The cost of home insurance in BC is on the rise, and if you're a homeowner in Vancouver or the Fraser Valley, you've probably noticed. It’s not just you. Understanding what’s pushing your premiums up is the first step to getting a handle on them and making sure your biggest asset stays protected.

Why BC Home Insurance Costs Are Rising

Owning a home in British Columbia comes with its share of expected costs, from the mortgage to property taxes. Lately, though, it’s the home insurance bill that’s causing a lot of homeowners to raise their eyebrows. If you feel like your annual premium is climbing faster than ever, you're right. These hikes aren't random; they're a direct response to a perfect storm of economic and environmental pressures hitting the entire province.

Think of your insurance policy as a high-quality financial raincoat. When the storms—like inflation, wildfires, and floods—get stronger and more frequent, the cost of making that raincoat goes up for everyone. Several major factors are driving this trend, making it more expensive for insurers to provide the coverage we all depend on.

The Main Drivers Behind Higher Premiums

For anyone owning a home in communities like Vancouver and the Fraser Valley, a few key forces are pushing costs upward. As real estate experts James and Nicole Isherwood often point out, being aware of these factors helps homeowners and buyers anticipate their long-term costs of ownership.

Here are the big ones:

- Soaring Construction Costs: The price of everything needed to build a house—from lumber and steel to drywall—has shot up. Combine that with a shortage of skilled tradespeople in the Lower Mainland, and the cost to repair or completely rebuild a home after a disaster is significantly higher than it was just a few years ago.

- Increased Frequency of Natural Disasters: British Columbia has been hit hard by a growing number of catastrophic events, especially wildfires and floods. The 2021 Abbotsford floods, for instance, caused an estimated $675 million in insured damages, highlighting the immense financial risk in the Fraser Valley. These events result in massive payouts, and insurance companies have to adjust premiums province-wide to cover this new level of risk.

- Global Economic Pressures: Things like supply chain backlogs and general inflation have a ripple effect. They drive up the replacement cost of everything inside your home, from your sofa to your kitchen appliances. Your policy has to cover these higher values, which in turn pushes up your premium.

Understanding these underlying trends is crucial for any homeowner. As real estate professionals, we see firsthand how these external factors impact the total cost of ownership. It's about more than the purchase price; it's about being prepared for all associated expenses. - James and Nicole Isherwood

This new reality means homeowners need to be more proactive. By understanding why your costs are rising, you can start looking for smart ways to keep your coverage affordable without sacrificing protection. For more insights on local property trends, feel free to check out the latest updates on our real estate news blog.

Before we get into savings strategies, let's break down these cost drivers in a quick-reference table.

Key Drivers of BC Home Insurance Costs at a Glance

The table below summarizes the primary factors pushing home insurance premiums up across British Columbia. Recognizing how these elements connect can give you a clearer picture of the current insurance landscape.

Seeing these factors laid out makes it clear that rising premiums are a response to real-world risks and costs that affect the entire province, not just individual homeowners.

How Inflation Impacts Your Insurance Premiums

When your home insurance renewal arrives with a higher price tag, it’s natural to wonder why. The answer often has less to do with your specific property and more to do with the broader economic picture in British Columbia, especially inflation. This isn't just about the rising cost of groceries; it’s about the very real, and very expensive, cost to rebuild your home from scratch after a disaster.

Think of your policy as a contract to make you whole again. If a fire destroys your house, the insurance company is on the hook to rebuild it. But if the price of lumber, drywall, and labour has shot up since you bought the policy, the cost of fulfilling that promise has also increased.

This is the economic reality forcing insurers to adjust their rates. They have to price their policies to cover the actual expense of rebuilding in today’s market, not yesterday's. It's the main reason that figuring out the home insurance cost BC homeowners are facing means looking at the province's economic health.

The Rise of Construction Costs

One of the biggest drivers behind your premium is the soaring cost of construction materials and labour in BC. Over the last couple of years, we've seen supply chain headaches and massive demand send prices for essentials like lumber, steel, and roofing through the roof.

On top of that, there's a serious shortage of skilled tradespeople in places like Vancouver and the Fraser Valley. When there aren't enough electricians, plumbers, or carpenters to go around, their wages naturally climb. So, both the materials and the people needed to fix or rebuild your home are now a lot more expensive.

Your insurance isn't just covering a building. It's covering the cost to rebuild that building at future prices. When the cost of construction jumps, your coverage has to keep pace, or you risk being underinsured.

Insurers have no choice but to base their pricing on these inflated costs. If your policy’s coverage limit doesn't match the current price of rebuilding, you could be left with a huge financial gap if you ever have to file a total loss claim. This is a massive factor behind the steady rise in premiums we've been seeing.

Understanding Home Replacement Cost Output Inflation

This brings us to a more specific term you might hear: Home Replacement Cost Output Inflation. It’s a mouthful, but the concept is simple. It isn't the general inflation rate you see on the news; it's a laser-focused metric that tracks price increases only for the goods and services used to build a house.

In British Columbia, this specific type of inflation has been a huge deal. It bundles together things like:

- Building Materials: The price of wood, concrete, drywall, and wiring.

- Labour Wages: The hourly rates for skilled tradespeople.

- Equipment Costs: The expense of renting or buying machinery for a build.

- Permits and Fees: The charges from municipalities for any rebuilding project.

When you add all that up, you get an inflation rate within the construction industry that's often much higher than the general economy's. This is why your home insurance premium might see a big jump even if overall inflation seems manageable. For example, a recent Canadian analysis showed that home insurance premiums in BC went up by an average of 5.89% year-over-year, outpacing Canada's general inflation rate. You can dig deeper into these numbers by checking out the full report on rising insurance rates.

Because of this, insurers are constantly recalibrating their models to make sure the coverage they offer is actually enough. The premium you pay is a direct reflection of this new reality—the true, inflated cost of putting things right after a loss.

The True Cost of Rebuilding Your BC Home

One of the biggest misunderstandings homeowners have is mixing up their home's market value with its replacement cost. It’s an easy mistake to make, but these two numbers tell completely different stories.

Your insurance policy isn’t designed to buy you a similar house down the street if disaster strikes. It’s there to rebuild your house, on your lot, from the ground up.

Think about it this way: your home’s market value is what someone would pay for it today—land, location, and curb appeal included. The replacement cost? That’s the bill for tearing down what’s left, hauling away the debris, and reconstructing your entire home with today's materials at today's labour rates. They are two very different beasts.

This single distinction is the key to understanding your home insurance cost in BC. Insurers aren't looking at real estate listings; they're calculating the staggering cost of a total rebuild, and that figure has been climbing fast across the province.

Why Replacement Cost Is Not Market Value

The real estate markets in Vancouver and the Fraser Valley are famously volatile, swinging with interest rates and buyer demand. The cost to actually build a house, however, is on a steady, relentless march upward, completely separate from property sale prices.

A huge piece of the puzzle is that your land—often the most valuable part of your property—isn't insured against things like a fire. Your policy is all about the structure itself.

That means your insurance costs are driven by real-world construction expenses, like:

- Debris Removal: Before a single nail can be hammered, the entire site has to be cleared. This is a messy, expensive job that people often forget to factor in.

- Modern Building Codes: If your home is a few decades old, it can't just be rebuilt as it was. It has to meet all of today's much stricter BC building codes, which can mean pricier materials and entirely new systems for plumbing and electrical.

- Skilled Labour Demand: As we've touched on, finding qualified tradespeople in the Lower Mainland and Fraser Valley is tough. High demand means high wages, which directly inflates the cost of any construction project.

“A home’s insured value can increase even when the real estate market is flat or declining. Homeowners need to understand that their policy is protecting them against construction costs, not market fluctuations. This is a crucial detail many overlook.”

This is why your premiums can keep climbing even if your property's assessed value doesn't budge. The insurance company is pricing the real-world risk of building materials and labour. A great first step is getting a handle on your home's current market value, which you can do with a free home evaluation to see one side of the equation.

BC-Specific Factors Driving Up Rebuild Costs

Here in British Columbia, the price tag for rebuilding is heavily influenced by our local economy. In fact, one of the biggest drivers of premium hikes is something called Home Replacement Cost Output Inflation—a metric that tracks just how fast construction costs are rising.

Since 2019, BC has been hit with major increases in both building materials and labour wages, far outpacing general inflation. Supply chain headaches and a shortage of skilled workers in the Vancouver area and Fraser Valley are the main culprits.

Rebuilding your home today is a lot like ordering a custom suit. The price isn't just about the fabric; it's the specialized skill and time of the tailor. In BC, both the "fabric" (materials) and the "tailor" (skilled labour) are getting more expensive by the day.

When you're figuring out what it would really cost to rebuild, it's critical to have a firm grip on your coverage, which means understanding insurance policy limits. These limits are the maximum your insurer will pay out. Making sure they reflect today's sky-high rebuilding costs is your best defence against a financial nightmare.

Your Location Matters for Insurance Rates

When it comes to your home insurance cost in BC, your postal code packs a serious punch. An insurer's job is all about calculating risk, and that risk profile can change dramatically from one neighbourhood to the next. The difference between living in a dense Vancouver community versus a sprawling part of the Fraser Valley is night and day from an insurance perspective.

Think of it like this: the odds of a car accident are wildly different on a quiet country lane compared to a bustling downtown intersection. It’s the same idea with your home. The unique geography, climate patterns, and urban realities of your location directly shape your annual premium.

Two homes of the exact same size and value can have completely different insurance costs, simply because one is sitting in a high-risk zone for something like an earthquake or flood, while the other isn't. This is why your address is a cornerstone of the entire insurance calculation.

Vancouver vs Fraser Valley Risk Profiles

The Lower Mainland provides a perfect case study in how geography dictates risk. The City of Vancouver and the communities spread throughout the Fraser Valley might be close on a map, but they present entirely different challenges for insurers.

Vancouver’s primary risks are tied to two things: urban density and seismic vulnerability. The city is smack-dab in a high-risk earthquake zone, a fact that every insurance provider bakes into their premiums for properties there. On top of that, buildings are packed tightly together, which increases the risk of fire spreading from one home to another. Older infrastructure in some neighbourhoods can also lead to a higher chance of issues like sewer backups.

The Fraser Valley, on the other hand, is dealing with a different set of threats. Its beautiful, wide-open landscape also contains major floodplains, especially near the Fraser River. It also has a much larger wildland-urban interface—that’s the zone where residential areas butt up against forested land. This dramatically increases the risk of wildfire damage, particularly during our dry summers.

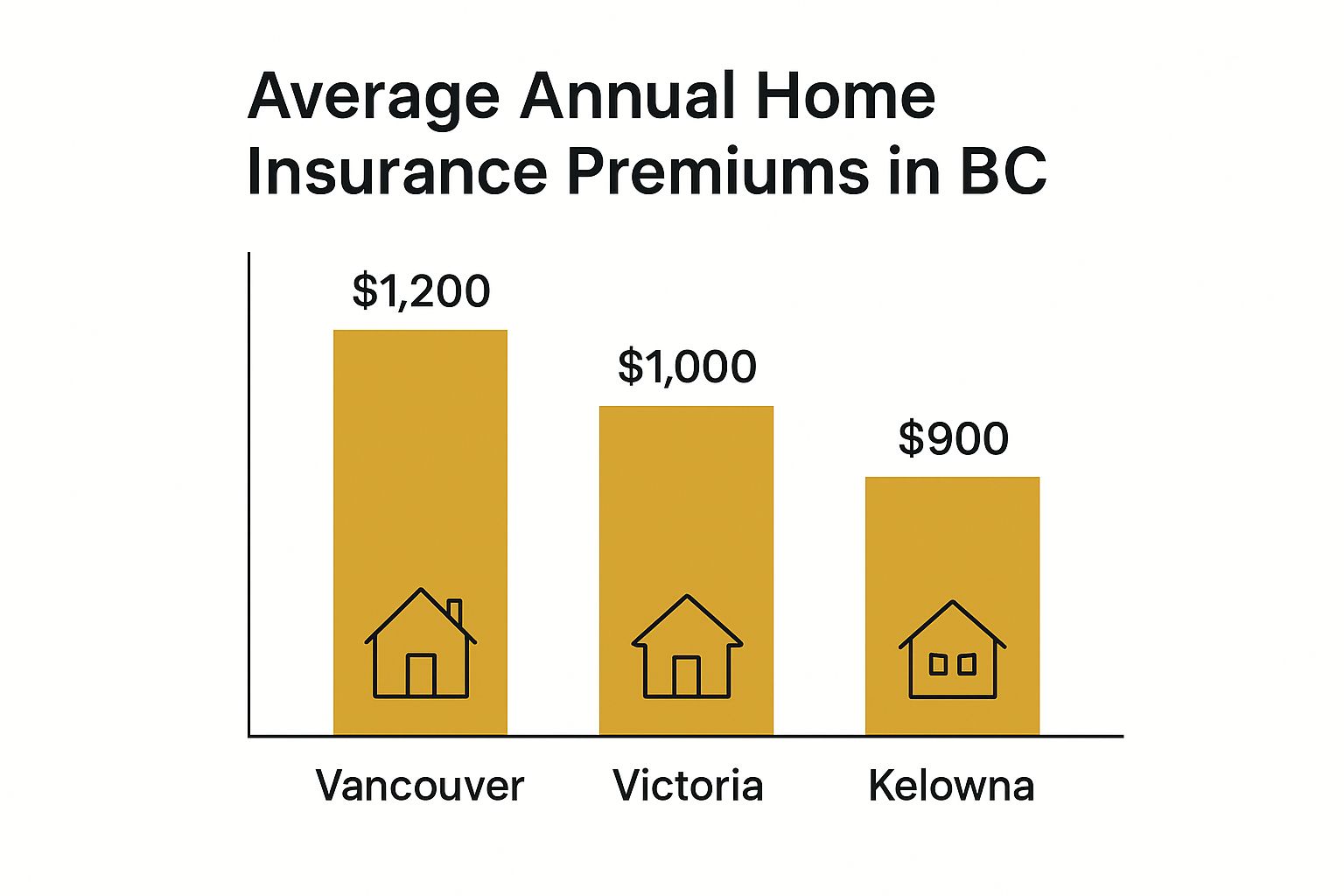

This brief chart shows how average premiums can differ across key BC cities based on their unique risk profiles.

As you can see, cities with different exposures—like the seismic risk in Vancouver and Victoria versus the wildfire risk near Kelowna—often see very different average premiums as a result.

How Property Type and Location Intersect

The specific type of property you own also gets layered on top of its location to create an even more detailed risk profile. For example, a brand-new single-family home in a Fraser Valley subdivision might face a higher wildfire or flood risk, but it probably has a lower risk tied to aging city pipes compared to a century-old home in Vancouver.

"When we help clients search for a new home, understanding these localized risks is a key part of the conversation. A property's location can have long-term financial implications that go far beyond the mortgage, directly impacting insurance costs and resale value." - James and Nicole Isherwood

As local real estate agents, James and Nicole Isherwood always stress that a property's appeal is about more than just its features; its geographical context is critical. Knowing these details is a vital part of the process when you are buying a home in the region, as it helps you anticipate what your future costs will look like. An expert can point out if a property is in a known floodplain or an area with a higher seismic rating, saving you from surprises down the road.

To make this crystal clear, the table below breaks down how insurers might look at different properties in these two distinct regions.

Insurance Risk Profile Vancouver vs Fraser Valley

This comparison shows how the exact same type of property can be assessed in completely different ways based on where it’s located and the dominant risks of that area.

Ultimately, your address tells an insurer a story about the potential challenges your property might face. By understanding the specific risks tied to your community—whether it’s in Vancouver or the Fraser Valley—you can better appreciate why your premium is what it is and make smarter decisions about your coverage.

How Climate Events Affect Every BC Homeowner

The increasingly wild weather in British Columbia isn't just small talk anymore; it's a force that's actively reshaping the cost of owning a home. There’s a straight, undeniable line connecting our changing climate, catastrophic events like wildfires and floods, and the bill you get for your home insurance. When a major disaster hits, the financial shockwaves are felt far beyond the fire line or flood zone, creating ripples that raise premiums for everyone.

Think of the entire provincial insurance market as one big shared pool of money. Every homeowner in BC contributes to this pool through their premiums. But when a massive event like an atmospheric river or a devastating wildfire season strikes, it drains billions from that pool to cover claims. To refill it—and brace for the next inevitable event—insurers have to increase contributions from everyone. That means higher premiums, plain and simple.

This isn't a guess; the numbers tell a sobering story. Weather-related disasters have had a massive impact on home insurance costs in BC, driving a big chunk of the premium increases we've seen. In recent years, Canada has seen insured damages from severe weather consistently exceed $2 billion annually, with BC's atmospheric rivers and wildfires being major contributors. You can get more insights on how these events impact home insurance rates on fraserandpartners.ca.

Recalibrating Risk in a New Climate

Insurance has always been a game of prediction. Companies use decades of historical data to figure out future risks and set their prices. The problem is, the scale and frequency of recent disasters in BC have thrown all the old models out the window. The past just isn't a reliable crystal ball for the future anymore.

Insurers are now scrambling to recalibrate their math in real-time, working with a new reality where "once-in-a-century" events seem to be happening every few years. This recalibration means they're:

- Using Updated Climate Models: They're bringing in sophisticated climate science to get a better handle on the likelihood of future floods, fires, and storms in specific places like the Fraser Valley.

- Re-evaluating High-Risk Zones: Areas that were once considered low or moderate risk are being reclassified, leading to some pretty jarring premium hikes for homeowners in those spots.

- Paying More for Their Own Insurance: Insurers buy their own protection, called reinsurance, to shield themselves from massive losses. As disasters increase globally, reinsurers are charging more, and that cost gets passed right down to you.

It’s all about the "ripple effect." A wildfire in the Interior or a flood in the Fraser Valley directly jacks up the premium for a homeowner in Vancouver who never saw a drop of water or a puff of smoke. The whole system has to absorb the financial hit.

This new way of doing things means that the home insurance cost BC residents pay is becoming more unpredictable and directly tied to what the environmental forecasts are saying.

The Provincial Ripple Effect Explained

It’s a question we hear all the time: "My home wasn't touched, so why is my premium going up?" The answer is that the provincial insurance market is all interconnected. One big disaster sets off a chain reaction that every policyholder feels.

Let's say a huge flood in the Fraser Valley causes significant insured damages. The insurance companies on the hook for those losses need to find that money somewhere. They do it by spreading the cost across their entire book of business in British Columbia.

This means a slice of those losses gets baked into the renewal premiums for homeowners in Vancouver, on Vancouver Island, and everywhere else in the province. You aren't just paying for the risk to your own four walls; you're chipping into a provincial fund built to handle catastrophic losses, no matter where they happen. As these events get more frequent and more expensive, everyone's contribution has to go up to keep the whole system afloat.

Practical Strategies to Lower Your Premiums

Knowing what drives up the home insurance cost BC residents pay is one thing, but actually doing something about it is where you can see real savings. While you can't control inflation or change the weather, you have more power than you might think to bring down your annual premiums. It all comes down to showing your insurer that you’re a lower risk.

Many of these strategies are surprisingly simple, involving either a few tweaks to your policy or smart investments in your home's safety. By being proactive, you can often find ways to make your coverage in Vancouver or the Fraser Valley much more affordable without sacrificing the protection you really need.

Adjusting Your Policy for Immediate Savings

One of the fastest ways to cut your premium is to look directly at the structure of your policy. These are straightforward changes you can discuss with your insurance provider right away.

- Increase Your Deductible: This is the amount you pay out-of-pocket on a claim before your insurance coverage starts. If you raise your deductible from, say, $1,000 to $2,500, you’re taking on a bit more of the initial risk. Insurers usually reward this by lowering your premium.

- Bundle Your Policies: Most companies offer a solid discount if you combine your home and auto insurance with them. It simplifies your paperwork and can easily save you 10-15% or more.

- Review Your Coverage Annually: Don't just let your policy auto-renew without a second thought. Your needs can change. Take a few minutes each year to shop around and review your coverage limits to make sure you're not paying for more than you need, especially for your personal belongings.

Proactive Home Upgrades and Maintenance

Insurers love seeing a homeowner who actively works to prevent problems. Investing in key upgrades and keeping up with maintenance can lead to some pretty significant discounts because you're lowering the odds of filing a claim. Real estate experts James and Nicole Isherwood often point out that a well-maintained home isn't just a better investment—it's cheaper to insure, too.

Think about making these high-impact upgrades:

- Install a Monitored Security System: An alarm system that automatically contacts the police or fire department is a big plus for insurers.

- Add Water and Fire Mitigation Devices: Things like smart water leak detectors, a reliable sump pump, and modern smoke detectors can stop a small issue from becoming a catastrophic claim.

- Update Key Systems: A new roof, updated electrical wiring (especially getting rid of old knob-and-tube), or a modern furnace all signal to an insurer that the risk of a major system failure is low.

New technology is also changing the game behind the scenes, helping to streamline the claims process and lower costs for everyone. You can learn more about the role of technology in reducing insurance claims costs to see how innovation is shaping the industry.

When you're buying a new property, a sharp real estate agent can help you spot which features will help or hurt your insurance rates—a cost of ownership that goes way beyond the mortgage. For context in a property sale, typical commissions are 7% on the first $100,000 and 3.5% on the balance. For rental property owners, keeping these systems in top shape is a critical part of our comprehensive residential services.

Common Questions About Home Insurance in BC

When you start digging into the details of home insurance, a few questions always seem to pop up, especially with the unique real estate landscape here in Vancouver and the Fraser Valley. Let's tackle some of the most common ones to help you get a clearer picture of what your policy really covers.

Condo vs. House Insurance Costs

Is there really a big difference in insurance costs between owning a condo and a detached house? Yes, and it’s a significant one. When you own a detached house, your policy has to cover the entire structure, everything inside it, and your personal liability. It’s the whole package.

A condo owner’s policy, on the other hand, is built differently. It mainly covers your unit's contents, your personal liability, and any upgrades you’ve made—think new kitchen cabinets or flooring. The building's exterior, roof, and common areas are already insured by the strata corporation's master policy. This split responsibility usually makes condo insurance quite a bit cheaper, but it’s crucial to know what the strata’s policy covers so you don’t end up with any gaps. For landlords of either property type, knowing where your responsibilities lie is essential; you can find more on this in our guide to landlord resources.

Is Overland Flood Insurance Included?

This is a big one, especially in our part of the world. Is overland flood insurance automatically part of a standard BC policy? Almost never. Overland flood coverage—which protects you from damage caused by overflowing rivers or heavy rainfall—is typically an optional add-on, often called an endorsement.

Given the increasing flood risk in places like the Fraser Valley, this isn't something to gloss over. You should absolutely ask your insurance provider if you're eligible for this coverage and have a serious conversation about whether it's a wise investment for your specific property.

How Can a Real Estate Agent Help?

You might wonder what your real estate agent has to do with insurance. While agents aren't insurance brokers, a knowledgeable one like James or Nicole Isherwood can offer some incredibly valuable insights while you're still house hunting.

They can point out features that insurers love to see, like a new roof, an updated electrical system, or a property that sits safely outside a high-risk floodplain. Their expertise can help steer you toward a home that might qualify for better insurance premiums right from the start, giving you a much clearer picture of your long-term ownership costs before you even make an offer.

Navigating the complexities of real estate and property ownership in the Fraser Valley requires local expertise. At Royal LePage Brookside Realty Property Management, we're here to help you make informed decisions. Contact us today to learn more.