That moment you find your perfect home in British Columbia is incredible, but the sticker price is only one part of the story. The real question is, what will you actually pay on closing day? These final expenses, known as closing costs, are all the behind-the-scenes fees needed to officially and legally make that home yours.

Understanding Your Total Homebuying Cost in BC

Think of the home’s purchase price as the main event, and closing costs as the essential backstage crew making the whole show happen. These aren't optional add-ons; they cover everything from mandatory government taxes to the legal paperwork required to transfer the property title into your name. Forgetting to budget for them can create a serious financial roadblock right at the finish line.

The key to a smooth and stress-free purchase is getting a handle on these costs from the get-go. In British Columbia, closing costs typically run between 1.5% and 4% of the home's purchase price. This is cash you need to have ready on top of your down payment.

For example, on a $700,000 home, a 2% closing cost would be around $14,000. These funds cover big-ticket items like the Property Transfer Tax, legal fees, and title insurance. It's so important to estimate these costs accurately because, in most cases, they can't be rolled into your mortgage.

The Importance of Early Budgeting

Failing to account for these final costs can put your entire home purchase in jeopardy. Since this money is due on closing day, any shortfall can cause major delays or even void the contract altogether. That could mean losing your hard-earned deposit.

The single biggest financial mistake a homebuyer can make is underestimating closing costs. Planning for an extra 1.5-4% of the purchase price isn't just a suggestion—it's a critical step for a stress-free closing.

Here's a little preview of what our calculator can do. It's designed to help you visualize where your money is going.

This tool is all about moving beyond rough guesses and giving you a personalized look at what you can expect to pay. By preparing for these costs from the very beginning, you can walk into the process with confidence, not anxiety. For more strategies on a successful purchase, check out our comprehensive guide on buying a home.

Decoding the BC Property Transfer Tax

For most people buying a home in British Columbia, the Property Transfer Tax (PTT) is the biggest and often most confusing closing cost they’ll face. It's not a simple flat fee; it's a tiered tax based on your property's fair market value. Getting a handle on how this tax works is absolutely essential before you can accurately estimate your total closing costs.

Think of it like our income tax system. You pay a certain rate on the first chunk of the home's value, then a higher rate on the next chunk, and so on. This can make doing the math by hand feel a little complicated, but once you break it down, it starts to make sense.

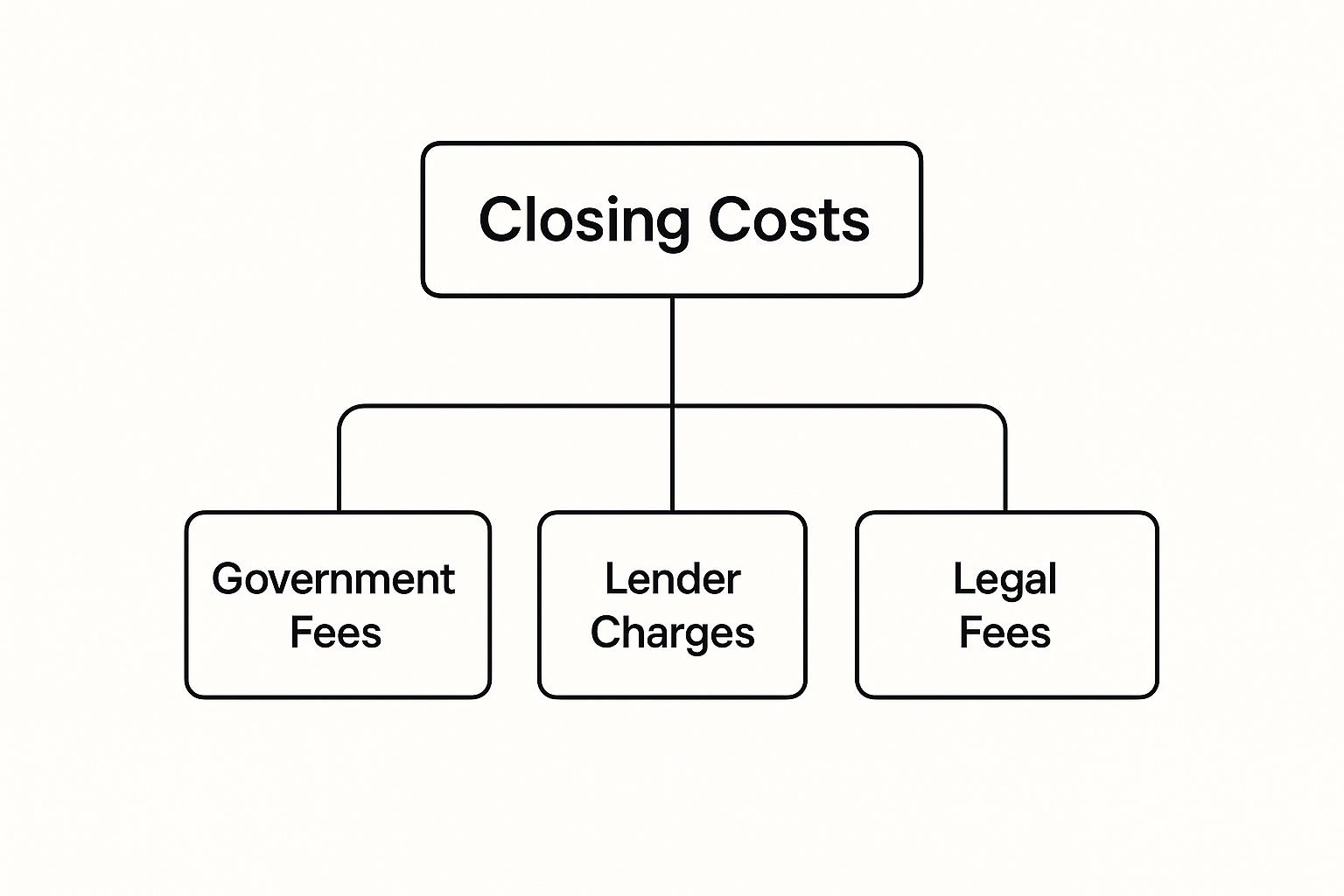

This infographic shows you exactly where the PTT lands in the grand scheme of your homebuying expenses.

As you can see, government fees like the Property Transfer Tax are a huge slice of the pie, sitting right alongside your legal and mortgage-related charges.

Calculating the Property Transfer Tax

The provincial government sets the PTT rates, which climb as the property value increases. As of the latest BC government updates, here’s the current breakdown:

- 1% on the first $200,000

- 2% on the portion of the value between $200,001 and $2,000,000

- 3% on the portion of the value between $2,000,001 and $3,000,000

- 5% on the portion of the value over $3,000,000

Let's walk through a real-world example to make this crystal clear. Say you’re buying a condo for $650,000. Here’s how you’d calculate the tax:

- First $200,000: 1% of $200,000 = $2,000

- Remaining Portion: Next up is the value from $200,001 to $650,000, which is a slice of $449,999. So, 2% of $449,999 = $9,000

- Total PTT Payable: $2,000 + $9,000 = $11,000

For a pricier property, like a $2.2 million house, the math just keeps climbing:

- First $200,000: 1% of $200,000 = $2,000

- Next $1,800,000: 2% of $1,800,000 = $36,000

- Next $200,000: 3% of $200,000 = $6,000

- Total PTT Payable: $2,000 + $36,000 + $6,000 = $44,000

As you can see, this tax adds up fast and becomes a major cash expense you need to have ready for closing day.

Can You Reduce or Eliminate This Tax?

Now for the good news. The BC government has a couple of programs that can slash or even completely wipe out your PTT bill. The two most common lifesavers are the First-Time Home Buyers' Program and the Newly Built Home Exemption.

Qualifying for one of these exemptions can save you thousands—sometimes tens of thousands—of dollars. It's essential to check your eligibility with your real estate professional or lawyer as early as possible in your homebuying journey.

The First-Time Home Buyers' Program

This program is an absolute game-changer for many people trying to get into the market. As of April 1, 2024, if you qualify as a first-time buyer, you could get a full PTT exemption on homes with a fair market value up to $835,000. There's also a partial break for homes priced between $835,001 and $860,000. This recent increase in the threshold, announced in the BC Budget 2024, reflects the government's effort to address housing affordability.

To get the exemption, you need to meet a list of requirements, including:

- Being a Canadian citizen or permanent resident.

- Having lived in British Columbia for at least a year right before you register the property.

- Never having owned an interest in a home that was your main residence anywhere in the world, ever.

The rules are quite strict, so it’s crucial to go over the complete eligibility requirements on the official government website.

The Newly Built Home Exemption

This program is designed to encourage the purchase of new construction. If you buy a brand-new home with a fair market value up to $1,100,000, you might be completely exempt from the tax. A partial exemption is available for newly built homes valued between $1,100,001 and $1,150,000.

Some of the key requirements include:

- The property has to be a brand-new build.

- The buyer must be an individual and either a Canadian citizen or a permanent resident.

- The property must be used as your principal residence.

When all is said and done, the data shows that the land transfer tax is typically the largest single closing expense in British Columbia. For this reason, a good rule of thumb is to budget between 1.5% and 4% of the home's purchase price to cover all your closing fees—that includes legal services, inspections, and insurance. For a $700,000 home, that could mean having $10,500 to $28,000 ready. You can dive into a deeper breakdown of these estimated expenses to get fully prepared.

Navigating Your Legal and Administrative Fees

Beyond government taxes, you'll have a few professional services to pay for that are essential to finalizing your home purchase and protecting your investment. This is where your legal and administrative fees come into the picture. They might feel like just another line item on your closing cost statement, but trust me, each one serves a critical purpose in making sure the whole process is smooth and secure.

These fees cover the experts who pour over contracts, verify who actually owns the property, and shield you from potential legal headaches down the road. Let’s break down what these services are, why you need them, and what they typically cost, so you can budget with confidence. A good closing costs calculator for BC can give you a ballpark figure, but understanding what's behind each fee is the real key.

Your Legal Team: Lawyer vs. Notary Public

In British Columbia, you’ll need to hire either a real estate lawyer or a notary public to handle the legal side of the property transfer. Think of them as the captain of your closing day ship, ensuring every legal document is in order and that the property title is correctly transferred into your name.

A real estate lawyer can provide comprehensive legal advice, step in to handle any disputes that might pop up, and represent you if the deal gets messy. A notary public is also licensed to manage property transfers but usually handles more straightforward, uncontested deals. For most standard home purchases, either professional is a solid choice.

The most important thing is to choose a professional you trust. Their entire job is to protect your interests, from doing a deep dive on the property's title history to making sure all the money goes where it's supposed to on closing day.

Cost-wise, you should plan to budget between $1,500 and $3,000 for these legal services. This fee typically bundles together a few key tasks:

- Title Search: This is where they confirm the seller is the true legal owner and that there are no nasty surprises like liens or claims against the property.

- Document Preparation: They'll draft and review all the legal paperwork, including the important Statement of Adjustments.

- Registration: This is the official step of registering your name on the property title with the Land Title and Survey Authority of BC.

- Disbursement of Funds: They manage the secure transfer of your down payment and mortgage money to the seller.

The Shield of Title Insurance

Title insurance is a one-time fee that buys you long-term protection. It's an insurance policy that protects you (and your lender) from financial losses that come from problems with the property’s title. We're talking about hidden issues that even a diligent lawyer’s search might not turn up.

This isn't your standard home insurance that covers fires or floods. Instead, it protects you from financial fallout due to things like:

- Title Fraud: Someone trying to fraudulently sell or mortgage your property without you knowing. This is a growing concern, with reports showing a significant rise in real estate title fraud across Canada.

- Survey Errors: Disputes over where your property line actually is or encroachments that weren't spotted on an old survey.

- Unknown Liens: Lingering claims against the property from a previous owner's unpaid debts or taxes.

Most lenders in BC will insist you get a title insurance policy. The cost usually lands somewhere between $250 and $500, paid as a one-time premium when you close. It’s a pretty small price to pay for some serious peace of mind.

Lender-Required Administrative Fees

Your mortgage lender will also have a couple of administrative costs that get rolled into your closing fees. The most common one is the appraisal fee.

An appraisal is simply a professional, unbiased assessment of the property's fair market value. Why does your lender care? They need it to make sure the home is actually worth the amount of money they're lending you. In essence, they're protecting their own investment. You can expect to pay somewhere between $400 and $700 for a professional appraisal.

Before we move on, here's a quick reference table to help you visualize these costs.

Estimated Range of Common Closing Costs in BC

Here’s a breakdown of typical costs for various services required to close a real estate deal in British Columbia. Keep in mind that costs can vary by provider and location.

Cost ItemTypical Price Range (CAD)PurposeLegal Fees$1,500 – $3,000To hire a lawyer or notary for title transfer, document prep, and fund disbursement.Title Insurance$250 – $500A one-time policy to protect against title defects, fraud, and survey issues.Property Appraisal$400 – $700A lender-required assessment to confirm the property's market value.

By understanding the why behind these legal and administrative fees, you can see them not just as expenses, but as vital investments in a secure and successful home purchase. These costs are a standard part of buying a home in BC, and accounting for them early on is the mark of a well-prepared buyer.

Budgeting for Property-Related Expenses

While government taxes and legal fees make up a big chunk of your final closing bill, a few other crucial costs are tied directly to the property itself and your mortgage. These are the expenses that many buyers accidentally overlook, but they're absolutely essential for protecting your investment.

Getting a handle on these is a key step before you can get an accurate estimate of your total costs. Let's break down these property-specific expenses, from inspections that save you from future headaches to the insurance your lender won't let you close without.

The Home Inspection: Your Best Defense

Before you commit hundreds of thousands of dollars to a property, spending a few hundred on a home inspection is one of the smartest moves you can make. While it isn't always mandatory, think of it as your best line of defense against discovering expensive surprises after you get the keys.

A professional home inspector dives deep, examining the home's structure, roof, plumbing, and electrical systems for any potential red flags. It’s like a comprehensive health check-up for the house. They'll give you a detailed report on any existing problems or areas that might need attention soon, from a minor leaky faucet to major signs of foundation trouble.

This report gives you powerful leverage. You can use it to negotiate repairs with the seller or, in serious cases, walk away from a deal that could turn into a financial nightmare. A typical home inspection in BC will run you between $400 and $700.

Understanding Property Tax Adjustments

Property taxes are paid once a year to the local municipality. But since you're almost certainly buying the home partway through the year, these taxes need to be split fairly between you and the seller. This is done through something called a property tax adjustment.

Here's how it works: if the seller has already paid the property taxes for the entire year, you'll need to reimburse them for the portion of the year you'll own the home. On the flip side, if the taxes aren't paid yet, the seller will give you a credit for the days they owned the property that year, and you'll be on the hook for the full bill when it comes due.

Your lawyer or notary public handles all the math, calculating this adjustment down to the exact day. It ensures you only pay taxes for the time you legally own the property, making it a fair and seamless process for everyone.

Property Insurance: A Non-Negotiable Requirement

You simply cannot get a mortgage in Canada without proof of property insurance (sometimes called fire insurance). Lenders demand it to protect their financial stake in your home. You must have a policy fully in place before closing day.

Your lawyer will need to send proof of this insurance to the lender before they will release the mortgage funds to complete the purchase. This insurance protects your home from damage or loss from events like fire, theft, and other common hazards. Recent data from the Insurance Bureau of Canada shows that severe weather events are causing insured losses to climb, making comprehensive coverage more important than ever.

When you're shopping around for a policy, here's what to look for:

- Guaranteed Replacement Cost: This is crucial. It ensures your policy will cover the full cost to rebuild your home, even if that cost exceeds your policy limit.

- Sufficient Liability Coverage: This protects you financially if someone is ever injured on your property.

- Water Damage Protection: Pay close attention to the fine print on coverage for floods, sewer backups, and overland water.

Special Costs for Strata Properties

Buying a condo or townhouse? You'll run into a few extra costs related to the strata corporation. Before your purchase is final, you'll need to review a big package of strata documents, which includes things like meeting minutes, bylaws, and the strata's financial statements.

While the seller usually pays for this main package, you might have to cover the cost of a Form B (which details the unit's status) or a Form F (which confirms the seller's strata fees are paid up). These are necessary for closing and are usually minor, costing around $35 to $50 each.

Budgeting accurately for these property-related expenses is just as important as planning for taxes and legal fees. Once you understand all these closing costs, you can get the full picture of your ongoing homeownership expenses by using helpful tools like a mortgage payment calculator to see how it all fits together.

A Real-World Closing Cost Calculation

Theory and percentages are one thing, but seeing how the numbers actually stack up in a real-world scenario is where it all clicks. Let's step away from the abstract for a moment and walk through a complete, step-by-step closing cost calculation for a pretty typical home purchase here in British Columbia.

This example should give you the confidence to use our closing costs calculator for BC and get a solid grip on your own potential expenses.

Let’s picture a family buying an $850,000 townhouse in Surrey. They aren't first-time homebuyers, and they're putting 20% down. So, what cash will they need to have ready on closing day, on top of that down payment?

Calculating the Big Ticket Items

First up, the elephant in the room: the Property Transfer Tax (PTT). Since our family doesn't qualify for any exemptions, we'll apply the standard tiered rates to their $850,000 purchase price.

- 1% on the first $200,000 = $2,000

- 2% on the portion from $200,001 to $850,000 (which is $649,999) = $13,000

- Total PTT Payable = $15,000

Next, we factor in the legal fees. After getting a few quotes, the family found a reputable real estate lawyer. Their fee, which covers everything from the title search to preparing and registering all the documents, comes to $2,200.

A crucial document your lawyer will prepare is the Statement of Adjustments. Think of it as the final, detailed receipt for the entire transaction. It meticulously lists every single credit and debit between you and the seller, revealing the exact dollar amount you need to bring to their office to close the deal.

This statement is the definitive financial breakdown. It ensures every last cent is accounted for, from pre-paid property taxes to any strata fees.

Adding Other Essential Services

Now for the other necessary costs—the ones that are easy to forget but are absolutely vital for a secure purchase. These are the expenses that protect your investment.

- Title Insurance: Their lender requires a policy to guard against things like title fraud or survey disputes. This is a one-time premium of $400.

- Home Inspection: Before committing, they smartly paid for a thorough home inspection. This proactive step cost them $550 but bought them invaluable peace of mind.

- Property Appraisal: The lender needed to confirm the home's value, which meant hiring a professional appraiser for $500.

Finally, we have to account for property tax adjustments. Let's say the sellers pre-paid their property taxes for the entire year, and the closing date is October 1st. The buyers now have to reimburse the sellers for the last three months of the year (October, November, December). If the annual taxes are $3,600, the buyers owe the sellers for one-quarter of that amount, which comes to $900.

The Final Closing Cost Tally

Alright, let's add it all up to see the total cash this family needs to have on hand to close the deal, completely separate from their down payment.

Cost ItemEstimated Amount (CAD)Property Transfer Tax (PTT)$15,000Legal Fees & Disbursements$2,200Title Insurance$400Home Inspection Fee$550Lender's Appraisal Fee$500Property Tax Adjustment$900Total Estimated Closing Costs$19,550

As you can see, the costs add up quickly. For their $850,000 purchase, the family needs $19,550 in liquid cash just to finalize the deal. That works out to be about 2.3% of the purchase price, which falls right in line with the typical range we see across BC. By mapping out each expense like this, you can walk into your closing day without any nasty surprises and with total financial confidence.

Common Questions About BC Closing Costs

Even with a detailed breakdown, it's totally normal for questions to pop up during the final steps of buying a home in British Columbia. These are the details that often trip people up right before the finish line. Let's tackle the most common ones with straight-up, practical answers to help you get through the home stretch without breaking a sweat.

Can I Add Closing Costs to My Mortgage in BC?

This is easily one of the most frequent questions, and the short answer is usually no. In BC, lenders expect you to have the cash on hand to cover your closing costs—things like the Property Transfer Tax and your legal fees. This money is completely separate from your down payment and needs to be paid out of pocket on closing day.

You might see some lenders advertising a "cash-back" mortgage, which sounds tempting. They give you a lump sum of money that you could, in theory, put towards these costs. But here's the catch: it’s not free money. These products almost always come with a much higher interest rate, which will cost you a lot more over the life of your mortgage. Always run the numbers with your mortgage broker before even thinking about going this route.

The standard play here is to have your closing cost funds ready to go as liquid cash. Trying to roll them into your mortgage is a move that can haunt your bank account for years.

For almost everyone, the smartest strategy is to save for these costs well ahead of time, just like you did for your down payment.

When Exactly Do I Pay My Closing Costs?

The actual payment happens right at the very end, but you need to have the money ready a few days before your official closing date. Your lawyer or notary will send you a final document called the Statement of Adjustments, which lays out the exact amount you owe down to the last penny.

From there, you’ll need to get those funds into your lawyer’s trust account. This is typically done with a bank draft or a certified cheque; personal cheques won't cut it for a transaction this large. Your lawyer then pools this money with your down payment and the mortgage funds from your lender to finalize the purchase on your closing day. To avoid any last-minute panic, make sure this money is sitting in an easily accessible bank account long before you need it.

Are Any Closing Costs Negotiable?

It would be great if you could haggle over every single fee, but the reality is some costs are fixed while others have a bit of wiggle room.

- Non-Negotiable Costs: The Property Transfer Tax is the big one. The rates are set by the provincial government and are based entirely on the home's purchase price. There’s absolutely no negotiating this.

- Negotiable Costs: On the other hand, fees for professional services are fair game. This includes what you pay your lawyer or notary, your home inspector, and your property appraiser.

You can, and absolutely should, shop around. Get quotes from a few different qualified professionals to compare their rates and what they offer. The cheapest option isn't always the best, but doing your homework can help you find top-notch service at a competitive price. Always ask for a detailed breakdown of their fees upfront so there are no nasty surprises on the final bill. The difference between a few quotes could easily save you hundreds of dollars.

What if I Cannot Afford the Closing Costs?

This is the nightmare scenario every homebuyer wants to avoid. Showing up on closing day without enough money for your closing costs is a huge problem. It means you're in breach of your contract of purchase and sale, and the consequences are serious. The seller could sue you, and you would almost certainly lose your entire deposit.

This is exactly why using a closing costs calculator for BC right from the beginning of your house hunt is so critical. Accurate budgeting is your best line of defense. If you do find yourself short, your options are incredibly slim. A documented financial gift from an immediate family member is one possibility, but your lender needs to sign off on it in writing well in advance.

Proactive, careful planning is the only reliable way to sidestep this kind of high-stress situation. Budgeting for 1.5% to 4% of the purchase price is a safe range that prepares you for these final, mandatory expenses. As you map out your finances, it can also be insightful to understand the other side of the deal by learning more about the process of selling your home in BC.

At Royal LePage Brookside Realty, we believe a well-informed homebuyer is an empowered one. If you have more questions or are ready to take the next step in your real estate journey in the Fraser Valley, our team is here to provide the expert guidance you need.