Trying to jump into the competitive real estate markets in Vancouver and the Fraser Valley can feel like a lot to take on. But here's a secret: the real first step isn't scrolling through listings. It's getting a mortgage pre-approval.

Think of a pre-approval as a lender's conditional commitment to loan you a specific amount of money. It's your official ticket into the serious home-buying game.

Your First Step in the BC Real Estate Market

A mortgage pre-approval instantly changes you from a window shopper into a confident buyer who’s ready to make a serious offer. This isn't the same as a pre-qualification, which is really just a rough guess based on numbers you provide yourself. A pre-approval is the real deal—a formal process where a lender digs into your financial details to confirm exactly how much you can borrow.

Having that pre-approval letter in hand gives you a huge advantage, especially in fast-moving markets like Vancouver. When you put in an offer backed by a pre-approval, sellers see you as a serious contender whose financing is already lined up.

Local real estate experts James and Nicole Isherwood always say that this one piece of paper can make an offer stand out, sometimes even more than a higher bid that doesn't have the same financial certainty. As you start your journey, it's also smart to stay informed about things like potential homebuyers and Stamp Duty Land Tax considerations to avoid any surprises.

Pre-Approval vs Pre-Qualification At a Glance

It's really important to know the difference between these two terms. A pre-approval gives you clarity and makes you a credible buyer, something a pre-qualification just can't do. For anyone serious about buying a home in British Columbia, this is a critical distinction.

Here’s a quick look at how they stack up.

As you can see, one is a powerful tool, while the other is more of a casual first look.

Securing a mortgage pre-approval isn’t just a formality; it’s the foundational step that gives you a clear budget and the confidence to compete effectively in the BC property market. It tells sellers, and just as importantly, tells you what you can truly afford.

Why Pre-Approval Is Your Golden Ticket

In the red-hot real estate markets of Vancouver and the Fraser Valley, a great home can get snapped up in days, often with multiple offers on the table. In this kind of fast-paced environment, walking in with a mortgage pre-approval letter is your golden ticket. It instantly tells sellers you’re a serious, qualified buyer, giving your offer the credibility it needs to stand out.

But this one document does more than just show you mean business. It gives you some much-needed clarity. When you go through the pre-approval process, you find out exactly what your budget is. This lets you focus your house hunt on homes you can actually afford, saving you a ton of time and the heartache of falling for a place that's just out of reach.

It also gives you a huge competitive advantage. An offer backed by a pre-approval is often way more appealing to a seller than a slightly higher bid from someone whose financing is still a question mark. As local real estate experts James and Nicole Isherwood often point out, having that proof of financial readiness can be the one thing that wins you a bidding war.

Key Benefits of Getting Pre-Approved

Having a pre-approval in your back pocket isn't just about getting a loan; it’s about setting yourself up for success from day one. Here are the real-world advantages you get as a homebuyer in BC.

- Budget Clarity: You’ll know the maximum amount a lender is willing to loan you. This helps you and your real estate agent zero in on the right properties right away.

- Increased Credibility: Sellers and their agents will take your offer much more seriously, knowing your financing is solid and less likely to fall through.

- Faster Closings: A lot of the financial heavy lifting is already done. That means the final mortgage approval and closing process can often move along much more quickly.

- Interest Rate Protection: Many lenders will lock in an interest rate for you for up to 120 days. This is huge—it protects you from rate hikes while you’re looking for the perfect home and gives you serious peace of mind.

A mortgage pre-approval transforms you from a casual browser into a powerful buyer. It's the strongest signal you can send to a seller that you are prepared, qualified, and ready to close the deal.

Getting pre-approved is a strategic first step. It builds a solid foundation for your entire home-buying journey. For more tips on navigating the local market, feel free to check out the latest real estate news and updates.

Gathering Your Financial Documents for Pre-Approval

Getting your mortgage pre-approval sorted out means taking a close look at your finances. Think of it like preparing your ingredients before you start cooking—getting all your documents in order first makes the whole process a lot smoother. Lenders in Canada need to be sure you can comfortably handle a mortgage, so they'll ask for some specific paperwork.

Being prepared doesn't just speed things up; it also shows your lender that you’re a serious, organized buyer. Before you even sit down with a mortgage professional, it’s a smart move to start collecting the key documents they’ll need to see.

Proving Your Income and Employment

First things first, lenders need to see that you have a steady income to cover your mortgage payments. This is the bedrock of your entire application.

If you're an employee, this usually means getting together:

- Recent Pay Stubs: Typically your last two to four pay stubs that show your year-to-date earnings.

- A Letter of Employment: A formal letter from your HR department confirming your job title, salary or hourly rate, and how long you've been with the company.

- T4 Slips and Notice of Assessment (NOA): Your last two years of T4s and NOAs from the Canada Revenue Agency give a clear picture of your income history.

If you’re self-employed or your income isn’t the same every month, lenders will want to dig a bit deeper. You'll likely need to provide a couple of years' worth of business financials and personal tax returns to show them your income is stable.

Verifying Your Down Payment and Assets

Next up, you need to show that you have the money for a down payment and the associated closing costs. This proves to the lender that you have some "skin in the game."

A crucial part of the mortgage pre-approval process is proving your down payment funds come from a legitimate source and have been sitting in your account for a little while, usually for 90 days.

You'll need to provide statements for any accounts where you're holding these funds. As you pull everything together, it helps to know how to easily obtain your bank statements to avoid any hold-ups. This includes your chequing, savings, and any investment accounts like TFSAs or RRSPs. If a family member is gifting you part of the down payment, you'll also need a signed gift letter from them.

Once you know your numbers, it's helpful to see how they translate into actual payments. To get a better handle on your potential monthly costs, play around with our mortgage payment calculator and see what your expenses might look like based on your down payment.

Navigating the Mortgage Pre-Approval Process

So, you've gathered all your financial documents and sent them off. Now the real work starts—on the lender's side. The journey from handing over your paperwork to getting that pre-approval letter in hand involves a few crucial steps, all designed to confirm your financial health and figure out what you can realistically borrow.

While the first chat with your mortgage broker or bank gets the ball rolling, it’s the formal application that really kicks off the underwriting process. One of the very first things a lender will do is pull your credit report.

Understanding the Credit Check and Underwriting

This isn’t just a quick peek at your score; it's what's known as a 'hard inquiry'. This kind of check can cause a small, temporary dip in your credit score, but it's an essential part of the process. It gives the lender a detailed history of how you’ve handled debt in the past, which is a massive piece of the puzzle for them.

With your credit report in hand, an underwriter—the person who has the final say—gets to work. They'll meticulously go through your entire financial profile, looking for one thing: assessing risk and making sure you can comfortably handle the mortgage payments you’re applying for.

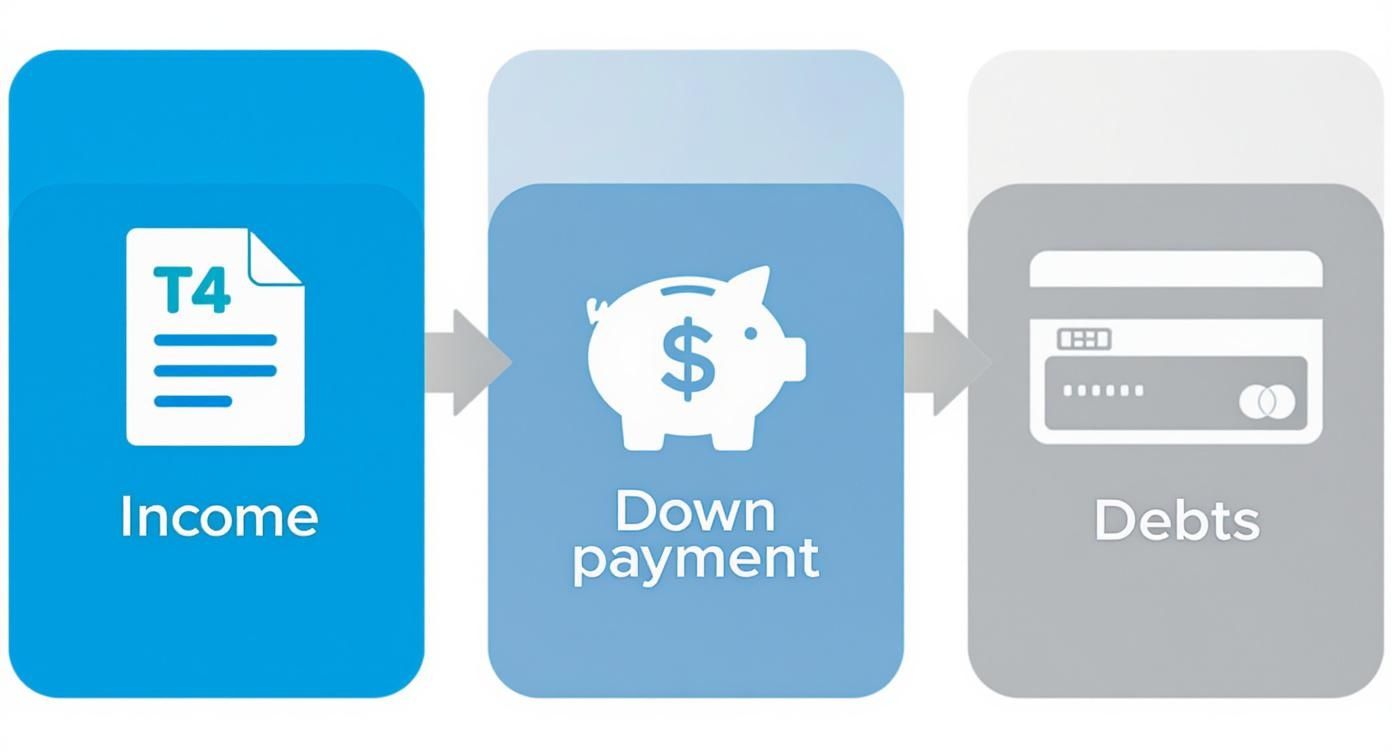

This visual gives you a good idea of the key documents underwriters look at to piece together your financial story.

This process shows how underwriters connect the dots between your income, down payment, and current debts to determine your borrowing power.

The Math Behind Your Approval Amount

Underwriters don't just go with their gut; they use specific calculations to see how your finances measure up against Canadian lending rules. Two of the most important numbers they look at are your Debt Service Ratios.

- Gross Debt Service (GDS) Ratio: This measures your potential housing costs (think mortgage principal, interest, property taxes, and heat) against your total household income before taxes.

- Total Debt Service (TDS) Ratio: This one takes it a step further. It includes all your GDS housing costs plus any other debts you have, like car payments, student loans, or credit card bills.

But that’s not all. Lenders are also required to use the Canadian mortgage stress test. This means they have to qualify you at a higher interest rate than the one you'll actually get. It’s a safety net to make sure you could still manage your mortgage if interest rates were to climb down the road.

The stress test is a critical safety measure in Canadian lending that directly impacts your final pre-approval amount. It sets a firm ceiling on your borrowing capacity based on your ability to handle higher potential payments.

After this thorough review, you’ll finally get your conditional approval letter. This document will spell out the maximum loan amount, the interest rate (which is often held for 90-120 days), and any other conditions you need to meet before the approval is finalized. It's vital to understand these terms, and if anything is unclear, it’s always smart to contact a professional for clarification.

How Your Real Estate Agent Uses a Pre-Approval

Think of a mortgage pre-approval letter as more than just a piece of paper for your lender. For your real estate agent, it's one of the most important tools they have. For experts like James and Nicole Isherwood, this single document is the starting pistol for a focused, winning strategy in the competitive Vancouver and Fraser Valley markets. It instantly shifts your house hunt from a casual weekend browse into a serious, targeted mission.

Once your budget is locked in, your agent can cut through the noise. They'll stop showing you properties that aren't a good fit and focus only on homes you can realistically afford. This precision saves a ton of time and, just as importantly, prevents the heartache of falling for a home that’s financially out of reach.

But where it really shines is when you're ready to make an offer.

Gaining a Strategic Advantage in Negotiations

In a hot market where multiple offers are the norm, walking in with a pre-approval letter attached to your bid sends a powerful message. It tells the seller you’re not just a dreamer; you’re a serious buyer who has already done the financial legwork. James and Nicole Isherwood stress that this one document can make your offer more appealing than a higher bid from someone whose financing is still a question mark. It takes a huge piece of risk off the table for the seller, pointing toward a smoother, faster closing.

That credibility is priceless. It allows your agent to negotiate from a position of strength, showing that your offer is a reliable commitment, not just a number on a page. In many ways, your pre-approval letter does the talking for you.

A mortgage pre-approval is the foundation of a strong offer. It gives your agent the leverage needed to negotiate effectively and proves to sellers that you are prepared to see the transaction through to completion.

This professional edge is a huge part of the value a seasoned agent brings. In BC's real estate world, commissions are typically structured as 7% on the first $100,000.00 and 3.5% on the balance. That fee covers this kind of expert guidance and strategic work—like knowing exactly how to use your pre-approval to help you land your dream home. It's also a key part of the dedicated work involved in providing professional residential services to both buyers and sellers.

Got Questions About Mortgage Pre-Approval in BC? We've Got Answers.

As you start getting serious about making an offer, you're probably bumping into some last-minute questions about what a mortgage pre-approval really means on the ground. It's totally normal. Getting a handle on the details is what will give you the confidence to navigate the real estate markets in Vancouver and the Fraser Valley. Let's clear up some of the most common things we hear from homebuyers across British Columbia.

How Long Does a Pre-Approval Last?

In BC, your mortgage pre-approval—and the interest rate you’ve locked in—is typically good for 90 to 120 days. Think of it as a four-month shopping window, which is usually a decent amount of time to find a place you love.

If you don't find a home within that timeframe, you'll just need to re-apply. It’s always a good idea to touch base with your lender or broker before your current one expires. They can usually make the renewal process pretty quick and painless.

Does Getting Pre-Approved Hurt My Credit Score?

Here’s the deal: when you apply, the lender does a 'hard inquiry' on your credit report. This can cause your credit score to dip by a few points, but it's a small, temporary drop. It’s just a standard part of the process.

Honestly, the impact is minimal and short-lived. The massive advantage of knowing your exact budget and being able to make a strong, confident offer far outweighs that tiny dip. Plus, Canadian credit bureaus are smart about this—they usually lump multiple mortgage inquiries within a couple of weeks into a single event, so you can shop around for the best rate without taking multiple hits.

Is a Pre-Approval a Guaranteed Mortgage?

This is a big one. No, a pre-approval is a conditional commitment, not an ironclad guarantee. The final green light depends on a few important things falling into place after your offer on a property is accepted.

Think of it this way: a pre-approval tells you what a lender is willing to lend you in principle. The final loan is always subject to the property itself checking out and your finances staying the same.

Your final approval really comes down to these things:

- A Stable Financial Picture: Your income and job situation need to stay consistent. This isn’t the time to quit your job or finance a new truck, as big changes or new debts can throw a wrench in the works.

- The Property Appraisal: The home you want to buy has to be worth what you’re paying for it. The lender will order an appraisal to make sure their investment is sound.

- Final Document Check: The underwriting team will do one last verification of all the documents you submitted.

Basically, the lender has to approve both you and the home before any money changes hands.

At Royal LePage Brookside Realty Property Management, we're here to help you move through every part of your real estate journey with total clarity. Contact us today to chat with local experts who really know the Fraser Valley market.