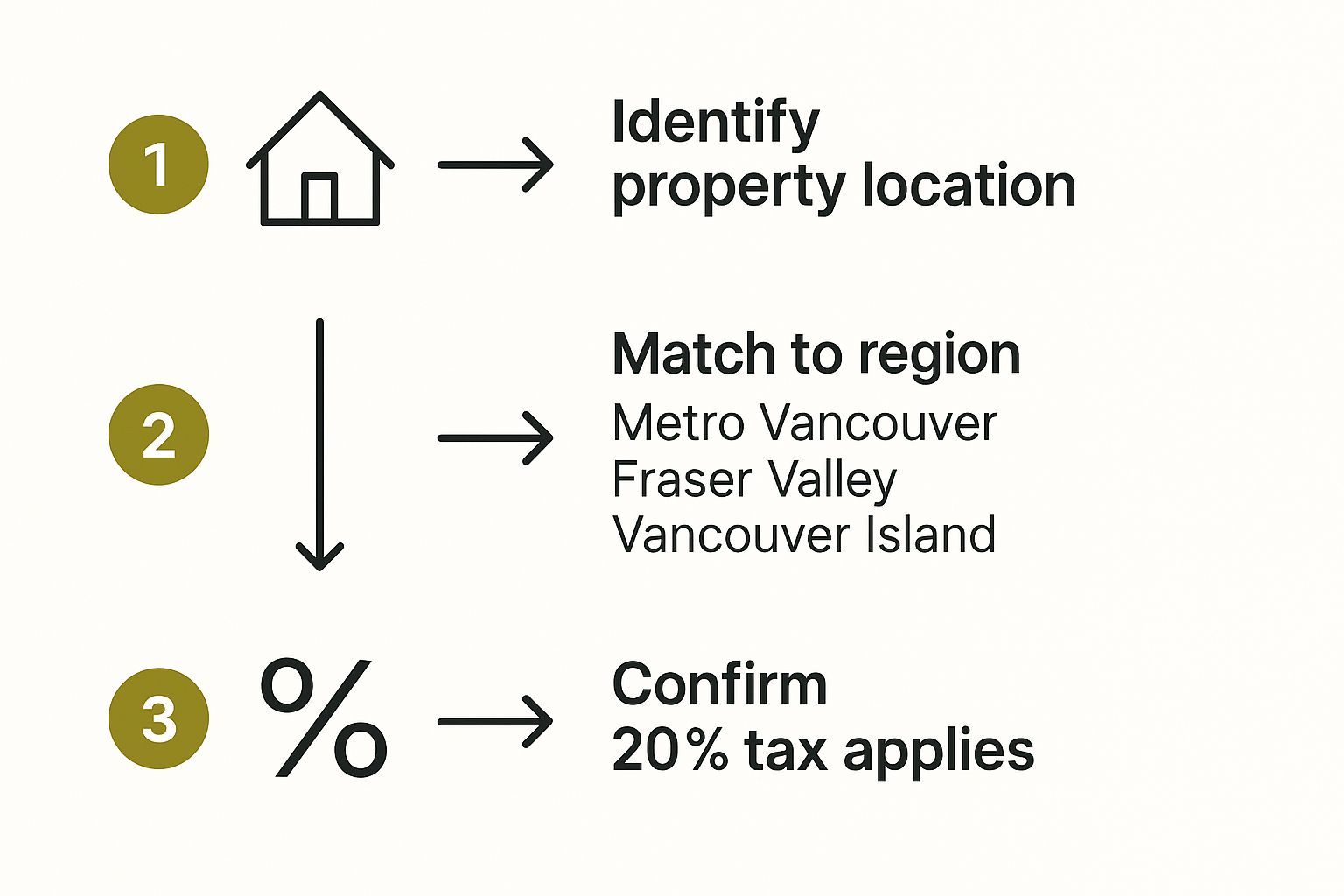

This infographic breaks down the simple process for figuring out if a property you're interested in is subject to the tax.

As you can see, it's a straightforward three-step check: pinpoint the property's location, see if it's inside a designated regional district, and then confirm the 20% tax applies. Following this simple framework helps avoid any nasty surprises when it comes time to close the deal.

Navigating these boundaries really requires local expertise. Real estate agents who live and breathe the Vancouver and Fraser Valley markets, like James and Nicole Isherwood, can give you precise, on-the-ground guidance about whether a specific property is affected. For more local real estate insights, feel free to check out our official news page.

How To Calculate The Total Tax On A Property

Alright, let's get down to the numbers. Understanding how the foreign buyers tax is actually calculated is the key to budgeting properly for your property purchase in the Fraser Valley. It's not just one flat fee; the total tax you’ll pay is a combination of two separate amounts: the standard Property Transfer Tax (PTT) that every buyer pays, plus the Additional Property Transfer Tax, which is the foreign buyers tax itself.

Let's walk through a clear, real-world example. Imagine you’re a foreign buyer looking at a home with a fair market value of $1,500,000. We’ll figure out the tax in two simple stages.

Stage 1: Calculating The Standard Property Transfer Tax

First up is the general PTT. This tax is tiered, meaning different rates apply to different chunks of the property's value. Think of it like income tax brackets, but for a home purchase. It's important to remember this is separate from any real estate agent commissions, which are typically structured as 7% on the first $100,000.00 and 3.5% on the balance.

Here’s how the general PTT breaks down for our $1,500,000 example:

- 1% on the first $200,000 = $2,000

- 2% on the portion from $200,000 up to $2,000,000 (in this case, $1,300,000) = $26,000

- 3% on the portion over $2,000,000 (which is $0 here) = $0

Add those up, and the standard Property Transfer Tax on this home comes to $28,000.

Stage 2: Calculating The Foreign Buyers Tax

Now for the second piece of the puzzle: the Additional Property Transfer Tax. This part is much simpler. It’s a flat 20% of the property's fair market value. No tiers, no brackets, just a straight percentage.

For our $1,500,000 property, the math is straightforward: $1,500,000 x 20% = $300,000. This $300,000 is the foreign buyers tax you have to pay on top of the standard PTT.

Finally, to get your grand total for taxes due at closing, you just add the two figures together.

- Standard Property Transfer Tax: $28,000

- Additional Property Transfer Tax: $300,000

Total Tax Due = $328,000

This example really shows how quickly the costs can stack up, turning a $1.5 million purchase into a much larger financial commitment. To get a better handle on your total monthly costs, our handy mortgage payment calculator can give you a more detailed breakdown.

Beyond this one tax, understanding the bigger picture of managing investment property tax effectively is essential for any owner. The complexity here is exactly why having an experienced real estate professional on your side is so valuable.

Qualifying for a Tax Exemption

That 20% tax figure can feel pretty daunting, almost like an unavoidable cost of buying a home in the Fraser Valley if you're not a Canadian citizen. But it’s not always a closed case. The provincial government has carved out specific pathways for certain individuals to get out of paying this tax, which can completely change the financial picture of your purchase.

These exemptions aren’t random loopholes. They’re designed for people who are genuinely putting down roots in British Columbia. Instead of penalizing those with concrete plans to live and work here, the rules offer a break to those on a clear path to becoming permanent residents. Knowing your options here is absolutely critical for smart financial planning.

The most common way to get an upfront exemption is through the BC Provincial Nominee Program (BC PNP). This program is a major immigration stream for skilled workers and entrepreneurs whose expertise is needed in our local economy.

The BC Provincial Nominee Program Exemption

If you’re a confirmed BC Provincial Nominee when you buy your home, you might not have to pay the foreign buyers tax at all. But just being in the program isn't enough—you need to tick a few specific boxes to qualify for this immediate relief.

To be eligible, you have to meet all of these conditions:

- You must be a confirmed BC Provincial Nominee on or before the day the property transfer is officially registered.

- The property you're buying must be your principal residence.

- The property must be transferred to you as an individual, not a corporation.

This exemption is a huge financial advantage, letting you sidestep that 20% tax payment right at the time of purchase. It directly links your commitment to making BC your home with your real estate investment. Of course, with ownership comes responsibilities; our guide on landlord resources is a great place to start learning about your obligations.

Claiming a Refund After Purchase

So, what happens if you buy your home before you're a BC PNP nominee, but you become a permanent resident soon after? The government has a plan for that exact situation. You can actually apply for a full refund of the tax you paid, as long as you meet certain criteria within your first year of ownership.

This refund mechanism is a game-changer for many newcomers. It means that even if you pay the tax initially, your long-term immigration plans can lead to a full reimbursement, effectively erasing that initial cost.

To get your money back, you must:

- Become a Canadian citizen or a permanent resident of Canada within one year of the property's registration date.

- Move into the home and live in it as your principal residence for the rest of that first year.

The deadline is strict. You have to apply for the refund after the one-year anniversary of the registration date but before 18 months have passed. On top of these specific exemptions, it's also worth understanding the broader property investment tax deductions that could lower your overall tax burden.

Navigating these rules takes careful timing and paperwork, which is why getting advice from experts like James and Nicole Isherwood is so valuable. They can help you make sure your property purchase timeline lines up perfectly with your immigration journey.

How Do You Actually File and Pay the Tax?

So, how does this all work in practice? The good news is, you won’t be navigating the administrative side of the foreign buyers tax on your own. This isn’t something you handle directly. Instead, it’s a critical step managed by your legal team—your lawyer or notary public—during the final stages of your property purchase.

It all happens at the moment of truth: when your legal representative registers the property title in your name. This is the official transfer of ownership, and it’s precisely when all associated taxes, including the foreign buyers tax, must be settled. The entire process is baked right into the closing paperwork you'll be signing.

The Key Document: The Property Transfer Tax Return

The central piece of this puzzle is a form called the Property Transfer Tax (PTT) Return. Think of it as the main declaration for the provincial government, recording all the crucial details about the transaction. It's not just for the standard tax; it’s where your status as a foreign buyer is officially put on the record.

On this form, your lawyer will fill out a section indicating whether you are a foreign national or a taxable trustee. This single declaration is what triggers the application of the 20% additional tax. It’s a mandatory part of registering any residential property in the designated taxable regions.

The Property Transfer Tax Return is the official trigger for the foreign buyers tax. Declaring your foreign status on this form is what legally obligates you to pay the additional 20% tax when you close on the home.

What if Your Status Changes? Applying For a Tax Refund

Life happens. What if you pay the tax but then your residency status changes? The government has a clear refund process for individuals who later gain permanent residency or Canadian citizenship. If you meet the criteria, you can actually reclaim the full amount you paid.

But there are some strict rules and timelines you have to follow. To successfully apply for a refund, you must:

- Meet the Residency Requirement: You must become a Canadian citizen or a permanent resident within one year of the date the property was registered in your name.

- Live in the Home: The property must have been your principal residence for the rest of that first year.

- Submit Your Application: You have a specific window to file for the refund. It must be after the one-year anniversary of the registration date but before 18 months have passed.

Getting the right documents together and hitting these deadlines is non-negotiable for a smooth claim. This is where working with experienced real estate salespeople like James and Nicole Isherwood from the start pays off. They can help you understand all the potential paths, including the possibility of a future refund, so you're prepared for any scenario.

Get Expert Guidance on Your Property Purchase

Trying to make sense of the foreign buyers tax in Vancouver and the Fraser Valley can feel like a serious undertaking, but it’s not something you have to do alone. Having a seasoned professional on your side can transform a potentially overwhelming process into a clear, manageable plan. The rules are complex, the regional boundaries are specific, and knowing if you qualify for an exemption requires deep local knowledge.

This is where the expertise of real estate specialists James and Nicole Isherwood really makes a difference. With years of experience focused squarely on the Vancouver and Fraser Valley markets, they have a detailed, practical understanding of how this tax impacts international clients. They provide straightforward, actionable advice that’s tailored to your unique situation, making sure no detail gets overlooked.

A Support System for Your Investment

James and Nicole Isherwood offer more than just real estate services; they provide a complete support system. Their network of trusted legal and financial advisors ensures every piece of your purchase is handled correctly, from calculating your total tax liability to filing all the necessary paperwork on time.

This team approach is crucial for a smooth transaction. For instance, while typical realtor commissions in the area are structured at 7% on the first $100,000.00 and 3.5% on the balance, the foreign buyers tax adds a significant layer to your financial planning. The right guidance helps you prepare for these costs and explore every option available to you.

While the foreign buyers tax is a major financial factor, the right guidance makes it a manageable part of your journey to owning a home in British Columbia. Partnering with experts who understand the local landscape is the smartest investment you can make.

Ultimately, a successful purchase comes down to accurate information and strategic planning. To understand what your current property might be worth in this market, you can start with a complimentary home evaluation to get a clear financial picture.

For a personalized consultation on your property goals, reach out to James and Nicole Isherwood today.

Common Questions About the Foreign Buyers Tax

When you're planning a major property investment in the Fraser Valley, the details surrounding the foreign buyers tax can feel a bit overwhelming. It's natural to have questions. Here are some straightforward answers to the ones we hear most often from our clients.

What Happens If I Become a Permanent Resident After Buying?

This is a big one for many newcomers, and the good news is there’s a potential path to getting your money back. If you become a Canadian citizen or a permanent resident within one year of the property transfer registration date, you might qualify for a full refund of the foreign buyers tax you paid.

But there are a couple of important strings attached. You also have to move into the home and use it as your principal residence within 92 days of the registration date, and you must continue living there for the rest of that first year. The window to apply for the refund closes 18 months after the registration date, so it’s critical to work with a legal professional who can ensure all the paperwork is filed correctly and on time.

Does the Foreign Buyers Tax Apply to Pre-Sale Condos?

Yes, it absolutely does, but the timing is key. You don't pay the tax when you sign the initial pre-sale contract. Instead, the tax is due when the property title is officially registered in your name, which happens once the project is complete.

This is a crucial detail because the tax is calculated on the fair market value of the property at the time of registration, not your original contract price. A recent CBC News article highlighted how this can catch people by surprise. If property values climb during construction, the market value at completion could be significantly higher, increasing the total tax you owe.

Is the Federal Underused Housing Tax the Same Thing?

No, and it's vital not to mix them up—they are two entirely separate taxes.

- BC Foreign Buyers Tax: Think of this as a one-time 20% provincial tax you pay at the finish line when you purchase a property in a designated region.

- Federal Underused Housing Tax (UHT): This is an annual 1% federal tax on the value of residential real estate owned by non-resident, non-Canadians that the government considers vacant or "underused."

It is entirely possible for a foreign buyer in the Fraser Valley to get hit with both of these taxes. The rules can be complex, which is why getting clear, local advice from real estate experts like James and Nicole Isherwood is the best way to understand all your financial obligations and avoid any unwelcome surprises down the road.

Navigating the complexities of real estate in the Fraser Valley requires local expertise. For personalized guidance on buying or selling your home, contact Royal LePage Brookside Realty Property Management to ensure you have the best advice on your side. Learn more at https://www.brookside-pm.ca.