You look at your latest assessment, then at the house you bought years ago in Maple Ridge, and the same thought hits a lot of owners at the same time: this place isn't just where you raised your family. It's your biggest asset.

That's especially true if you've owned in West Maple Ridge for a long time, bought in Albion before prices moved up, or settled into Silver Valley when it still felt a little more tucked away. Over the years, your home value may have changed from something abstract on paper into something that could shape retirement, a move, or help the kids.

Then the uncomfortable question shows up. If you sell, how much of that gain are you keeping?

When people start searching online and get pulled into the wrong rabbit hole. They find American articles about property tax breaks or flat capital gains exclusions that don't apply in Canada. That creates confusion fast, especially for homeowners already sorting through timing, repairs, suite income, and whether now is the right time to list. If you've been following the local market, a general Maple Ridge real estate overview helps with the market side, but the tax side needs its own plain-English explanation.

In Canada, the answer usually starts with one rule: the principal residence exemption, often shortened to PRE.

Your Maple Ridge Home and a Surprising Tax Question

A lot of Maple Ridge sellers don't ask about the principal residence exemption until they're already close to making a move. They've called a realtor, maybe started clearing out the garage, maybe talked about downsizing from a detached house near Kanaka Creek into something simpler. Then someone mentions capital gains tax, and the mood changes.

That reaction makes sense. For many families, the sale of a home is the largest financial event they'll handle outside of retirement planning.

Why this question shows up late

Homeowners usually focus first on practical things:

- Timing the move: school catchments, work commutes, and whether they want to stay close to Golden Ears or move closer to shops and services

- Condition of the home: roof, paint, landscaping, suite compliance, and what buyers in their neighbourhood will notice

- Sale proceeds: mortgage payout, legal fees, and what's left to put toward the next property

Tax often gets pushed to the side until the numbers become real.

Many sellers assume, “It's my home, so it must be tax-free.” Sometimes that's true. Sometimes it's only partly true. The details matter.

In Maple Ridge, that detail often comes down to how the property was used over the years. A family home that was lived in is one thing. A home with a basement suite in Cottonwood, a temporary move for work, or a second property bought later is something else.

The practical version of the question

When clients ask me what is principal residence exemption, they usually aren't asking for a technical definition. They're really asking one of these:

| What the owner says | What they usually mean |

|---|---|

| “Do I owe tax if I sell?” | Will the gain on my home be exempt? |

| “We rented the basement for a while. Is that a problem?” | Did income use affect the exemption? |

| “We bought another place before selling.” | Which property should count as the principal residence? |

| “We moved out and kept it for a bit.” | Did a change in use create a tax issue? |

Those are everyday PRE questions. They aren't accounting seminar questions. They're kitchen-table questions from people trying to protect the value they built over time.

Understanding the Principal Residence Exemption

The easiest way to think about the principal residence exemption is this: it's a tax shield for the gain on the sale of your main home.

In Canada, the principal residence exemption is a federal income-tax rule that can reduce or eliminate capital gains tax when you sell your home. It isn't a flat dollar amount like the American rule you'll often see online. Its value depends on the years the property is designated as your principal residence, and the calculation includes a “+1” year factor according to this guide to the principal residence exemption.

What it is not

Many Maple Ridge homeowners often get tripped up.

If you search “principal residence exemption,” you'll find a lot of U.S. content about property tax relief or fixed exclusion amounts. That isn't the Canadian framework. Canadian homeowners don't use the U.S.-style $250,000 / $500,000 exclusion rule. Instead, the Canadian approach turns on designation, occupancy, and the formula used when the home is sold.

If you want to compare how other countries explain the idea of a main-residence exemption, this overview from EndureGo Tax on CGT exemptions is useful for context, but Maple Ridge sellers need to stay grounded in Canadian rules, not imported search results.

Why the formula matters

The PRE works a bit like a tax-free growth container for your primary home. If the home qualifies for all the years you owned it, the entire gain may be sheltered. If it qualifies for only part of the ownership period, the exemption is prorated.

That +1 factor matters because life isn't perfectly tidy. People buy one home before selling another. They move mid-year. They relocate and then list later. The formula was built with some room for those transitions.

Practical rule: The PRE doesn't ask, “Did you own a house?” It asks, “Was this your principal residence for the years you're claiming?”

That's why this issue matters so much in Maple Ridge. Owners here often hold property for a long time. The longer the ownership period, the more important it becomes to get the designation and planning right.

One more point. If you're comparing tax costs tied to a move, don't mix this up with other closing costs. The PRE deals with capital gains on sale. It isn't the same thing as what land transfer tax means in a real estate transaction.

Basic PRE Eligibility for Your Family Home

For the standard family home in Maple Ridge, PRE eligibility is usually straightforward. The property generally qualifies only if it's owned by the taxpayer, ordinarily inhabited during the year by the taxpayer or certain family members, and designated as the principal residence, with that designation normally made in the year of sale through the required tax reporting, as outlined in the CRA-based explanation summarized in the earlier BMO reference.

What “ordinarily inhabited” means in real life

This doesn't mean you must sleep there every night of the year. It means the property has to be your real home base.

That can include a detached house in Albion, a townhouse near Cottonwood, or a condo if that's where you reside. If your spouse, partner, or child ordinarily inhabits the property, that can also fit within the general rule.

The core checklist

Most homeowners can pressure-test their situation with a simple list:

- You owned the home: title matters. If you didn't own it, you can't designate it.

- You lived in it as a home: not a pure investment property, not just something held for resale

- You designate it properly: the PRE doesn't apply by magic. It has to be reported correctly when you sell.

Here's where local families sometimes run into trouble. They assume that because they loved the house, raised their kids there, and treated it as “the family home,” the paperwork side doesn't matter. It does.

One home per family unit per year

This rule catches more people than you'd think. A married or common-law couple can't each freely designate separate homes for the same year just because both properties feel important.

If one spouse works in the city and keeps a condo closer to work while the family lives in Maple Ridge, that doesn't automatically mean both properties can be treated as principal residences for the same year. A choice may have to be made.

If you own more than one property, the best one to designate isn't always the one you feel most attached to. It's often the one where the tax result is strongest.

For the plain-vanilla case, though, the rule is usually simple. If you owned one home, lived in it as your family home, and didn't use it in a way that changed the tax picture, the PRE often does exactly what homeowners expect it to do.

Navigating PRE Rules in Common Maple Ridge Scenarios

At this stage, the clean, simple version of the principal residence exemption starts to bend a bit.

In Maple Ridge, many owners don't just live in a home and then sell it years later without any changes. They add a mortgage helper. They move and keep the home for a while. They buy a second property before deciding which one to sell first. Those are normal decisions. They can also affect the PRE.

The CRA rules are particularly nuanced around change-in-use events and partial rentals, which are common situations for homeowners generating income. The Canadian PRE for capital gains can be partially or fully lost if part of the home is used to produce income, unless specific conditions and elections are met, as noted in the background described in this discussion of the Canadian versus U.S.-style confusion around principal residence exemptions.

Basement suite in Cottonwood or Albion

This is one of the biggest local issues.

A lot of Maple Ridge homeowners have rented a basement suite at some point. Sometimes it was to help with mortgage costs. Sometimes it was temporary. Sometimes the suite was there when they bought the home and stayed in use.

The practical takeaway is that partial rental use can complicate the exemption.

A few things usually need close review:

- How much of the home was used to earn income: a self-contained suite can create a different analysis than a spare room

- Whether there was a real change in use: the tax treatment can shift if part of the property became income-producing in a meaningful way

- What records exist: dates, floor plans, rental history, and expense records all matter later

You moved out and rented the whole house

This happens often when a family buys another property first, relocates for work, or wants to wait for stronger sale timing.

Once the whole property stops being your home and starts being a rental, the file gets more technical. Owners should ask about change in use and whether any election may be available. The 4-year election rules can be relevant in some temporary rental situations, but they aren't something to guess at casually.

A short period of renting after you move out doesn't always destroy the PRE. But assuming you're safe without checking is where people get hurt.

You own two properties at the same time

A very Maple Ridge version of this is a family home here and a smaller property elsewhere for work or family reasons.

When that happens, the issue isn't just “Which one did we live in more?” The issue is which property should be designated for which years to produce the best result. The answer can depend on occupancy history, expected appreciation, and sale timing.

A local sale strategy matters too. If you're preparing to list a property with one of these complications, the timing and positioning of the sale should be coordinated early, not after photos are booked. A practical Maple Ridge home-selling plan should sit beside your tax conversation, not after it.

Quick scenario check

| Scenario | PRE risk level | Why |

|---|---|---|

| Long-time family home with no rental use | Lower | Usually the cleanest claim |

| Home with basement suite | Moderate | Partial income use may affect the exemption |

| Former home turned full rental | Higher | Change-in-use rules may apply |

| Two homes owned in overlapping years | Higher | Designation decisions become strategic |

How the PRE Calculation Works in Practice

The formula matters most when ownership wasn't perfectly simple. The basic idea is that the exemption is tied to the capital gain and adjusted by the years the home is designated as your principal residence relative to the years you owned it, with that extra +1 year factor built in.

Example one with a straightforward family home

A family buys a detached home in West Maple Ridge and lives there the whole time they own it. They don't rent part of it out. They don't convert it to an income property. When they sell, they designate it as their principal residence for the years they owned it.

In that kind of file, the PRE often shelters the full gain because the designation years and the ownership years line up in the cleanest possible way.

That's the version one generally expects when first inquiring about what is principal residence exemption. For a standard owner-occupied home, that expectation is often correct.

Example two with partial rental history

Now take a more mixed scenario.

A homeowner buys a detached property in Maple Ridge and lives upstairs while renting a basement suite for part of the ownership period. At sale time, the gain may not be treated the same way as in the first example, because a portion of the property may have been used to earn income.

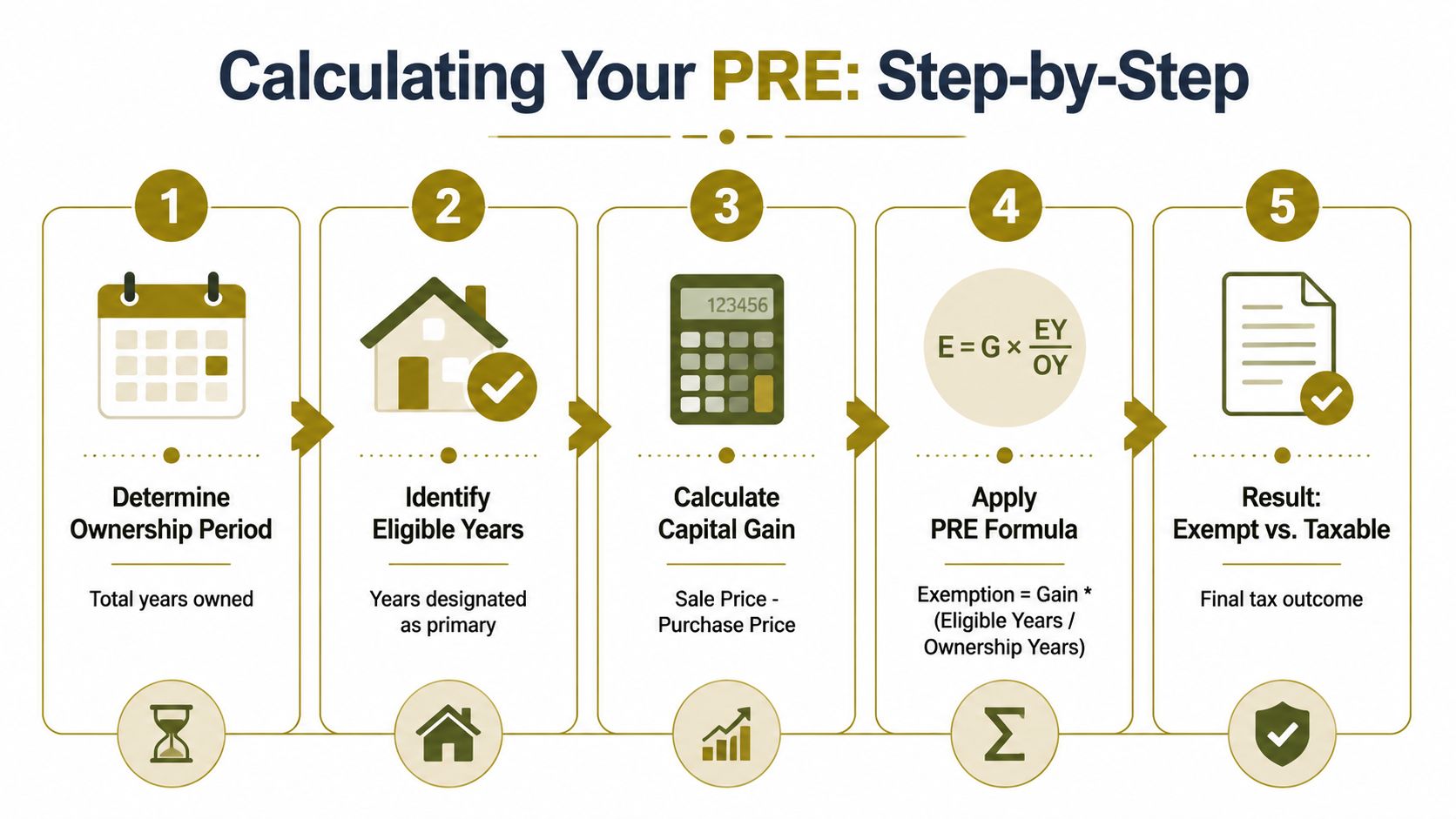

The practical calculation process looks like this:

Work out the ownership period

Count the years the property was owned.Identify the years that can be designated

This is where occupancy history and use matter.Calculate the capital gain

Sale price minus purchase price, adjusted by the normal tax framework and supporting records.Apply the PRE formula

The exempt portion is prorated using the designated years relative to years owned, with the +1 factor included in the Canadian formula.Separate exempt and non-exempt portions

If part of the gain isn't sheltered, that's the part your accountant will focus on.

The biggest mistake sellers make with PRE math isn't arithmetic. It's assuming the property use history is simpler than it really was.

Why the numbers on paper can still mislead you

Two homes can sell for the same amount and produce very different tax outcomes. The difference often comes from use, not price.

That's why I tell Maple Ridge sellers to compare tax value, assessed value, and real market value carefully, but not to confuse any of them with the PRE analysis. If you want a cleaner handle on the pricing side before you layer in tax questions, it helps to understand assessment versus market value.

Reporting the Sale and Smart Planning Tips

Even if the entire gain is exempt, the sale of a principal residence still needs to be reported on your tax return. That surprises people.

For many sellers, the assumption is simple: if there's no tax owing, there's nothing to report. That isn't how this works.

What usually needs to be filed

Canadian homeowners commonly hear about:

- Schedule 3: where the disposition is reported

- Form T2091: used for the designation of a property as a principal residence by an individual when required

Your accountant should tell you exactly what applies to your file, but the important point is that the reporting step is part of the claim. Don't treat it as an afterthought.

Records worth keeping before you sell

A strong PRE file is usually built long before the listing goes live.

Keep records for things like:

- Purchase documents: statement of adjustments, legal paperwork, and completion records

- Capital improvements: invoices for renovations that may affect your adjusted cost base

- Occupancy history: when you moved in, moved out, or changed how the home was used

- Rental records: suite start dates, lease periods, and any documents showing which portion of the property was rented

If you've read U.S. tax material while trying to understand home sale rules, you've probably noticed similar planning themes around documentation and timing. For broad comparison only, this piece on San Diego home sale tax insights shows how often sellers in other markets face the same problem of not gathering records until it's too late. The legal rules are different, but the planning lesson is familiar.

A seller's planning checklist

Before listing, I'd strongly suggest this sequence:

Talk to a tax professional early

Especially if there was a suite, a move-out period, or another property involved.Build a simple timeline

Note when you bought, lived in, rented, moved, and sold.Pull your documents together before the rush

It's easier to find invoices and tenancy records before offers start coming in.Coordinate the sale strategy with the tax strategy

Price, timing, possession, and even whether to list now or later can all intersect with the bigger picture.

If you want a broader plain-English look at the tax side of selling, this guide on selling a home and capital gains is a helpful companion to the PRE conversation.

Protecting Your Investment in Maple Ridge

The principal residence exemption is one of the most valuable tax rules available to Canadian homeowners. For many Maple Ridge sellers, it can shelter all of the gain on the family home. But it works best when the ownership story is clean, the records are organized, and the reporting is handled properly.

Where people get into trouble is rarely the basic family-home scenario. It's the in-between situations. The basement suite that felt informal. The temporary move that lasted longer than expected. The second property that changed which home made the best designation choice.

That's why this topic deserves more than a quick online search. Generic articles often answer the wrong question, especially when they drift into U.S. property tax rules or fixed dollar exclusions that don't apply here. Maple Ridge owners need a local, practical lens.

This article is general information, not personal tax advice. The right next step is usually twofold. Speak with a qualified tax professional about your exact facts, then work with a local realtor who understands how sale timing, neighbourhood demand, suite history, and property positioning all fit together in a real transaction.

If you're thinking about selling in Silver Valley, West Maple Ridge, Albion, Cottonwood, or Kanaka Creek, getting clear on the PRE before you list can protect far more than your paperwork. It can protect the value you built in the home itself.

If you're planning a move in Maple Ridge or Pitt Meadows and want practical guidance on timing, pricing, and preparing your home for a smooth sale, Royal LePage Brookside Realty Property Management can help you build a strategy that fits your property, your neighbourhood, and your next step.