When it comes to figuring out your tax obligations as a landlord, a rental income tax calculator is your best friend. It’s designed to cut through the noise, systematically adding up your rental income, subtracting all those eligible expenses—like mortgage interest and property taxes—and giving you the net rental income. That’s the magic number you'll be taxed on at your personal marginal rate.

Your Guide to Maple Ridge Rental Tax

Sorting out rental taxes in Maple Ridge can feel like a maze, but what the Canada Revenue Agency (CRA) asks for is actually quite straightforward: report all the income your property earns, and then deduct every reasonable expense you paid to earn it. This is exactly why a good calculator is so crucial—it helps you stay accurate and ensures you don't hand over more to the government than you need to. As a recent analysis by Chartered Professional Accountants of Canada highlights, meticulous record-keeping is the cornerstone of a compliant and optimized tax return for property owners.

At the end of the day, your tax bill comes down to one simple formula:

Gross Rental Income - Deductible Expenses = Net Rental Income (or Loss)

Getting a handle on this calculation is the first real step toward managing your investment property like a pro.

Gathering Your Numbers: What You’ll Need

Before you can even touch a calculator, you need to pull together all your financial data for the year. This part can feel a bit like a scavenger hunt, but having everything organized makes the rest of the process a breeze. You’re essentially looking for two piles of information: all the money that came in, and all the money that went out to keep the property running.

Here’s a quick rundown of the essential data points you’ll need for any Maple Ridge rental.

Essential Data for Your Tax Calculation

Data PointWhat It Is & Real-World ExampleGross Annual RentThe total rent you collected from your tenants over the year. Example: Your tenant pays $2,500/month, so your gross annual rent is $30,000.Other IncomeAny extra money the property generated, like fees for parking spots or coin-operated laundry. Example: You collect $600 in parking fees for the year.Mortgage InterestOnly the interest portion of your mortgage payments is deductible, not the principal. Example: Your annual mortgage statement shows you paid $12,000 in interest.Property TaxesYour annual municipal property tax bill for the rental property. Example: In 2024, Maple Ridge approved a 5.71% municipal tax increase, so your tax bill might be higher than last year. Let's say it was $3,695.InsuranceThe premium for your landlord or rental property insurance policy. Example: Your annual insurance premium cost $1,200.UtilitiesAny utilities you paid for, like hydro, gas, or water, if they weren't covered by the tenant. Example: You paid $900 for the property's water bill.Repairs & MaintenanceCosts for keeping the property in good shape, from fixing a leaky faucet to painting a room. Example: You spent $750 on a plumber and new paint.Management FeesIf you use a property manager, their fees are a deductible expense. Example: You paid a property management company $3,000 over the year.Other ExpensesThis can include advertising costs, legal fees, or travel expenses to manage the property. Example: You spent $150 on online ads to find a new tenant.

Once you have these figures tallied up, you're ready to plug them into the calculator and see where you stand.

For many landlords, juggling the day-to-day of leases, maintenance requests, and legal compliance is more than a full-time job. It’s why many choose to partner with professional property management services. This frees them up to focus on the financial big picture while an expert team handles the operational details.

Organizing Your Rental Income and Expense Records

Before you even think about plugging numbers into a rental income tax calculator, the real work begins with getting your financial house in order. An accurate tax filing is built on a foundation of solid, year-round record-keeping. To get the full financial picture of your Maple Ridge property, you need to track every dollar coming in and going out.

On the income side, it’s about more than just rent. Gather all your bank statements that show rent deposits, of course, but don't forget about other revenue streams. Did you collect fees for extra parking spots or coin-operated laundry? That all counts.

The expense list, as any landlord knows, is usually much longer.

One of the best pieces of advice I can give is to keep your personal and rental finances completely separate. The Canada Revenue Agency (CRA) loves to see a dedicated bank account for the property. It creates a clean, easy-to-follow paper trail for all your income and expenses, which is invaluable if you're ever audited.

This one simple habit will save you a world of headaches come tax time.

Now, let's start collecting. You'll need your mortgage statements to isolate the interest paid (a key deduction!), property tax bills from the City of Maple Ridge, and your insurance policies. And then there are the receipts—for every single repair, big or small. Don’t overlook the utility bills you cover for your tenants or any invoices from property managers or tradespeople. Every slip of paper is a potential deduction.

Finding Every Eligible CRA Deduction for Your Property

This is where so many landlords leave money on the table. It’s easy to do, but missing out on eligible deductions is one of the biggest—and most common—mistakes I see. The Canada Revenue Agency (CRA) actually allows for a whole range of expenses that can significantly lower your taxable income, which is precisely what a good rental income tax calculator is designed to show you.

Before you start tallying up receipts, there's one critical distinction you have to get right: the difference between current and capital expenses.

Current vs. Capital Expenses Explained

Here’s the simplest way I explain it to my clients: Fixing a leaky faucet or a broken dishwasher? That’s a current expense. It's a repair to keep things running, so you can deduct the full cost in the same year you paid for it.

But what if you decide to rip out that old dishwasher and install a brand-new, high-efficiency model as part of a kitchen upgrade? That’s a capital expense. Because it provides a lasting benefit and improves the property's value, you can't write it all off at once. Instead, you'll claim a portion of its cost over several years through the Capital Cost Allowance (CCA).

Getting this right is fundamental to maximizing your returns. The CRA has clear rules, but it's also a common red flag for audits if a major purchase gets misclassified as a simple repair.

Beyond the big stuff, many Maple Ridge landlords I work with often forget about the smaller, recurring costs that really add up. Don't overlook these valuable deductions:

- Travel costs when you drive to your property for an inspection or repair.

- The strata fees you pay every month.

- Any advertising expenses you paid to find those great tenants.

Figuring Out Your Net Rental Income

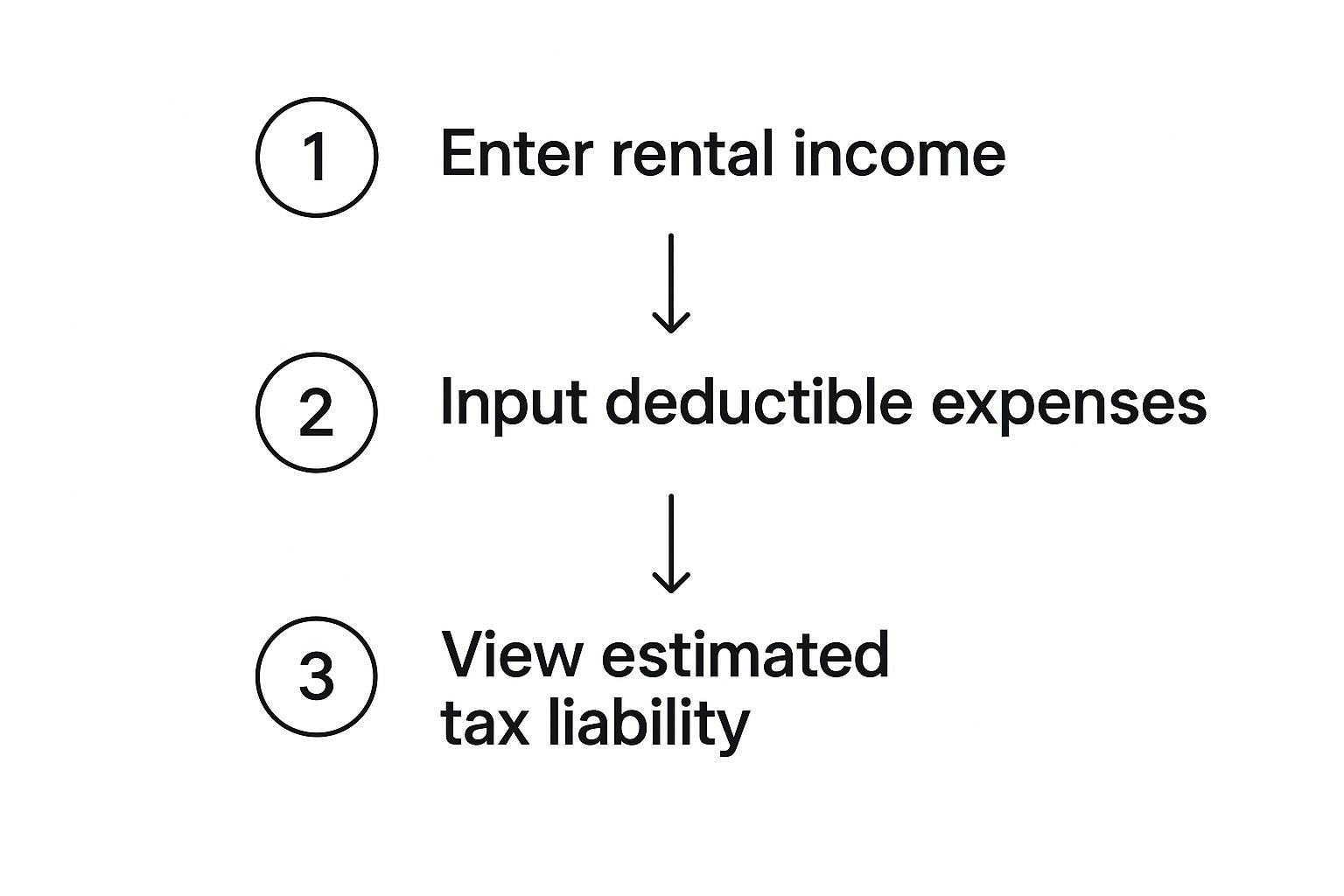

Alright, with all your paperwork gathered, it’s time to actually crunch the numbers. This is where you’ll use a rental income tax calculator to get a clear picture of your financial position. It’s all about systematically accounting for every dollar that comes in and goes out.

Start by plugging in your total gross rental income. Next, you’ll work through all those expense categories you organised, entering the figures for things like property taxes, insurance, and any repairs you had to do.

One of the most important numbers here is your mortgage interest—this is often a huge deduction. A good tip is to figure this out ahead of time, which you can do with a tool like our online mortgage payment calculator. You’ll also want to pay close attention to the Capital Cost Allowance (CCA). This lets you depreciate major assets, like the building itself or that new fridge you installed, which can lower your taxable income over several years.

This infographic breaks down the core calculation into a simple visual.

As you can see, it’s a straightforward process. Following these steps will take your raw numbers and turn them into a clear, understandable tax estimate.

Making Your Tax Results Work for You

That final number you get from a rental income tax calculator isn't just for the CRA. Think of it as a financial health report for your Maple Ridge investment property. How you read that report can completely reshape your strategy for the year ahead.

For instance, if you're looking at a net rental income, that number tells you exactly how much extra tax you’re on the hook for at your personal marginal rate. Seeing that figure in black and white can be a real wake-up call, pushing you to make smarter financial moves.

A high taxable income from your rental might be the perfect nudge to boost your Registered Retirement Savings Plan (RRSP) contributions. Doing that can directly chip away at the amount you owe. For the 2023 tax year, the contribution limit was 18% of your previous year's earned income, up to a maximum of $30,780.

On the flip side, a net rental loss isn't necessarily bad news. In many cases, you can use that loss to bring down your taxable income from other places, like your day job.

This isn't just about filing taxes. It's about turning a yearly chore into a powerful tool for managing your entire investment portfolio and building wealth over the long haul.

Even with a solid rental income tax calculator, I find landlords in Maple Ridge often run into the same handful of questions. It's completely normal, especially when you're trying to get everything right for the CRA.

One of the most common questions I hear is about mortgage payments. Can you deduct the whole thing? The short answer is no. You can only claim the interest portion of your payment, not the principal that pays down your loan.

Another frequent one is what to do if you have a rental loss. If your expenses for the year end up being more than your rental income, you can typically deduct that loss against your other sources of income. This can be a real silver lining, as it might actually lower your overall tax bill.

If I could give just one piece of advice, it would be this: open a separate bank account just for your rental property. It’s not an official CRA rule, but trust me, it creates a perfectly clean audit trail that makes your bookkeeping a thousand times easier.

For more answers to common landlord questions, take a look at our library of landlord resources.

Ready to take the guesswork out of managing your Maple Ridge investment? Let Royal LePage Brookside Realty handle the details, from tenant screening to financial reporting. Visit us at https://www.brookside-pm.ca to learn more.