For most Canadians, the biggest sigh of relief when selling a home comes from a single, powerful tax rule: the Principal Residence Exemption (PRE). In short, this means you likely won't pay a dime in capital gains tax on the profit from selling your main family home. As long as the property you’re selling has been your primary address, you can often shelter the entire gain from the taxman.

Your Guide to Capital Gains on Your Home Sale

If you're a homeowner in the fast-paced Vancouver or Fraser Valley real estate markets, the question of taxes probably looms large. After years of watching property values climb, the potential profit from a sale can be massive—and with that comes the worry of a hefty bill from the Canada Revenue Agency (CRA).

But here’s the good news: our tax system is designed to protect the gains on your family home. The Principal Residence Exemption is one of the most generous breaks in Canadian tax law, and this guide will walk you through exactly how it works. We'll break down the essential concepts in simple, straightforward terms.

Navigating the Financial Side of Your Sale

Think of this as your roadmap to understanding the financial side of selling your home with confidence. We’ll cover what qualifies as a principal residence, how you report the sale, and the specific situations that might actually trigger a tax bill. A little planning goes a long way.

A crucial piece of the puzzle is making sure you designate the property correctly. In any given year, a family unit—that’s you, your spouse or common-law partner, and any kids under 18—can only designate one property as their principal residence.

This is where having an experienced real estate team in your corner is so important. While they aren't tax advisors, experts like James and Nicole Isherwood live and breathe the local market. They understand the importance of having a solid financial plan and will ensure you’re connected with a qualified accountant for advice tailored to your situation.

Their job isn't just about marketing your home and negotiating the best price—which includes factoring in typical commissions of 7% on the first $100,000.00 and 3.5% on the balance. It's about guiding you through the whole journey, so you can focus on your next chapter knowing the tax side of things is being handled correctly.

What Exactly Is a Capital Gain on Real Estate?

Before we jump into tax exemptions, we need to get clear on what a capital gain actually is. In simple terms, a capital gain is the profit you pocket when you sell an asset—what the government calls capital property—for more than you paid for it. This rule applies to stocks, rare art, and, of course, real estate.

Think of it this way: you buy an asset for $20,000 and, a few years later, sell it for $30,000. That $10,000 difference is your capital gain. The same idea applies to selling a home, but the math has a few more important moving parts. The real key is understanding the difference between your sale price and what the Canada Revenue Agency (CRA) calls the Adjusted Cost Base (ACB).

Understanding Your Adjusted Cost Base

Your property's ACB isn't just the price you paid for it. It’s a running total of your initial investment plus any eligible costs you've incurred that genuinely add to the property's value. Getting this number right is one of the single most effective ways to lower your potential tax bill.

So, what can you include in your ACB?

- Original Purchase Price: This is the straightforward starting point—the amount you first paid for the home.

- Acquisition Costs: These are the necessary expenses from when you bought the property, like legal fees, land transfer taxes, and home inspection fees.

- Capital Improvements: This one is a big deal. It covers major renovations that improve the property, not just maintain it. We're talking about a brand-new kitchen, a finished basement, or a significant landscaping overhaul. Regular repairs, like repainting a room, don't make the cut.

By keeping meticulous records of these expenses, you increase your ACB. A higher ACB means a lower calculated profit when you sell, which directly shrinks any potential capital gains tax.

How Capital Gains Are Taxed in Canada

Another critical piece of the puzzle is Canada's inclusion rate. You aren't taxed on the entire profit from your sale. Instead, only 50% of the capital gain is actually considered taxable income.

For example, if you sell an investment property and make a capital gain of $100,000, only $50,000 of that profit gets added to your income for the year. This taxable amount is then taxed at your personal marginal tax rate, just like the income from your job.

This 50% inclusion rate is a fundamental concept for anyone selling a property that doesn't fully qualify for the Principal Residence Exemption. It makes figuring out your potential tax obligations much more manageable. With a solid grasp of both your ACB and the inclusion rate, you're in a much better position to navigate the financial side of selling a home and capital gains.

How the Principal Residence Exemption Works

The Principal Residence Exemption (PRE) is hands-down the most powerful tax benefit for Canadian homeowners. When you start digging into the rules around selling a home and capital gains, you’ll quickly find that this exemption is the key that lets most people in Vancouver and the Fraser Valley walk away with their profits completely tax-free.

But it’s not an automatic pass. You have to meet specific criteria laid out by the Canada Revenue Agency (CRA) to qualify.

At its core, the PRE hinges on a single, simple-sounding rule: you must have "ordinarily inhabited" the home during the years you claim the exemption. The CRA uses this intentionally flexible phrase because "living" in a home looks different for everyone. It doesn't mean you had to be there 365 days a year, but it has to be clear that this was your main hub—the place you came home to, got your mail, and lived your day-to-day life.

This flexibility is helpful in a lot of real-world situations. Even if you only owned the home for a short time, you could still qualify, as long as your primary reason for buying it was to live in it, not to flip it for a quick profit. The CRA will look at the facts of your case, like the address on your driver’s licence and where you were registered to vote, to confirm it was your home base.

Designating Your Principal Residence

Here’s a critical detail: a family unit can only designate one property as its principal residence for any given year. This rule becomes incredibly important for families in BC who might own a primary home in Surrey and a weekend cabin up in the Fraser Valley. You can't shield the gains on both properties for the same tax years.

When you eventually sell one of those properties, you’ll have to make a strategic decision about which years you assign the exemption to. This choice directly affects how much of the PRE you’ll have left to use on your other property down the road.

The "family unit" for this rule includes you, your spouse or common-law partner, and any unmarried children under 18. This collective rule stops couples from trying to each claim a different home for the same year.

This is a perfect example of why getting professional advice is so crucial. Navigating the transaction with real estate experts like James and Nicole Isherwood ensures you're prompted to connect with a tax professional who can help you make the smartest designation for your long-term financial health. For those who own multiple properties, especially rentals, understanding your obligations is vital. You can find more valuable information in our guide to landlord resources.

The "Plus One" Rule Explained

The tax formula for the PRE includes a handy little provision known as the "plus one" rule. In simple terms, this rule lets you add one extra year to the number of years you designate a home as your principal residence.

Why does this matter? It’s designed to help homeowners who sell their old home and buy a new one in the same calendar year. Without it, you’d technically own two principal residences at the same time, which could create a tax mess. The "plus one" rule ensures the gains on both homes can be fully sheltered for the year you move, preventing any overlap issues. It's a common and welcome scenario for active buyers and sellers in the Vancouver market.

Finally, and this is non-negotiable, you must report the sale of your principal residence on your income tax return for the year it was sold. Even if you owe $0 in tax because the PRE covers the entire gain, you are still required to file Form T2091, Designation of a Property as a Principal Residence by an Individual. Forgetting this step can lead to hefty penalties and could even put your entire exemption at risk.

When You Might Owe Capital Gains Tax

The Principal Residence Exemption (PRE) is one of the most valuable tax breaks for Canadian homeowners, but it's not a free pass in every scenario. While most people in Vancouver and the Fraser Valley will sell their main home without paying a dime in tax, a few common situations can land you with an unexpected capital gains tax bill.

Knowing these exceptions is key to smart financial planning, especially when you decide to sell.

The most common trigger is what the Canada Revenue Agency (CRA) calls a "change in use." This happens when you switch all or part of your property from your personal home into something that generates income. The CRA treats this change as if you sold that portion of your property at its fair market value on the very day its purpose changed. This is known as a "deemed disposition."

When Your Home Becomes a Business

In bustling areas like the Fraser Valley, it's not uncommon for homeowners to use part of their property to earn some extra money. It's a savvy move, but it has major tax implications down the road.

Two main scenarios cause a "change in use":

- Putting in a Rental Suite: Turning your basement into a separate apartment for a long-term tenant is the classic example. That part of your home is no longer your principal residence—it's now a rental property in the eyes of the CRA.

- Running a Business From Home: If you use a room exclusively for a business office, workshop, or studio, it can also qualify. The real kicker is if you claim Capital Cost Allowance (depreciation) on that part of your home for your business taxes. Once you do that, the CRA officially considers it income-producing property.

When you eventually sell your home, you'll likely owe capital gains tax on the growth in value of that income-producing portion, calculated from the day you made the change.

It's a common myth that any rental income automatically kills your PRE. If the rental is a small part of your home's overall use, you don't make structural changes, and you don't claim depreciation, you might be in the clear. Still, this is tricky territory, and you absolutely should talk to a tax professional to be sure.

For example, you'll almost certainly owe capital gains tax if the property isn't your main home at all, which is a key consideration for anyone figuring out how to sell rental property with tenants.

The Half-Hectare Rule

Another important limit to the PRE involves the size of your land. The exemption automatically covers your house and the land it sits on, but only up to one-half hectare (which is about 1.24 acres).

Plenty of properties in Langley, Maple Ridge, and other parts of the Fraser Valley are bigger than that. If your lot is larger than the half-hectare limit, the CRA won't automatically exempt the whole thing. You can still claim the PRE on the extra land, but the burden is on you to prove why you should.

To get the exemption for a property larger than half a hectare, you have to demonstrate to the CRA that the extra land was "necessary for the use and enjoyment" of your home. That can be a tough standard to meet. Things like local zoning laws that dictate a minimum lot size or the physical nature of the land (like a ravine that makes part of it unusable for anything else) could help your case.

Without solid proof, the capital gain on the excess land will be taxable. This is a critical detail for homeowners with larger lots and a point where experienced real estate advisors like James and Nicole Isherwood would strongly recommend getting an accountant involved early.

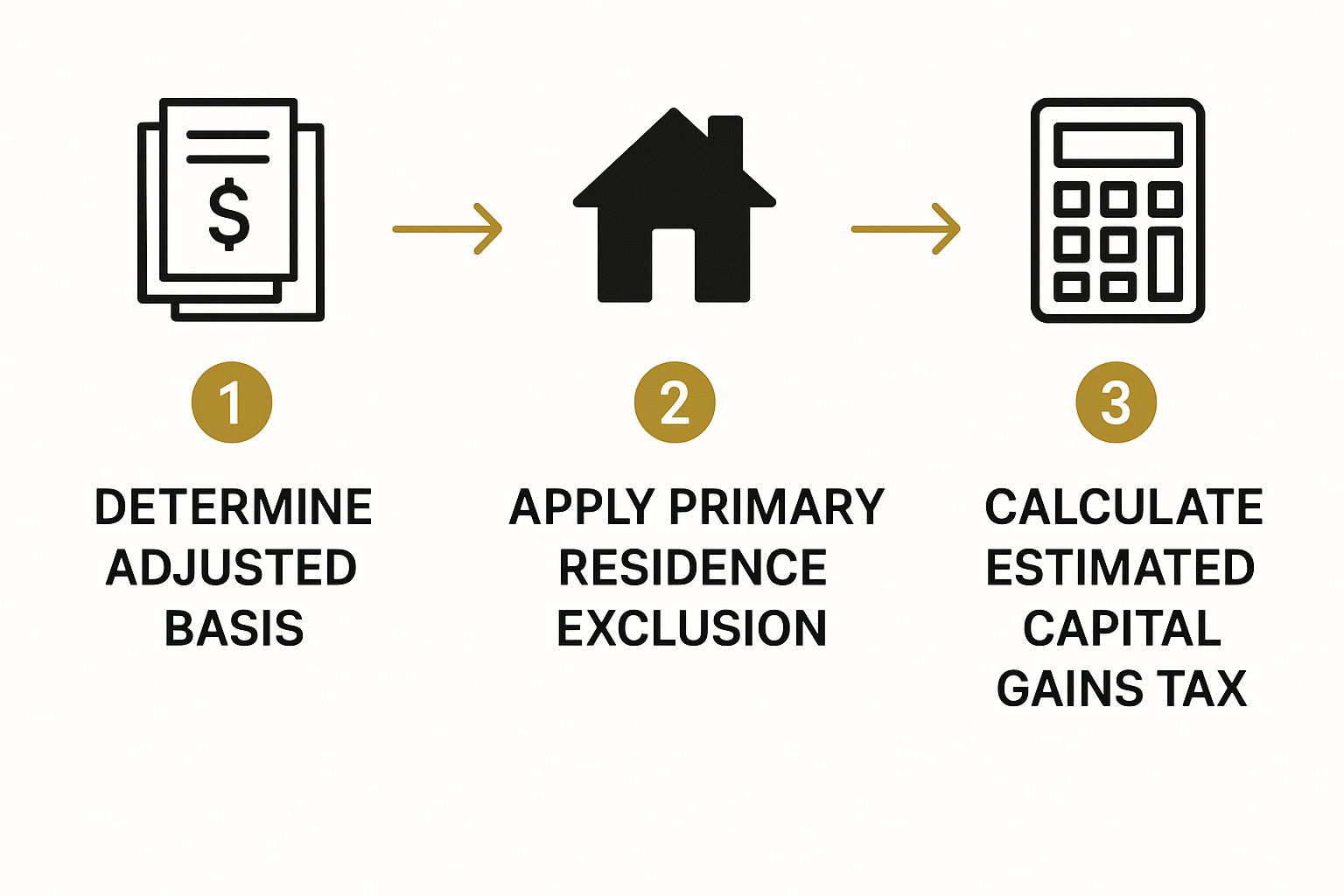

Putting Pen to Paper: How to Calculate Capital Gains Tax in BC

Understanding the theory behind capital gains is one thing, but actually crunching the numbers makes it all click. Let’s walk through a realistic scenario for a property sale in the Vancouver area to break down exactly how this works. The whole process really comes down to a few key steps: figuring out what you truly spent, calculating your real profit, and then determining the taxable slice of that profit.

This flowchart gives you a simple, three-step look at the calculation.

As you can see, the main idea is to find your true profit by subtracting all the eligible costs from your final sale price before the tax rules come into play.

A Real-World Vancouver Example

Let's imagine you're selling a home that was never your principal residence—maybe it was a rental property. This means the entire gain is on the table for tax purposes.

Here's the situation:

- Original Purchase Price: You bought the property for $800,000.

- Capital Improvements: Over the years, you put $75,000 into qualifying renovations, like a brand-new kitchen and updated bathrooms.

- Sale Price: You sell the home for $1,500,000.

First, we need to pin down two crucial figures: the Adjusted Cost Base (ACB) and the Proceeds of Disposition.

Step 1: Calculate Your Adjusted Cost Base (ACB)

Think of the ACB as your total investment in the property. It’s not just what you paid for it; it also includes those big-ticket capital improvements and any costs you paid when you first bought the place.

- Purchase Price: $800,000

- Capital Improvements: $75,000

- Total Adjusted Cost Base (ACB): $875,000

Getting this number right is critical because a higher ACB directly shrinks your capital gain.

Step 2: Determine Your Proceeds of Disposition

Next up, let's figure out what you actually pocketed from the sale. This is your sale price minus all the costs that came with selling the property. These expenses, like legal fees and real estate commissions, get deducted right off the top.

Let's calculate the real estate commission first. A typical structure in BC is 7% on the first $100,000.00 and 3.5% on the remaining balance.

- Commission on first $100,000.00: $100,000.00 x 7% = $7,000

- Commission on the balance: ($1,500,000 - $100,000.00) x 3.5% = $1,400,000 x 3.5% = $49,000

- Total Commission: $7,000 + $49,000 = $56,000

Now, let's factor in other typical selling costs, like legal fees (we'll estimate $1,500).

- Gross Sale Price: $1,500,000

- Less Total Commission: -$56,000

- Less Legal Fees: -$1,500

- Proceeds of Disposition: $1,442,500

Step 3: Calculate the Capital Gain and Taxable Amount

With our two main figures locked in, the rest is pretty straightforward.

Capital Gain = Proceeds of Disposition - Adjusted Cost Base (ACB)

- $1,442,500 - $875,000 = $567,500 (Total Capital Gain)

Now for the key part: in Canada, you’re only taxed on 50% of your capital gains.

- Taxable Capital Gain: $567,500 x 50% = $283,750

This $283,750 is the amount you have to add to your total income for the year. It gets taxed at your personal marginal tax rate, which all depends on your total income bracket. Seeing these numbers can also be a huge help when planning for your next purchase; you can play around with potential monthly costs with a handy mortgage payment calculator to get a clearer picture of your budget.

When you file your taxes, you'll report the sale on Schedule 3 (Capital Gains or Losses). If you were claiming the PRE for some or all of the years, you'd also need to complete Form T2091 to designate the property as your principal residence. Experienced real estate professionals always advise clients to work with an accountant to make sure these calculations and forms are handled perfectly.

Navigating Your Sale with Expert Guidance

Selling your home isn't just another transaction; for most people, it's one of the biggest financial events of their lives. Getting a handle on the details of selling a home and capital gains means you need more than a quick Google search—you need a coordinated team of pros on your side. This is where an experienced real estate salesperson provides value that goes far beyond just putting a sign on your lawn.

For anyone selling in the fast-paced Vancouver and Fraser Valley markets, real estate salespeople like James and Nicole Isherwood become the central hub for the entire sale. Their deep local knowledge ensures your property is priced right and marketed effectively to pull in the best buyers. But that's just the beginning.

Your Professional Team Quarterback

Think of James and Nicole as the quarterback for your professional team. While real estate salespeople don't give tax advice, their most critical role is connecting you with their network of trusted experts, including accountants and lawyers who live and breathe BC real estate tax law.

This guidance is everything. They make sure you're asking the right questions from day one, helping you sidestep common mistakes and get ready for tax season long before it arrives. From accurately calculating what you'll walk away with after commissions—typically 7% on the first $100,000.00 and 3.5% on the balance—to making sure your paperwork is flawless, their support is invaluable.

If you're curious about what your home could be worth in the current market, a good first step is getting a free home evaluation.

An experienced salesperson makes sure every piece of the puzzle fits together perfectly. They'll coordinate with your lawyer for the closing and give you a nudge to chat with your accountant about capital gains, ensuring the whole process is smooth and financially sound.

Beyond the numbers, getting your home market-ready is a huge piece of the puzzle. You can boost your home's appeal and potentially its final sale price by following expert home staging advice. This kind of proactive approach, led by seasoned professionals, can turn a stressful process into a well-managed and successful financial outcome.

Common Questions About Home Sales and Capital Gains

Working through the rules around capital gains on a home sale can feel a bit like untangling a knot. Lots of specific questions pop up. Here, we'll tackle some of the most common ones we hear from homeowners in Vancouver and the Fraser Valley, giving you clear, straightforward answers.

What Happens If I Forget to Report the Sale of My Home?

This is a big one. Since 2016, the Canada Revenue Agency (CRA) has required you to report the sale of your principal residence on your tax return, even if you owe zero tax because of the exemption.

If you simply forgot, the best thing to do is file an amendment to that year’s tax return as soon as you realize the mistake. Don’t wait. The CRA can hit you with a late-filing penalty, which is the lesser of $8,000 or $100 for each full month your report is overdue.

Can I Claim the Exemption on a Vacation Property?

Yes, you can designate a vacation property or a cottage as your principal residence, but you have to play by the rules. The key phrase from the CRA is that you must have "ordinarily inhabited" it at some point during the years you’re claiming the exemption. You don't have to live there full-time, but you must have used it.

Here’s the catch: a family unit (you, your spouse, and your children under 18) can only designate one property per year. This makes strategic planning essential, especially if you sell your city home and the cottage in different years. It's always a good idea to chat with a tax professional to figure out the most tax-efficient way to use the exemption. For those thinking about what comes next, our guide on buying a home can help you navigate the next chapter.

A classic B.C. scenario is owning a family home in the city and a cabin up north. When you decide to sell, you can't shield the gains on both properties for the same years. Deciding which property to designate for which year is the key to minimizing your overall tax bill.

How Does Divorce Affect the Principal Residence Exemption?

When a marriage or common-law partnership ends, the rules around the principal residence exemption get tricky. A home can typically be transferred between spouses on a tax-deferred basis, but the decisions you make during the separation agreement can have major capital gains consequences for both of you down the road.

This is not something to navigate on your own. It's absolutely critical to get advice from both your family lawyer and a tax accountant to ensure everything is handled correctly and fairly for the future.

At Royal LePage Brookside Realty Property Management, we believe that giving our clients the right knowledge and connecting them with trusted professionals is the foundation of a successful sale. When you're ready to plan your next move, you can count on our team to guide you.