You're probably doing the same math a lot of Maple Ridge buyers do at the kitchen table. Rent, savings, down payment, closing costs, mortgage payment, then a quick search for “first-time home buyer programs bc 2026” to see if there's a way to make the numbers work.

That search usually starts with a dream that's very local. A condo in West Maple Ridge close to shops and an easier commute. A townhouse in Albion near parks and schools. A place where Saturday might mean the Haney Farmers Market, and Sunday might mean a trail day near Golden Ears Provincial Park. For a lot of buyers, the goal isn't flashy. It's stability, a front door that's yours, and a home base in a community you already know.

Maple Ridge makes that dream feel close and far away at the same time. Buyers can still find options across neighbourhoods like Cottonwood, Silver Valley, Albion, and West Maple Ridge, but the upfront cash needed to buy can still feel like the hardest hurdle. That's where the right programs matter. Not as a magic fix, but as tools that can change timing, monthly comfort, and how competitive you can be when the right listing shows up.

I've found the biggest mistake first-time buyers make isn't lack of effort. It's assuming every incentive works the same way in every neighbourhood and price band. It doesn't. A condo search in West Maple Ridge leads to one strategy. A newer townhouse in Albion can lead to another. If you want a helpful starting point on neighbourhood fit, this guide to Maple Ridge neighbourhoods for first-time buyers is worth bookmarking.

A second useful step is checking your budget against real monthly ownership costs instead of relying on broad guesses. I like using buyer affordability insights to pressure-test what feels comfortable before buyers start writing offers.

Dreaming of a Home in Maple Ridge

A lot of first purchases here start with a very practical conversation. Not “What's the perfect home?” but “What kind of home gets us into the market without stretching us too thin?”

That's a smart question in Maple Ridge. West Maple Ridge can appeal to buyers who want convenience and established streets. Albion often pulls young families who want parks, newer townhome communities, and access to schools. Silver Valley attracts buyers who love a quieter edge-of-nature setting, but the style of home there can push the conversation quickly into what incentives still apply and which ones fade out.

What first-time buyers are really choosing

Most buyers aren't only choosing a home type. They're choosing a lifestyle rhythm.

- West Maple Ridge condo buyers often want lower-maintenance ownership and walkability for day-to-day errands.

- Albion townhouse buyers usually focus on family function, more space, and a neighbourhood feel near schools and parks.

- Silver Valley buyers tend to prioritise setting and newer housing stock, even if that means trade-offs on budget or commute.

The right first home is often the one that leaves room in your monthly budget for real life, not just the one that looks best in listing photos.

Why 2026 planning needs to be specific

Government programs can make a real difference, but only if you apply them to the actual type of property you're targeting. A buyer looking at an older condo and a buyer targeting a new build townhome are not playing the same game. Their financing structure can be different. Their tax savings can be different. Their monthly payment strategy can be different.

That's why broad national advice falls short in Maple Ridge. Here, a few thousand dollars at closing can be the difference between keeping your emergency cushion intact or draining every account to get the keys.

If you're serious about buying in 2026, it helps to think less like a browser and more like a planner. Pick your likely neighbourhood. Pick your likely property type. Then build your financing around that, not the other way around.

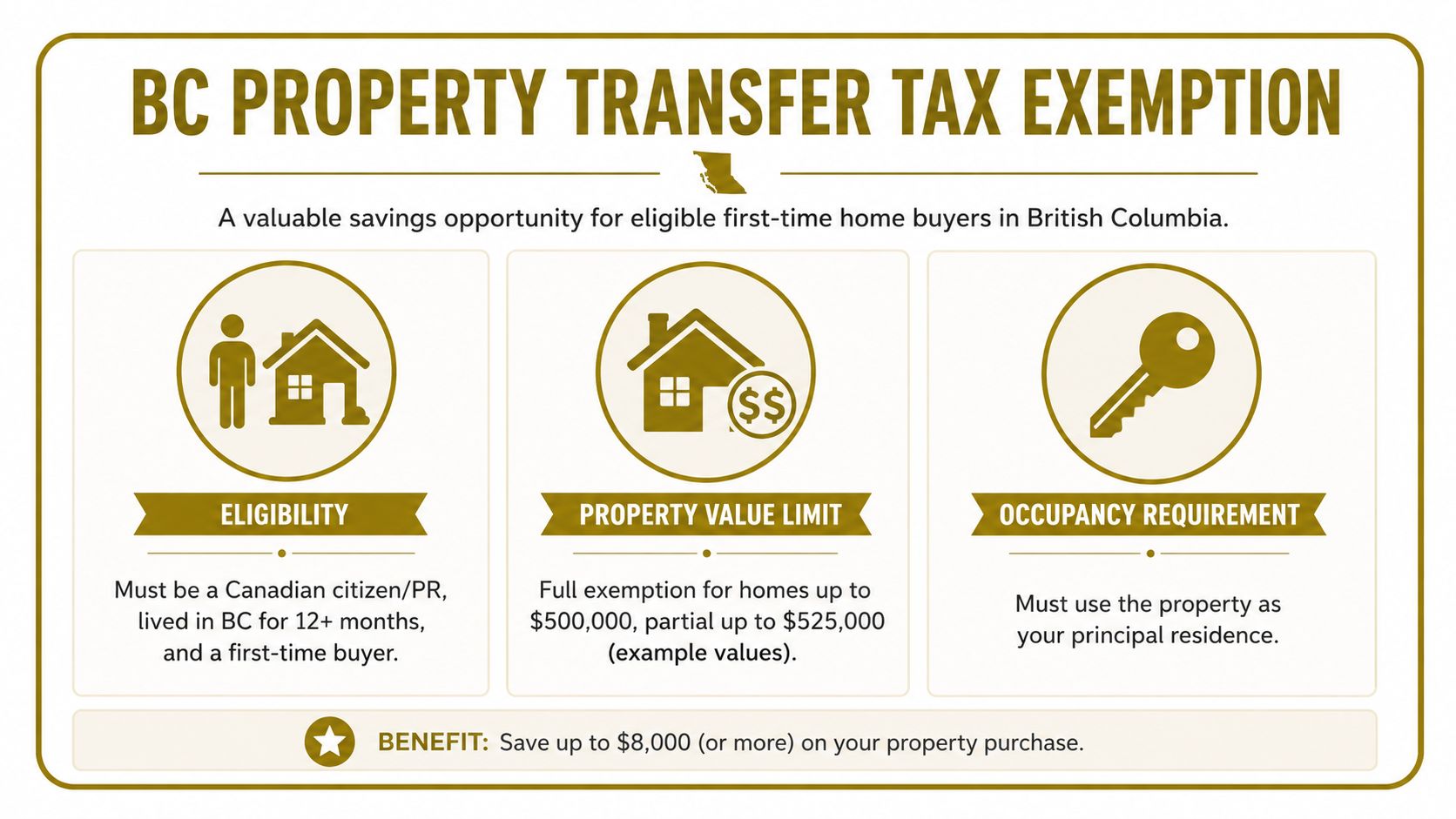

Understanding BC's Property Transfer Tax Exemption

A lot of first-time buyers in Maple Ridge get surprised by closing costs. They spend months focused on the down payment, then realize the tax bill, legal fees, moving costs, and setup expenses all hit at once.

That is why the BC Property Transfer Tax exemption matters.

For eligible first-time buyers in B.C., this program can reduce or remove the Property Transfer Tax on a purchase, which directly lowers the cash you need on completion. The current rules for price thresholds and buyer eligibility are outlined in this BC first-time home buyer tax exemption overview.

What this means in Maple Ridge

In Maple Ridge, this exemption is most useful for buyers shopping in the entry-level part of the market. A condo in West Maple Ridge may sit in a range where the tax savings still help in a meaningful way. An Albion townhouse often pushes higher, which can reduce the benefit or wipe it out entirely depending on the final price.

That changes how I would approach the search.

If a buyer wants to keep more cash in reserve after closing, I usually want the price range discussed early, before we write offers. Saving money on transfer tax can mean the difference between having funds left for blinds, basic repairs, and a proper emergency cushion, or arriving on possession day with every account drained.

If you want a plain-English refresher on the tax itself, this quick breakdown of what land transfer tax means in practice helps.

The plain-English qualification checklist

The price is only part of the equation. Personal eligibility matters just as much.

Who qualifies: You need to be a Canadian citizen or permanent resident, meet the B.C. residency history requirement, and be a true first-time buyer who has never owned a principal residence anywhere in the world.

I have seen buyers assume they qualify because the home price fits. Then they find out a residency detail or past ownership issue knocks them out. That is a frustrating problem because by then they have often built their budget around savings they may not ultimately receive.

Where buyers make better decisions

This exemption works best when it is built into the plan from day one.

- Works well when your search is centred on price points where the exemption or partial exemption still saves real money.

- Works well when your realtor, mortgage broker, and notary know early that you intend to claim it.

- Works poorly when buyers treat the list price as the only number that matters.

- Works poorly when paperwork is left until the last stretch before closing.

A Maple Ridge buyer comparing two similar homes should not only ask, “Which one do I like more?” They should also ask, “Which one leaves me in a stronger cash position after completion?”

That is the practical value here. In 2026, first-time buyer programs are not just about qualifying. They are about choosing a home that still feels manageable after you get the keys.

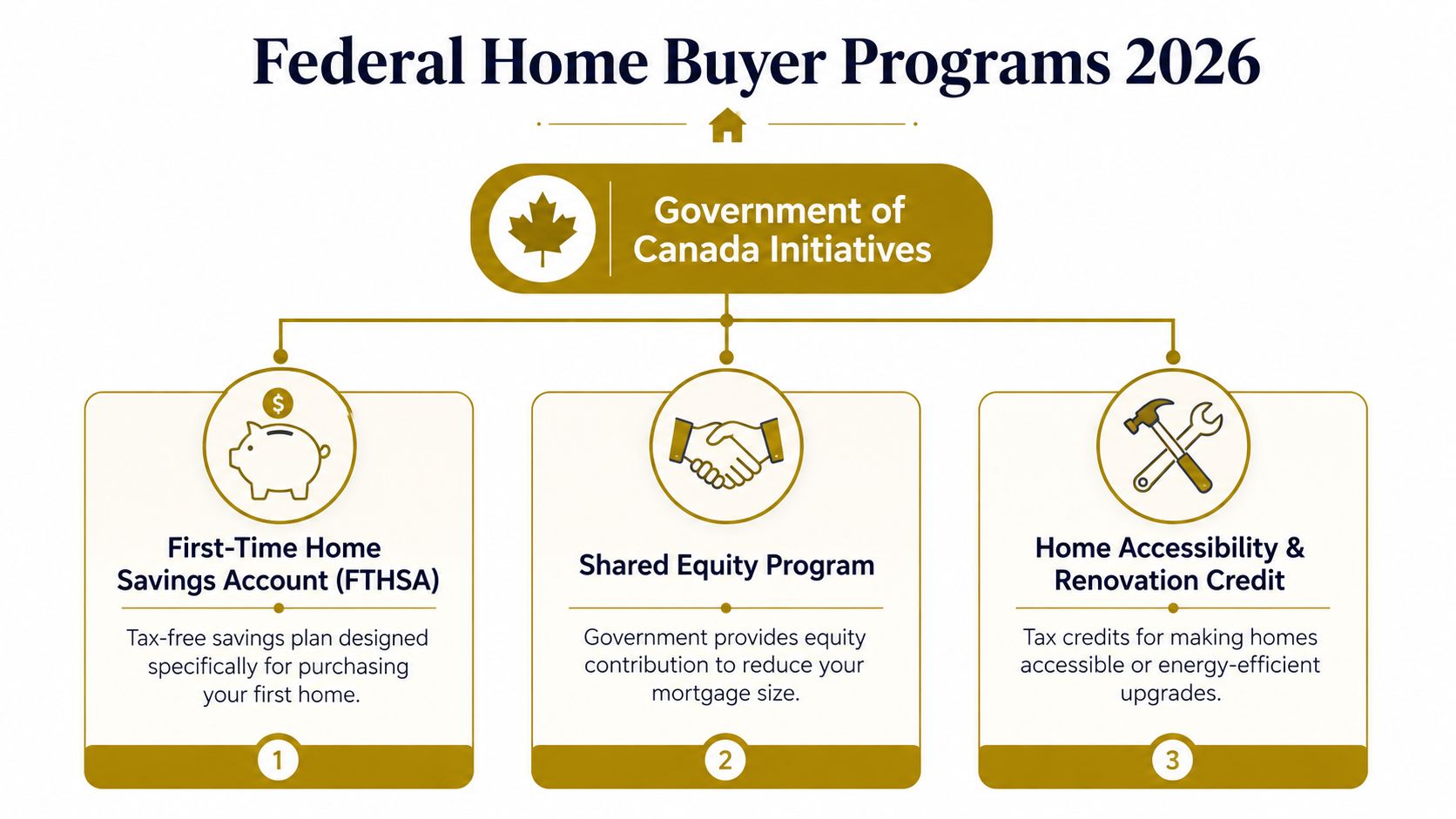

Exploring Federal Home Buyer Programs for 2026

A lot of Maple Ridge buyers reach the same point. They have saved, they understand the B.C. tax side, and then they ask the practical question. “What can Ottawa do to help me buy here in 2026?”

Federal programs matter most when the monthly numbers are tight. That is common in Maple Ridge. A buyer looking at a condo in West Maple Ridge and a buyer trying to stretch into a newer townhouse in Albion are both first-time buyers, but they usually need different tools.

The Home Buyers' Plan

The Home Buyers' Plan (HBP) lets eligible buyers withdraw money from an RRSP for a down payment. In real life, this is often the cleanest federal option because it uses your own savings rather than changing the ownership structure of the home.

I find it fits best for buyers who have been contributing steadily to an RRSP and need more cash flexibility at closing. That often describes someone buying a resale condo in West Maple Ridge, where keeping extra cash on hand for closing costs, moving, and the first few months of ownership matters just as much as the down payment itself.

The trade-off is simple. You are pulling future retirement savings into today's purchase, and that money has to be repaid under the program rules.

The First-Time Home Buyer Incentive

The First-Time Home Buyer Incentive (THBI) offers shared-equity mortgages of 5% for existing homes and 10% for newly constructed homes, as explained in this Maple Ridge first-time buyer program guide. It can lower monthly mortgage costs, which is why buyers close to their qualification ceiling still ask about it.

But shared equity needs a sober look. If the home goes up in value, the government shares in that gain when the incentive is repaid. If a buyer already qualifies comfortably, I usually want them to compare that future cost against the short-term payment relief before deciding.

A buyer considering a modest older condo may not need this at all. A buyer trying to make a new-build purchase work may see real value in it.

Practical rule: Use THBI to solve a payment problem you can clearly define.

The 30-year amortization option

Some first-time buyers purchasing eligible insured new builds can access a 30-year amortization option. The practical effect is lower monthly payments, but more interest paid over time.

That can matter in Maple Ridge where new construction sometimes pulls buyers away from resale. A newer unit may offer lower maintenance risk in the first few years, but the purchase price is often higher. Spreading payments over a longer period can make that monthly budget work, especially for buyers choosing between an older resale and a newly built home they plan to live in for several years.

It is not automatically the better choice. Lower payments help cash flow. A longer amortization also slows down principal paydown, so buyers need to decide whether monthly breathing room is more important than building equity faster.

Which federal tool tends to fit which buyer

These programs solve different problems, and I would not treat them as interchangeable.

- HBP helps buyers who already have RRSP savings and want more down payment flexibility.

- THBI helps buyers who need lower monthly costs and are comfortable sharing future equity.

- 30-year amortization helps buyers focused on payment comfort in an eligible new build, even if it means carrying the mortgage longer.

The Maple Ridge angle matters here. A buyer shopping for a more attainable condo in West Maple Ridge may get enough value from the HBP alone. A buyer reaching for a newer home in a higher-priced pocket may need to combine two federal tools and then compare whether the extra complexity is still worth it.

For a broader policy view, this article on federal housing measures and B.C. affordability concerns is a useful read.

How to Stack Programs A Maple Ridge Scenario

First-time home buyer programs in BC for 2026 become real when considering an example. Let's use a practical Maple Ridge example. A buyer is purchasing an $850,000 townhouse in Albion.

Albion is a neighbourhood where first-time buyers often try to stretch from condo ownership into family-friendly townhome living. You get a stronger neighbourhood feel, access to parks, and a home style that can work longer term. But the price point also lands right in one of the trickiest parts of the PTT exemption rules.

Why the $850,000 price point matters

A lot of generic guides say buyers receive a partial exemption between the upper threshold and the cut-off, but that misses the real issue. The drop-off gets sharp.

For homes priced between $835,000 and $860,000, the savings fall quickly. At $850,000, the buyer receives 50% of the $8,000 maximum exemption, which is $4,000. At $859,000, the benefit is less than $100, which creates a real pricing trap for buyers who assume they're still getting meaningful help near the top of the range, as highlighted in this discussion of the BC PTT sliding scale trap.

A buyer at $850,000 is still getting something useful. A buyer at $859,000 is basically not.

That difference matters in negotiations. In Maple Ridge, I'd rather have a buyer understand this before writing an offer than realise it after subjects are removed.

A stacked strategy for an Albion townhouse

Here's how the stack can look in principle for an eligible first-time buyer:

- HBP funds can support the down payment side if the buyer has RRSP savings available.

- THBI may help reduce the mortgage burden on an eligible purchase if the buyer and lender determine it fits.

- PTT exemption savings still exist at $850,000, but they're reduced to $4,000 rather than the maximum.

If you're still sorting out the basics of budgeting, financing, and neighbourhood fit, this local guide on first-time buyer considerations in Maple Ridge is a useful companion read.

Sample savings view

| Item | Amount | Impact on Buyer |

|---|---|---|

| Purchase price | $850,000 | Sets the budget level for an Albion townhouse search |

| BC PTT exemption at this price point | $4,000 | Reduces upfront closing cost pressure |

| Maximum PTT exemption reference point | $8,000 | Shows how much has already been lost by this stage of the sliding scale |

| Difference between max exemption and $850,000 exemption | $4,000 | Highlights the pricing penalty of shopping higher in the range |

| PTT exemption near $859,000 | Less than $100 | Shows why buyers shouldn't assume “partial” means meaningful |

What this looks like in the real world

In a live transaction, the stack doesn't just change the spreadsheet. It changes the buyer's confidence. A stronger down payment position can make financing cleaner. Lower monthly obligation can help the lender file. A few thousand saved at closing can keep cash in reserve for moving, furniture, or the first repair that always seems to show up after possession.

But there's a trade-off. An $850,000 townhouse in Albion may still be the right buy even with only a partial tax break. The key is knowing you're no longer shopping in the sweet spot of the provincial exemption. You're making a conscious decision to pay more for space, location, or product type.

That's why neighbourhood-level advice matters. West Maple Ridge condo buyers may focus on preserving cash and entering ownership sooner. Albion townhouse buyers may accept thinner tax savings because the home works better for a young family. Both choices can be smart. They're just different strategies.

The wrong move is drifting upward in price without understanding what you're giving up. In Maple Ridge, that usually shows up when buyers jump from “almost ideal” to “we can probably make it work” and accidentally lose one of the few meaningful closing-cost advantages available to first-time buyers.

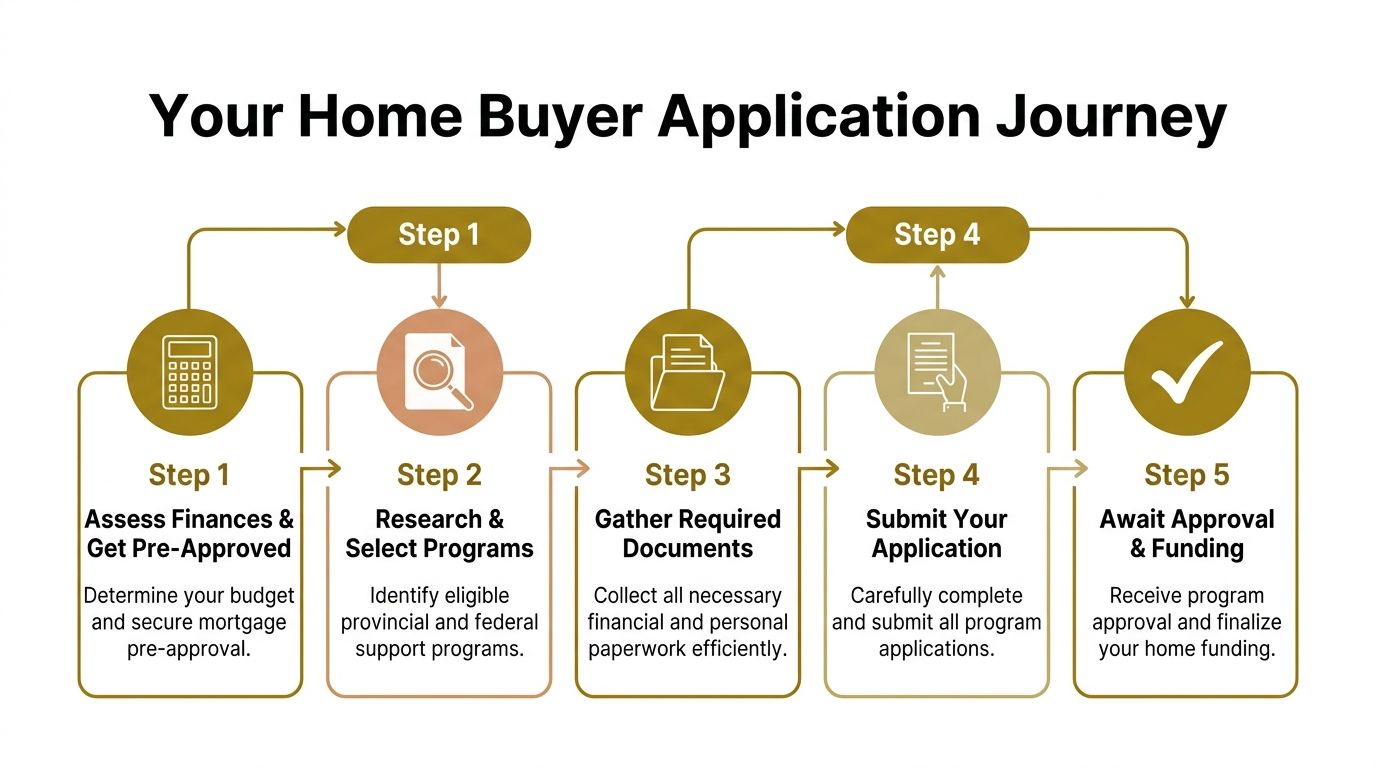

Your Step-by-Step Application Journey

The application side of this process is where good planning saves stress. Most first-time buyers don't lose out because the programs are impossible. They lose out because they speak to the wrong people in the wrong order.

Start with financing. Then build the property search around what that financing can support.

Start with the right mortgage conversation

Not every lender conversation is equal. You want a mortgage broker or lender who understands first-time buyer program layering, not just basic pre-approval math.

A standard pre-approval is useful, but a strategic pre-approval is better. It tests whether RRSP withdrawals, shared-equity options, or eligible new-build financing can improve the file before you shop.

If you need a refresher on the basics, this guide to mortgage pre-approval in Maple Ridge is worth reading first.

Ask one direct question early. “Which first-time buyer programs actually improve my file, and which ones only sound helpful?”

Build your property search around eligibility

Local guidance holds significant importance. If you're targeting a new build, the financing path may differ from a resale townhome. If you're near a provincial price cut-off, your search range may need tighter discipline.

A Maple Ridge buyer searching in Albion, Silver Valley, Cottonwood, and West Maple Ridge shouldn't treat all listings the same. Some homes suit a first-time buyer strategy better than others because of price, age, property type, or likely lender fit.

Keep your paperwork moving in parallel

The smoothest transactions happen when buyers gather documents before they're urgently needed.

- Income and identity documents should be organised before offer time.

- Proof of funds needs to be easy to verify, especially if RRSP money is part of the plan.

- Eligibility details for exemptions should be confirmed early, not guessed at.

- Legal closing coordination should happen with a notary or lawyer who knows which filings need attention.

A short video can also help if you want a quick visual overview before diving into paperwork.

The closing-stage handoff

Your realtor helps shape the offer and property strategy. Your broker handles financing structure. Your lawyer or notary makes sure the legal and registration side is correct.

That handoff matters. Buyers often assume incentives are “automatic.” They aren't. Good professionals flag them, document them, and make sure nobody is scrambling right before possession.

Taking Your Next Step Toward a Maple Ridge Home

The good news for first-time buyers is that 2026 still offers real ways to reduce the strain of buying. The hard part is that these programs don't help equally at every price point, in every property type, or in every Maple Ridge neighbourhood.

That's why a local strategy beats generic advice every time. A buyer focused on a West Maple Ridge condo may need a very different plan from a buyer trying to secure a newer townhome in Albion. One may care most about preserving cash at closing. The other may need a monthly payment solution. Neither path is wrong if it fits the home, the budget, and the long-term plan.

What works is simple. Get clear on your true comfort zone. Understand which programs apply to the homes you're considering. Then build a search around the numbers, not around wishful thinking.

The smartest first-time buyers aren't always the ones with the biggest down payment. They're the ones who understand how to match the right program to the right property.

If you're buying in Maple Ridge, local details matter more than is often underestimated. School catchments, strata style, development age, commuting routes, and the difference between a pricing sweet spot and a pricing trap can all shape whether a purchase feels manageable or stressful after the keys are in your hand.

A steady plan usually wins. Not a rushed one.

If you're weighing condos, townhomes, or family homes in Maple Ridge or Pitt Meadows, Royal LePage Brookside Realty Property Management can help you sort through the local options and build a buying or selling strategy that fits your budget, timing, and goals.