A lot of buyers in Maple Ridge and Pitt Meadows start the same way. They type bc waterfront property for sale into a search bar, scroll through oceanfront estates, remote cabins, and dream-lake photos, then try to answer a harder question. What fits real life if you still want access to work, schools, family, and everyday services in the Lower Mainland?

That’s where waterfront buying gets more complicated than standard home shopping. A waterfront home can offer privacy, recreation, and long-term enjoyment, but it also brings a different set of questions about access, insurance, flood exposure, shoreline rules, property use, and resale. A listing can look perfect online and still be the wrong fit once you examine the land, the setbacks, and the cost of owning it properly.

From a Maple Ridge perspective, that gap matters. Buyers here often aren’t choosing between “waterfront” and “not waterfront” in the abstract. They’re choosing between staying connected to Fraser Valley life or trading convenience for a more distant recreational property. That decision needs local context, not generic province-wide advice.

The Dream and Reality of BC Waterfront Living

Waterfront living in BC sells a powerful idea for good reason. Morning coffee facing the water. A kayak or boat close at hand. Quiet evenings instead of traffic noise. For many buyers in Maple Ridge and Pitt Meadows, that vision isn’t fantasy. It’s a serious goal tied to lifestyle, retirement planning, or a move away from a conventional suburban lot.

The practical side starts fast. Waterfront property is rarely just about the house itself. You’re also buying shoreline conditions, access limitations, municipal rules, insurance realities, and in some cases a maintenance schedule that looks very different from an inland property.

That’s especially true if you’re comparing options across BC while trying to stay rooted in the Lower Mainland. A riverfront property near the Fraser has different trade-offs than a lakefront home in the Interior or an oceanfront home on the Island. Buyers who skip that comparison stage often chase photos instead of fit.

Two habits help early:

- Check your current equity first: If you already own in Maple Ridge or Pitt Meadows, start with a realistic value estimate before touring waterfront listings. A local home evaluation gives you a workable budget range and keeps the search grounded.

- Think beyond the sale price: If the property includes a dock, boathouse, or marine equipment, ongoing care matters. Buyers looking at boat-access lifestyles often review maintenance resources such as Ceramic Coating Marine to understand how exposure to water and weather affects long-term upkeep.

Practical rule: Waterfront works best when the lifestyle matches your weekly routine, not just your weekend imagination.

For Maple Ridge and Pitt Meadows buyers, the smartest move is to treat waterfront as a specialised purchase category. The right property can be exceptional. The wrong one can tie up money in restrictions, repairs, and compromises you didn’t spot at showing time.

Understanding the 2026 BC Waterfront Market

A Maple Ridge buyer can spend Saturday touring a Fraser River property, then lose Sunday night comparing it to a lakefront cabin in the Shuswap or an oceanfront home on the Island. On paper, all three are "waterfront." In practice, they behave like different asset classes, with different carrying costs, risk profiles, and resale pools.

What the current numbers say

A useful snapshot comes from Vancouver Island waterfront listings. Current Vancouver Island waterfront listing data shows 156 waterfront properties for sale, with an average list price of $2.3 million, an average price per square foot of $906, and average time on market of 81 days. That is a premium segment by any standard, and buyers still need to separate true value from expensive frontage with practical limitations.

The wider housing market is moving on a different track. The Vancouver Island Real Estate Board market update reported 636 unit sales across all property types in March 2026 and 3,360 active listings. That matters because many buyers still apply ordinary detached-home assumptions to waterfront homes. Inventory depth, pricing pressure, and buyer urgency are often very different once shoreline enters the equation.

For Lower Mainland buyers, the lesson is simple. Do not treat a waterfront home like a standard house with a better view.

Three very different waterfront categories

A buyer starting from Maple Ridge or Pitt Meadows usually ends up weighing three broad choices, and the trade-offs are not subtle.

Oceanfront

Oceanfront usually carries the strongest emotional pull. It also tends to bring the highest entry price, greater weather exposure, and more scrutiny around foreshore use, private docks, bank stability, and access. For a buyer who still needs regular trips back to the Fraser Valley, the romance can fade once ferry schedules, storm exposure, and maintenance logistics become part of the weekly routine.

Lakefront

Lakefront often fits buyers who want active use. Swimming, paddling, fishing, and multigenerational weekends are usually the point. The challenge is distance. If the property is close enough for frequent use, it is often scarce and priced accordingly. If it is farther into the Interior, ownership becomes more hands-on from a distance.

That split is why many local buyers spend time searching connected communities first through a Pitt Meadows home search with local map-based filters, then expand outward only after they define what "usable waterfront" really means for their schedule.

Riverfront

Riverfront deserves more attention than it gets. For Maple Ridge and Pitt Meadows buyers, it can be the most practical version of waterfront ownership because it keeps you closer to work, schools, and family support. It also demands sharper review. Along the Fraser River and near creek systems such as Kanaka Creek, the questions change quickly. Floodplain rules, setback limits, erosion history, and insurance availability can matter more than the view from the deck.

I often find buyers underestimate that difference. A beautiful riverfront lot can still be the wrong purchase if a large portion of the site is constrained or if future improvements are difficult to approve.

The best waterfront purchase is usually the one you can use often, maintain properly, and resell without explaining away major limitations.

Why Lower Mainland buyers need a narrower market lens

Province-wide search results can give a false sense of abundance. Many listings are seasonal, remote, boat-access, heavily constrained, or priced far beyond what a Maple Ridge or Pitt Meadows move-up buyer intends to carry.

That is why broad BC market data has limits. It helps frame pricing and supply, but it does not answer the practical questions that matter most to a Fraser Valley buyer. Can you reach the property after work. Will the site support the use you want. Is the shoreline stable. Are there flood or servicing issues that make ownership more expensive than the list price suggests.

This is where local context matters. A buyer comparing Alouette Lake aspirations, Fraser River frontage, and Vancouver Island inventory is not just comparing scenery. They are comparing access, regulation, maintenance, and resale depth across very different markets. Buyers who understand that early tend to make better decisions and fewer expensive compromises.

Where to Search From Maple Ridge and Pitt Meadows

Most local buyers don’t need more listings. They need a better search map. If you’re based in Maple Ridge or Pitt Meadows, the best waterfront search usually starts by deciding how much distance you’re willing to tolerate for the sake of shoreline.

Start with your real commute and routine

A buyer who wants a weekend retreat can search differently from a buyer who still needs a weekday school run, regular office access, or quick trips to Maple Ridge amenities. That’s why I usually divide the search into two buckets. One is destination waterfront. The other is connected waterfront.

Destination waterfront includes the Gulf Islands, Shuswap, Okanagan, and more remote lake areas. These can be beautiful and rewarding, but they ask more from the owner. Travel time is longer. Maintenance logistics are harder. A small issue with the property may require a full day to handle.

Connected waterfront is the category that usually matters more to Lower Mainland buyers. That includes river-oriented opportunities, water-adjacent pockets, and properties that keep you within reach of Maple Ridge, Pitt Meadows, schools, shopping, and family support.

The gap in the market close to home

There’s a real shortage of accessible local options. In 2025, Maple Ridge saw only 3 waterfront sales averaging C$1.2M, which highlights how limited the local supply is for buyers who want a practical lifestyle property near areas like Kanaka Creek and Cottonwood, according to Lower Mainland waterfront market commentary.

That shortage explains why local buyers often feel stuck between extremes. On one side, there are remote parcels. On the other, there are high-end listings that don’t fit the budget or the day-to-day plan.

If you want to monitor homes that keep you tied to the local market while you refine your search, a live Pitt Meadows home search is a practical place to track nearby inventory patterns.

Areas local buyers usually compare

Fraser River edge

The Fraser is the obvious local reference point. Some buyers are drawn to the scale of the water and the sense of openness. Others underestimate the due diligence that riverfront requires. Along the Fraser, the view may be excellent while the building envelope, shoreline use, or insurance profile is less flexible than expected.

This is often where buyers need to separate “waterfront feeling” from “waterfront function.”

Pitt River side

For buyers in Pitt Meadows, Pitt River proximity can offer a balance of scenery and access. The appeal is straightforward. You stay close to established community services while still pursuing a waterfront-oriented lifestyle. The trade-off is scarcity. When practical properties come up, they attract serious attention.

Alouette Lake and recreation-oriented searches

Alouette Lake is usually part of the conversation because buyers love the recreation and the local familiarity. The caution is simple. Recreation value doesn’t always line up with easy ownership. Some buyers are better served by a home with strong access to parks and water activities rather than pursuing a direct waterfront property with more restrictions.

A good search area isn’t just where the water is. It’s where ownership still works after the excitement wears off.

How neighbourhood character changes the search

Neighbourhood matters because waterfront value isn’t only about the shoreline. It’s also about how the property fits into daily living.

- Albion: Buyers often like Albion for family orientation, school access, and established neighbourhood feel. For waterfront-adjacent searches, the key issue is usually whether the lot gives you the lifestyle you want without overcomplicating improvements.

- Kanaka Creek: This area attracts buyers who want more greenery and a different pace. It can be appealing for a creekside or river-influenced search, but buyers need to ask harder questions about land use and setbacks.

- Silver Valley: Silver Valley often attracts buyers seeking nature and privacy. That can pair well with a waterfront mindset, but rural-feeling settings usually demand stronger due diligence on services and build constraints.

- Cottonwood: Cottonwood is worth watching for buyers who want a practical home base and quick access to local amenities while staying open to nearby lifestyle-oriented properties.

This video gives a useful visual sense of waterfront search considerations in BC:

The buyers who do well in this market aren’t always the ones chasing the most dramatic listing. They’re the ones who define their radius, identify what “usable waterfront” means to them, and stay realistic about how often they’ll live the lifestyle they’re paying for.

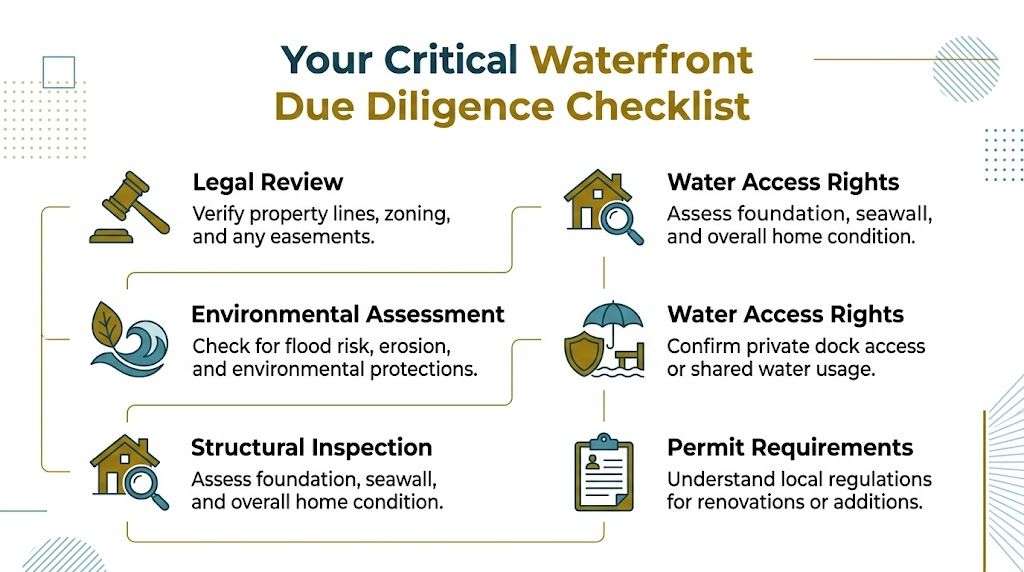

Your Critical Due Diligence Checklist

A waterfront purchase needs a different standard of investigation. On a typical suburban home, the big questions are often condition, price, and location. On waterfront, you also need to know what you can build, what you can insure, what part of the shoreline you control, and what environmental limits come with the land.

Flood and setback issues are not side notes

For Maple Ridge area buyers, flood exposure belongs near the top of the checklist. Record Fraser River levels in 2025 brought that issue into sharp focus, and the Riparian Areas Protection Regulation requires 30m setbacks, affecting development in places such as Albion and Silver Valley. The same source notes that insurance premiums for high-risk zones have surged by 40%, which is why geotechnical review has become much more than a box to tick, according to this BC waterfront risk overview.

That matters for two reasons. First, your future renovation options may be narrower than the listing suggests. Second, a lender and insurer may view the same property more cautiously than a buyer does on first impression.

The six checks that matter most

Legal boundaries and rights

Waterfront buyers often assume the lot line works the way it does on a standard residential parcel. It may not. You need a lawyer and survey review that confirms property lines, easements, access rights, and any restrictions tied to shoreline use.

A dock, retaining wall, path, or cleared area near the water can exist physically and still raise legal questions. Don’t treat visible use as proof of permitted use.

Environmental constraints

Environmental regulation is where many waterfront buyers lose flexibility. Creeks, rivers, and shorelines can trigger setback rules, habitat protections, and permit requirements that shape what you can add, remove, or rebuild.

Imagine it as buying a home with invisible lot lines inside the parcel. The title may say one thing, but the usable area for future changes can be smaller.

Structure and site stability

A home inspection matters, but it isn’t enough by itself on waterfront. The shoreline, grade, bank condition, drainage behaviour, retaining structures, and any signs of long-term movement deserve close attention. If the lot shows warning signs, a specialist opinion is money well spent.

This is especially important near riverbanks and creek-influenced sites, where a nice rear yard can mask ongoing ground movement.

Local caution: If the value of the property depends on the shoreline, inspect the shoreline as seriously as you inspect the house.

Services and systems can change the deal

The farther a property gets from standard municipal servicing, the more careful a buyer should become. Some waterfront homes rely on private systems or older infrastructure that can be manageable when maintained and expensive when ignored.

Key checks usually include:

- Water source: Confirm whether the property uses municipal water, a private well, or another system, and test quality where appropriate.

- Septic arrangements: Verify age, condition, location, and compliance, especially if future additions are part of your plan.

- Drainage behaviour: Ask how the property handles heavy rain, runoff, and seasonal water movement.

- Access: Confirm road condition, shared access terms, and year-round usability.

Financing and insurance should be reviewed early

Many buyers leave lender and insurer questions too late. That’s a mistake on waterfront property because a standard approval on paper doesn’t guarantee a smooth file once the property details are reviewed.

I strongly recommend this sequence:

- Speak to your mortgage professional before touring seriously.

- Flag any riverfront, creekside, or unusual access property immediately.

- Request insurance input before removing subjects.

- Budget for specialist reports where the land conditions call for them.

A lender may be comfortable with one waterfront property and hesitant on another that looks similar to you. The difference is often in access, setback constraints, erosion exposure, or rebuild complexity.

What buyers in Maple Ridge often underestimate

The biggest misconception is that due diligence only protects against disaster. In practice, it also protects your plans. A buyer may be perfectly happy with some flood exposure or a more limited building envelope if they know that upfront and buy accordingly.

The problem starts when someone pays for a dream version of the property and receives a restricted version of it after closing.

A good waterfront purchase isn’t the one with zero complications. It’s the one where the buyer understands the complications, prices them correctly, and still likes the property enough to proceed with confidence.

Financing and Insuring a Waterfront Home

Many buyers are surprised when financing a waterfront home feels slower than financing a conventional house. The reason is simple. Lenders and insurers don’t underwrite waterfront the same way they underwrite a standard lot in a typical subdivision.

They look more closely at the asset itself. Not just your income, down payment, and credit, but the land, risk profile, and ease of resale if something goes wrong.

Why the approval process feels different

With waterfront property, lenders often ask more detailed questions about access, improvements near the shoreline, servicing, and insurability. If the home is on a riverbank, near protected areas, or tied to non-standard systems, the file can require more review.

That doesn’t mean financing is out of reach. It means you should prepare for a narrower lending conversation and build more time into the process.

A few practical steps help:

- Get fully reviewed, not loosely pre-approved: A surface-level pre-approval may not account for the property type you eventually choose.

- Use payment planning early: A tool like this mortgage payment calculator helps buyers test realistic monthly scenarios before they commit to a waterfront price point.

- Keep reserve funds available: Waterfront buyers often need room for reports, repairs, insurance adjustments, or post-closing maintenance.

Insurance can reshape the whole deal

Insurance is where many waterfront purchases either stabilise or become far less attractive. A buyer may be comfortable with a home’s location, but if coverage is limited, expensive, or layered with exclusions, ownership cost changes quickly.

This is why I tell buyers to treat insurance as an active approval item, not an afterthought. Ask early whether the insurer is comfortable with the exact property. “Waterfront” is too broad a category to be useful on its own.

Questions worth asking include:

- Does the policy address flood-related exposure clearly?

- Are docks, shoreline structures, or detached waterfront improvements included?

- Are there conditions tied to inspections or specialist reports?

- Will the insurer require upgrades or mitigation work?

The wrong time to discover an insurance problem is after you’ve emotionally committed to the property.

Build your team before you write

This part of the transaction works better when the property side, mortgage side, and insurance side are aligned before subjects come off. Depending on the property, buyers may also involve lawyers, inspectors, and, where relevant, local service providers such as Royal LePage Brookside Realty Property Management for practical information about property operations and oversight in the Maple Ridge and Pitt Meadows market.

The strongest waterfront buyers don’t just prove they can purchase the property. They prove they can carry it comfortably once the true cost of ownership is on the table.

Navigating the Buying Process Step by Step

A waterfront search needs more discipline than a standard home search. Buyers who treat it like a normal residential purchase often move too quickly on the wrong property or write offers without the right protections. Local expertise matters because the issues aren’t abstract. They affect what you can do with the land, what it costs to own, and how easy it will be to sell later.

If you’re preparing to buy, start with a grounded overview of the home buying process in Maple Ridge and Pitt Meadows, then adapt that process to the extra layers waterfront adds.

A simple process that protects buyers

Stage one: define the use

Decide whether this will be a primary residence, a part-time retreat, or a long-term lifestyle purchase you grow into later. That answer shapes location, commute tolerance, servicing expectations, and offer strategy.

A buyer who needs weekday practicality should eliminate unsuitable areas early. A buyer who wants a recreation property can widen the map, but should expect more ownership complexity.

Stage two: search with filters that matter

Don’t search by “waterfront” alone. Add filters based on access, neighbourhood fit, likely servicing, and how much improvement flexibility you need. A pretty shoreline with no realistic path to your intended use can waste weeks.

Stage three: view the property like land first

At showings, spend as much attention outside as inside. Look at slope, drainage paths, retaining structures, shoreline condition, and where nearby homes sit relative to the water. The kitchen renovation isn’t the first priority on waterfront. The site is.

Waterfront Property Buying Checklist

| Stage | Key Action | Local Tip for Maple Ridge Buyers |

|---|---|---|

| Search setup | Narrow the search by use, distance, and property type | Focus first on whether you need everyday access to Maple Ridge or Pitt Meadows |

| Property review | Assess the lot, shoreline, and surrounding context | Pay close attention to riverfront and creekside conditions before getting attached |

| Offer preparation | Build in strong subjects tailored to the property | Include conditions that address water, land, and insurance issues where relevant |

| Subject period | Bring in the right specialists | Use professionals familiar with Fraser Valley land and waterfront concerns |

| Final decision | Re-price the deal after reports and insurance feedback | A good purchase still has to make sense after the hidden costs become visible |

What strong waterfront subjects often address

The offer is where local representation becomes essential. Subject clauses on waterfront property shouldn’t be recycled from a standard detached purchase without thought. They need to reflect the actual risks attached to the home and site.

Common areas for conditions may include:

- Financing review: Especially where the property type raises lender questions.

- Insurance review: Critical on riverfront or higher-risk sites.

- Inspection and specialist review: Sometimes including shoreline, drainage, septic, or engineering input.

- Water and servicing review: Important where municipal assumptions don’t apply.

- Title and legal review: To confirm use rights, easements, and restrictions.

A clean offer isn’t always a smart offer. On waterfront, the best-written offer is the one that protects the buyer from the right risks.

The local advantage matters most at the decision point

Hyper-local expertise pays off when a listing looks attractive but the property tells a more mixed story in person. An agent who knows Maple Ridge and Pitt Meadows can often spot the difference between a property with manageable issues and one with constraints that will keep resurfacing.

That’s the part many out-of-area buyers miss. On paper, several waterfront homes can look interchangeable. In real life, one sits in a more workable setting, has a clearer path for insurance, and fits local ownership expectations far better. That difference is what keeps buyers from making a costly emotional decision.

Why a Local Waterfront Specialist is Essential

Waterfront buyers usually don’t need more enthusiasm. They need sharper judgement. The right specialist helps by filtering emotion through practical local knowledge, especially when a property is tied to river conditions, neighbourhood nuances, and municipal limits that don’t appear clearly on the listing sheet.

In Maple Ridge and Pitt Meadows, that local layer matters because waterfront and water-adjacent purchases don’t exist in isolation. They sit inside real neighbourhood patterns. School access, commuting routes, future resale, flood-area awareness, and lot usability all affect whether the purchase will feel smart two years from now, not just on possession day.

Questions buyers still ask late in the process

Do I need a waterfront specialist if I already know the area

Yes, if the property is meaningfully different from a conventional residential purchase. Knowing Albion, Silver Valley, or Pitt Meadows as neighbourhoods isn’t the same as understanding the implications of setback rules, bank conditions, or insurability on a shoreline property.

Can a good general inspection cover most of it

Sometimes, but not always. A capable home inspector is valuable, but waterfront often requires a wider circle of professionals. The issue isn’t whether the inspector is good. It’s whether the property raises questions outside the scope of a standard inspection.

Is the value mainly in the view

No. The value is in the combination of view, usable site, legal clarity, ownership cost, and future marketability. A strong view with weak practicals can still be an overpayment.

What local representation changes

A local specialist helps buyers:

- Screen opportunities faster: Some listings look better online than they do once you assess the site and surroundings.

- Ask better questions earlier: That reduces wasted showings and weaker offers.

- Coordinate the right professionals: Lawyers, inspectors, insurance contacts, and site-specific specialists matter more on waterfront.

- Negotiate from facts instead of emotion: The advantage usually comes from what the land and improvements can or can’t support.

Buyers also want proof that the person advising them understands this market in real transactions, not just in theory. Reviewing local client experiences and testimonials can help you gauge whether the guidance has been useful to other buyers and sellers in Maple Ridge and Pitt Meadows.

The best waterfront purchases usually come from a calm process. Good local advice keeps the dream intact while removing the avoidable mistakes.

Frequently Asked Questions

Is waterfront property in BC always a luxury purchase

Not always, but it often trades in a premium category. The bigger point is that “waterfront” includes very different property types. A local riverfront opportunity, a remote parcel, and a high-end oceanfront home may all appear under the same search term while offering very different ownership realities.

What should Maple Ridge buyers focus on first

Start with practicality. Decide whether you want daily livability near the Lower Mainland or a destination property farther away. That choice will narrow the field faster than scrolling through hundreds of province-wide listings.

Are Fraser River properties automatically a bad idea because of flood concerns

No. They just require stronger due diligence. Flood exposure, setbacks, and insurance should be reviewed carefully so you understand the property you’re buying, not the one you assumed you were buying.

Is a dock the main thing I should look for

A dock can add appeal, but it shouldn’t lead the analysis. Usable land, shoreline condition, insurance, legal rights, and property constraints matter more than one visible feature.

Can I rely on the listing description for waterfront details

Use the listing as a starting point, not a final authority. Waterfront homes need verification on title, land use, insurability, and any improvements near the shoreline.

Should I sell my current home before searching seriously

That depends on your equity position, risk tolerance, and the type of purchase you’re pursuing. Many buyers make better decisions when they understand their current home value and financing range before they start writing offers on specialised properties.

If you’re weighing a waterfront move, a sale, or a broader real estate decision in Maple Ridge or Pitt Meadows, Royal LePage Brookside Realty Property Management can help you sort through the local details with a clear, practical approach.