You hear that the Bank of Canada has cut rates, then your mind goes straight to the practical stuff. Can we finally afford that townhouse near Albion? Will a detached home in Kanaka Creek feel less out of reach? If we list our place in Cottonwood this spring, are more buyers going to show up?

That reaction is normal. Most Maple Ridge buyers and sellers don't care about the policy headline itself. They care about the next step. Their payment, their approval amount, their competition, and whether their own street will feel any different in the next few months.

That's where national coverage often falls short. It tells you rates are down, but it doesn't tell you what that means if you're trying to stay close to Samuel Robertson Technical, hoping for something walkable to downtown Maple Ridge, or debating whether Silver Valley is worth stretching for.

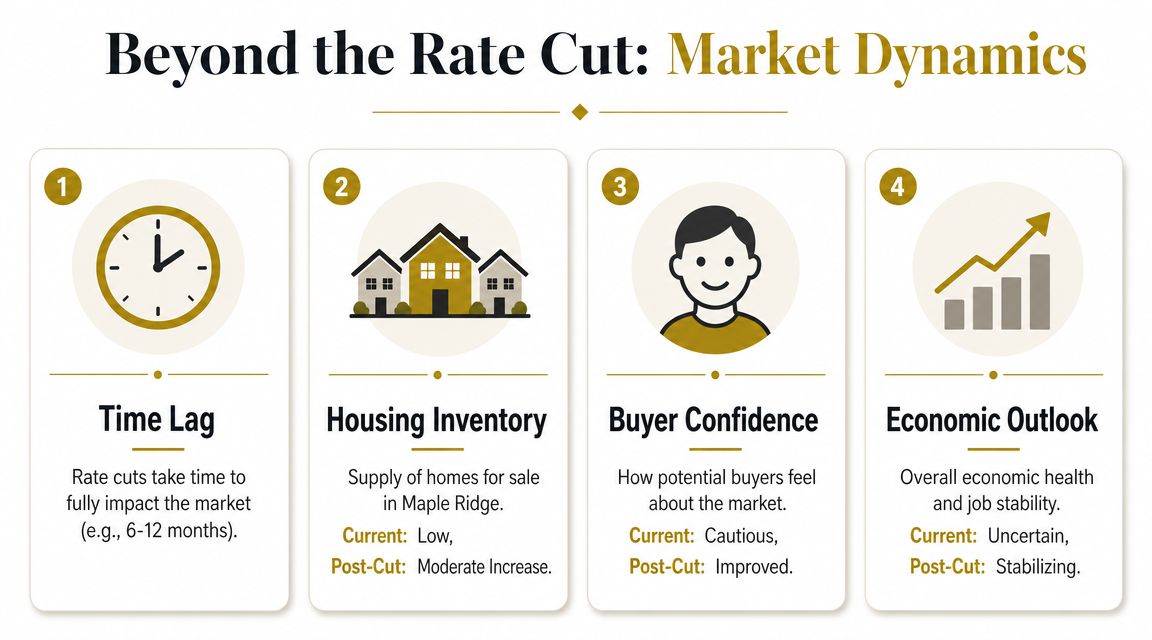

The short version is simple. Bank of Canada rate cuts usually affect Maple Ridge through affordability first. Prices often react later, and sometimes they barely react at all unless lower rates stick around long enough to change buyer behaviour.

What Bank of Canada Rate Cuts Mean for Your Wallet

A Maple Ridge rate cut story usually starts at the kitchen table. You open a mortgage app, plug in a lower rate, and ask a simple question. Does this change what we can comfortably buy in the neighbourhood we want?

That first impact is usually your monthly payment and, in some cases, your approval range. Buyers looking at Silver Valley, Albion, or West Maple Ridge often feel the difference there before they see much change in asking prices on their street. Lower rates can improve the monthly math, but the stress test still sets limits, so a better headline does not always translate into a dramatically bigger budget.

What matters in practice is timing. A cut can make ownership feel more manageable before it changes seller expectations. In Maple Ridge, that gap matters. If more buyers can carry the payment on a townhouse near schools or a lower-priced detached home with a yard, competition can pick up in those segments first while other parts of the market stay fairly steady.

What buyers usually notice first

Buyers usually notice breathing room, not bargains.

A lower borrowing cost can bring hesitant buyers back into the market, especially people who were close to qualifying or were uncomfortable with the monthly payment. That often shows up fastest in entry-level price bands, where a small payment change can decide whether someone keeps renting or starts writing offers.

Neighbourhood choice can shift too. A buyer who had been comparing a farther-out option with central Maple Ridge may decide the shorter commute or preferred school catchment is now within reach. On the ground, that does not mean every home type moves the same way. A newer townhouse in a popular pocket can react differently than an older detached property that still needs a roof, windows, or drainage work.

Practical rule: A rate cut can improve your monthly carrying cost. It does not remove inspection issues, strata rules, or financing conditions.

If you own a rental or are comparing a purchase against holding an investment property, it also helps to review local Maple Ridge landlord resources and property management guidance before assuming lower rates automatically improve your numbers.

What sellers should take from this

Sellers usually benefit first from stronger buyer confidence, not an instant price jump. More showings, more second looks, and fewer buyers sitting on the sidelines often come before any clear change in sale prices.

That lag is why pricing still matters. If your home in Cottonwood or Hammond is listed above where buyers see value, a rate cut will not fix that on its own. It may increase the pool of interested buyers, but condition, presentation, and neighbourhood supply still shape the result.

For buyers, lower rates should never crowd out due diligence. Before writing on an older detached home in Maple Ridge, it helps to review an essential Vancouver house checklist so a better payment does not distract you from repair costs that can change the full budget fast.

From Ottawa to Your Mortgage The Rate Cut Effect

The easiest way to understand a rate cut is to think of it as water moving through a series of gates. Ottawa opens the first gate. Your lender and the mortgage market decide how much of that water reaches your payment.

Variable rates move first

The Bank of Canada sets the overnight rate on fixed announcement dates. That overnight rate affects short-term borrowing costs, which feed into lender prime rates and then into variable-rate mortgages. The Bank outlines that transmission in its explanation of the key interest rate and monetary policy framework.

For Maple Ridge buyers, that means a variable mortgage can respond faster than a fixed one. If the cut is meaningful enough to lower the rate you're offered, your monthly payment may improve sooner than buyers in a fixed product expect.

A related concept shows up in U.S. commentary too. If you want a simple cross-border explainer on how central-bank decisions influence borrowing costs, this piece on understanding Fed impact on rates is a useful companion read.

Fixed rates are slower and less direct

Fixed mortgage pricing doesn't directly copy the Bank of Canada announcement. It moves through lender pricing and bond-market expectations. That's why some buyers hear “rates were cut” and then wonder why their fixed quote didn't drop much.

In practical terms, a 25-basis-point cut can lower qualifying rates for some buyers and slightly increase purchasing power, but the price effect is often muted unless the cut is sustained and paired with stronger employment and consumer confidence, according to the Bank of Canada policy framework noted above.

Lower rates matter most when they change what buyers can actually qualify for and feel comfortable carrying, not when they create a good headline.

Here's the bigger local point. Even if borrowing costs improve, a buyer in Maple Ridge still has to decide between products, neighbourhoods, and timing. A detached home in a school-focused pocket near Kanaka Creek Elementary may draw a different crowd than a townhouse closer to transit and shopping.

For owners and investors who want broader housing context beyond just resale purchases, Brookside also keeps practical market material in its landlord resources, which can help frame financing decisions against local rental and ownership considerations.

A short visual version of the same chain helps if you prefer seeing the mechanics laid out:

What Different Rate Cuts Mean for Your Buying Power

In Maple Ridge, buyers rarely ask about basis points for long. They ask a much simpler question. “Does this move me into a different kind of home?”

That's the right lens. A small cut may not transform your options, but it can change whether a purchase feels tight or manageable. Expert commentary has noted that a 25-basis-point cut can move some variable rates down to about 3.74% and let borrowers qualify for a slightly larger mortgage, increasing buying power at the margin, while the biggest price response tends to come when cuts are unexpected or part of a broader easing cycle (reference).

Three practical scenarios

Instead of pretending every cut has the same effect, it helps to think in ranges.

| Rate Cut Scenario | Example Mortgage Rate | Monthly Payment | Increase in Buying Power |

|---|---|---|---|

| Mild cut | Slightly lower than before | Modest relief | Marginal increase |

| Moderate easing cycle | Noticeably lower than before | More comfortable monthly carrying cost | Enough to widen options in some segments |

| Significant easing cycle | Materially lower than before | Stronger payment relief | Can move some buyers into a different property tier |

That table is intentionally qualitative because monthly payment and buying power depend on your down payment, income, debt ratios, and mortgage product. There isn't one universal Maple Ridge answer.

Where the extra flexibility shows up

In real life, a mild cut may not move you from a condo to a detached home. What it can do is reduce pressure enough that you're no longer shopping at the absolute top of your approval.

That matters more than people think. Buyers who stop stretching to the limit usually make better decisions on inspection risk, renovation budget, and location. They're less likely to compromise on a busy road, awkward floor plan, or deferred maintenance just to stay within payment comfort.

A moderate series of cuts is where choices can start to shift more visibly. That might mean:

- Townhouse buyers step into stronger complexes: Better monthly affordability can make a better-run strata or more desirable school catchment realistic.

- Detached buyers expand neighbourhood options: Instead of ruling out Cottonwood or parts of West Maple Ridge immediately, some buyers may keep those areas on the shortlist.

- Move-up households regain confidence: Owners with existing equity may feel less pinched when trading from a starter property into a family home.

The biggest mistake I see is treating a rate cut like permission to spend every extra dollar a lender will approve.

If you want to test your own payment range before you shop, use a proper mortgage payment calculator. It's one of the fastest ways to turn a rate headline into a real buying decision.

A Neighbourhood Look at Rate Cut Impacts in Maple Ridge

A rate cut won't hit every part of Maple Ridge the same way. The effect depends on who typically buys there, what kind of homes are available, and how tight inventory feels in that pocket.

National affordability commentary points in a useful direction here. Lower rates improve monthly payment capacity and tend to support demand first in rate-sensitive segments like first-time buyers, townhomes, and lower-priced detached homes, with mortgage payment-to-income metrics improving in Q4 2025 across 6 of 10 Canadian centres, falling 0.4% quarter over quarter in that group according to the housing forecast summary from True North Mortgage (reference).

Central Maple Ridge and Albion

These areas often catch buyers who need a practical entry point. They want access to schools, shopping, parks, and day-to-day convenience, but they still need the numbers to work.

That's why a lower-rate environment can matter here early. Townhome and condo buyers are usually more payment-sensitive. If financing gets a little easier, this segment can wake up faster than the higher-end detached market.

Albion also attracts young families because the housing mix offers a lot of “next step” options. Buyers who were stuck renting or trying to move up from a condo may re-enter here before they jump into more expensive detached pockets.

Kanaka Creek and Cottonwood

These neighbourhoods often appeal to buyers who are balancing school catchments, yard space, and a longer-term family plan. They're not just shopping a payment. They're shopping a lifestyle.

A lower rate can help these buyers qualify a bit more comfortably, but they usually move when two things line up. They need borrowing costs to feel manageable, and they need confidence that they'll still have room in the budget for childcare, activities, commuting, and upkeep.

If demand rises while listings stay lean, these family-oriented detached segments can feel the pressure quickly. If more owners decide to list at the same time, the extra demand can get absorbed without dramatic price movement.

Silver Valley and new construction pockets

Silver Valley behaves a little differently because buyers there often compare resale against newer homes. Financing costs can shape those decisions more directly.

When borrowing improves, some buyers become more willing to pay for newer layouts, modern finishes, and the trail-access lifestyle that draws people to the area. But they also tend to be selective. A rate cut may bring them back into the market, not remove their concern about lot size, slope, privacy, or long-term resale.

West Maple Ridge

West Maple Ridge covers a wider mix of property types and buyer intentions. Some households want larger lots and established streets. Others are looking at commute convenience or long-term redevelopment potential.

That means demand here can be less uniform. Lower rates may help, but buyer behaviour often depends on the specific product. A well-located family home near parks and commuter routes may respond differently than an older property needing major updates.

If you're comparing larger-lot and established-home options, this local guide to West Maple Ridge gives helpful neighbourhood context that broad market articles usually miss.

The Real Story Timing Inventory and Market Sentiment

It's often assumed that a rate cut should push prices up right away. In Maple Ridge, that's usually not the first thing that happens.

The first shift is often activity. More inquiries. More showings. More buyers who stop “just watching” and start booking appointments. Price movement can come later, and sometimes it doesn't come much at all if listings rise at the same time.

Recent Canadian commentary has highlighted that there is a lag between rate cuts and Maple Ridge price effects, and that the key local question is whether prices move first or sales volume moves first. It also notes the Bank of Canada policy rate was down to 2.25% by April 2026 after cuts in 2025, while local impact still depends on whether turnover, multiple offers, or listings increase first (reference).

What usually changes first

Sales volume often reacts before benchmark pricing does. Buyers who had been paused by payment anxiety start testing the market again. They write offers more confidently. They stop waiting for the “perfect bottom.”

Sellers react too. Some see lower rates as a better window to list. Others hold back because they expect stronger prices later. That push and pull matters more than the announcement itself.

Inventory can cancel out the pressure

If lower rates bring in more buyers but also bring in more listings, the result may be a steadier market instead of a hot one. That's why watching active inventory matters as much as following the Bank of Canada schedule.

A balanced rise in both supply and demand can keep pricing fairly contained. On the ground, that can look like homes selling faster without necessarily selling much higher.

Don't judge the Maple Ridge market by the rate cut alone. Judge it by the mix of new listings, accepted offers, and whether buyers start competing on the same homes.

Market sentiment is local

Sentiment in Maple Ridge doesn't always match national headlines. A cautious buyer in central Maple Ridge may still move quickly if a clean, well-priced townhouse comes up near the right school. A detached buyer in Silver Valley may still pause if they're worried about job stability or renewal timing.

What I'd watch most after a cut is this:

- Turnover: Are homes moving faster than they were a few months ago?

- Offer behaviour: Are buyers putting in cleaner offers or more aggressive subjects?

- Listing response: Are more owners stepping in, or are good homes still scarce?

- Neighbour comparisons: Are Maple Ridge conditions tracking nearby Fraser Valley communities, or diverging?

If you want current local housing updates rather than broad national summaries, Brookside's news section is one place to monitor market-facing updates tied to Maple Ridge and Pitt Meadows.

Your 2026 Game Plan for Buying and Selling in Maple Ridge

A lot of 2026 decisions in Maple Ridge will come down to timing.

A buyer in Albion may feel a rate cut in their monthly payment before they feel it in local prices. A seller in West Maple Ridge may hear more optimism from buyers, then wait weeks or months before that turns into stronger offers on their street. That lag matters. It is often the difference between buying early with less competition and waiting until more buyers have returned.

That is the practical takeaway for 2026. Rate cuts usually show up in affordability first, then in buyer confidence, and only later in sale prices if inventory stays tight in the neighbourhood you are watching.

If you're buying

Lower rates help your monthly math, but they do not fix overpaying or choosing the wrong location. Buyers who make good decisions in Maple Ridge usually know their ceiling, their preferred neighbourhoods, and the type of compromise they will accept before the market speeds up.

A good plan looks like this:

- Sort out your full budget early: Know your pre-approval amount, your monthly comfort level, closing costs, and the repair buffer you want to keep after possession.

- Track the neighbourhood, not just Maple Ridge as a whole: A townhouse in central Maple Ridge, a detached home in Silver Valley, and a family home near Albion schools can react differently to the same rate cut.

- Buy for the next five years, not the next headline: A better payment today does not help much if the layout, commute, or lot size stops working a year from now.

- Stay selective on condition: Lower borrowing costs do not make a weak strata, an aging roof, or poor renovation work any cheaper to own.

For buyers who want a practical overview before they start touring homes, Brookside's guide to buying a home in Maple Ridge is a useful starting point.

If you're selling

Sellers should treat rate cuts as a chance to meet more qualified buyers, not as permission to overprice. In Maple Ridge, buyers still compare block by block, and they notice quickly when a home is priced ahead of recent sales.

Three things usually matter most:

- Price for the market that exists now: If your area has more showings but no offer pressure yet, the right list price still matters more than the rate headline.

- Prepare the home properly: Clean presentation, solid photos, and obvious maintenance updates help buyers feel confident, especially when they are stretching on budget.

- Watch your listing window closely: Some neighbourhoods get a short period where demand improves before listings catch up. That window can be useful, but it does not last in every pocket of Maple Ridge.

If you're investing

Investors need to be more careful than the headlines suggest. Lower rates can improve cash flow on paper, but the actual decision still depends on rent levels, vacancy risk, strata bylaws, maintenance exposure, and the kind of tenant the property is likely to attract.

Royal LePage Brookside Realty Property Management is one local option that handles Maple Ridge and Pitt Meadows real estate and property management. That can help if you are weighing a purchase as both an investment property and a future resale.

The better question is not whether rates might drop again. It is whether you are ready if the right property shows up before the rest of the market reacts.

For 2026, the smartest approach is local and specific. Buyers should watch how quickly good listings disappear in their target area. Sellers should watch competing inventory on streets buyers cross-shop. On one street, a rate cut may bring more second showings within two weeks. On another, it may take a full season before pricing changes at all.

If you're trying to figure out what lower rates mean for your own move in Maple Ridge, whether that's buying in Albion, selling in West Maple Ridge, or weighing your options in Silver Valley, Royal LePage Brookside Realty Property Management can help you look at the local numbers, your likely competition, and the timing that makes the most sense for your next step.