Before you even think about scrolling through listings in Maple Ridge or Pitt Meadows, the real work begins. It’s not as exciting as picturing your furniture in a new living room, but getting your finances sorted is the single most important step you can take.

This is where you go from just dreaming about a home to being a serious, qualified buyer. It’s all about figuring out your real purchasing power, not just a ballpark number, and getting a clear picture of every cost involved.

Getting a Real Mortgage Pre-Approval

Think of a mortgage pre-approval as your golden ticket. It’s not some five-minute online calculator; it's a formal review where a lender digs into your income, credit score, and debts to tell you exactly how much they’re willing to lend you.

Having that pre-approval letter in your back pocket changes everything:

- It sets your budget in stone. No more wasting time looking at homes you can’t afford. You know your numbers, and you can search with confidence.

- It makes your offer powerful. In a competitive market like the Fraser Valley, sellers want to see that you're a sure thing. A pre-approval shows them you’re financially ready to close the deal.

- It puts you in the fast lane. Since the lender has already done most of the heavy lifting, your final mortgage approval will be much faster once your offer is accepted.

A pre-approval letter is what separates the lookers from the buyers. It signals to everyone—sellers and their agents—that you're serious and ready to act.

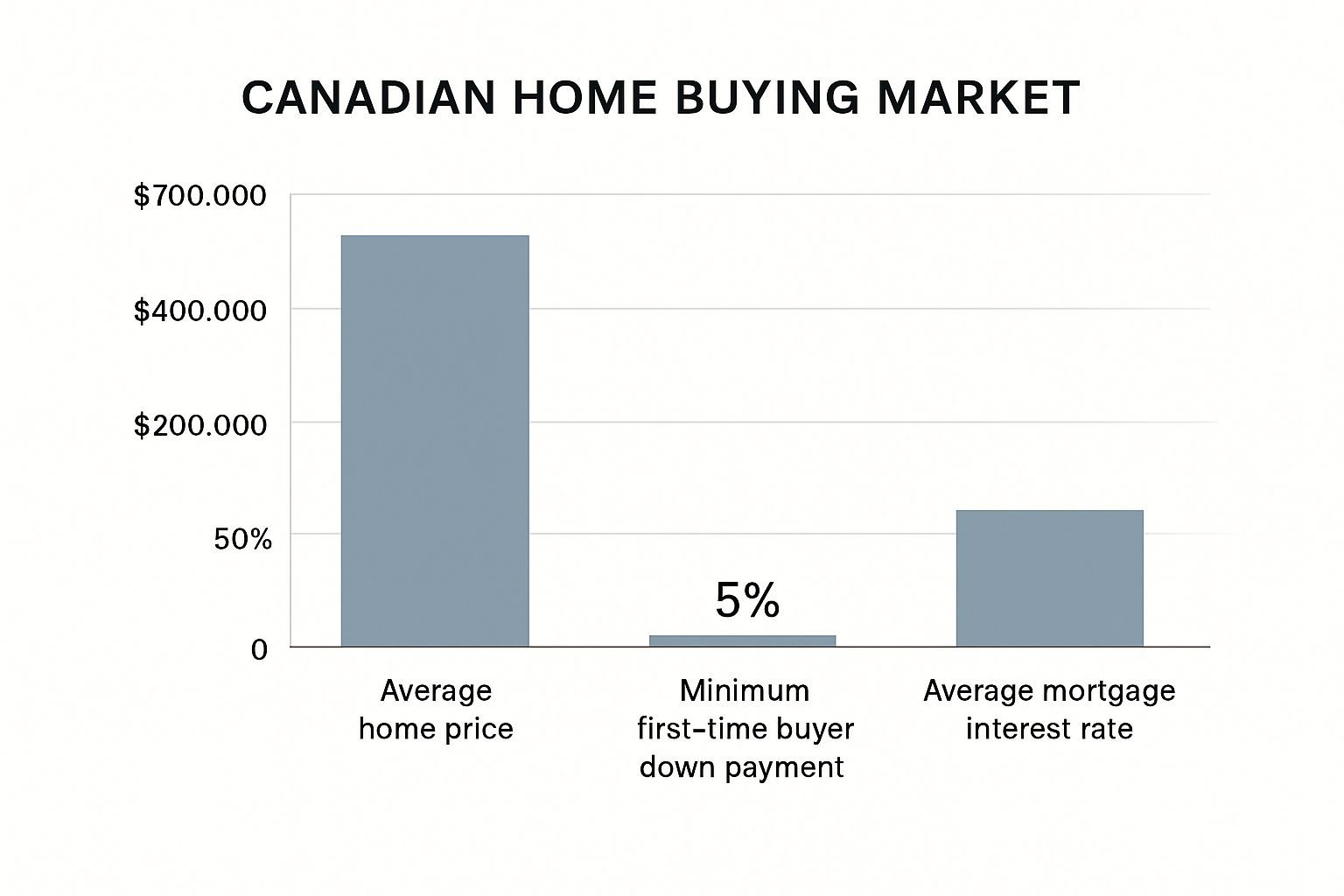

Nailing Down Your Down Payment

Your down payment is a massive piece of the financial puzzle. A critical first move is to calculate your down payment on a house, which helps you see how different loan options and closing costs fit together.

In Canada, the minimum you need to put down is based on the home's price. For homes under $500,000, the minimum is 5%. If you’re looking at homes between $500,000 and $999,999, it’s 5% on the first $500,000 and 10% on whatever is left.

But here’s the catch: if you put down less than 20%, you’ll have to get mortgage loan insurance. This protects your lender in case you default, and the premium is usually just rolled into your total mortgage balance.

The Closing Costs No One Talks About

Your down payment is the big one, but it’s not the only cheque you’ll be writing. I’ve seen too many first-time buyers get blindsided by closing costs—the one-time fees needed to actually seal the deal.

Here in British Columbia, you should budget an extra 1.5% to 4% of the home's purchase price for these expenses. They can add up fast. To get a handle on what your total monthly outlay might look like, our mortgage payment calculator is a great tool for seeing the whole picture.

Fraser Valley Closing Cost Estimates

Below is a realistic look at the one-time expenses a home buyer in Maple Ridge, Pitt Meadows, or Mission can expect to pay.

These are the real-world costs of finalizing your purchase, so be sure to have these funds ready and available in addition to your down payment.

Finding the Right Real Estate Professionals

Trying to navigate the Fraser Valley’s real estate market alone is like hiking a mountain without a map. Sure, you might eventually get there, but you’re bound to hit some dead ends and miss out on the best views. Assembling a team of dedicated professionals isn't a luxury; it’s a non-negotiable part of buying a home in Canada.

Think of this team as your personal board of directors for the biggest purchase of your life. They’re your guides, your advocates, and your safety net, each with a specific job to do—from finding the perfect spot to making sure the deal is financially and legally rock-solid.

Let's break down who you need in your corner.

Choosing Your Real Estate Agent

Your real estate agent does a whole lot more than just unlock doors. In a market as unique as the Fraser Valley, a great local agent is your source for the kind of on-the-ground intel you’ll never find online. They are your strategic partner, plain and simple.

When you're looking for an agent to help you buy in Maple Ridge, Pitt Meadows, or Mission, you need to prioritize hyper-local expertise. You need someone who knows which quiet street is about to become a major thoroughfare, which schools have the best reputations, and what new community developments are just around the corner. That’s the kind of insight that turns a good buy into a fantastic long-term investment.

Here’s what to look for:

- Local Market Fluency: Does the agent actually work in your target neighbourhoods? Ask them to show you some of their recent sales in those specific areas.

- Strong Communication: You need someone who is responsive and keeps you in the loop, not someone you have to chase for updates. They should be proactive, not reactive.

- Top-Notch Negotiation Skills: A seasoned agent knows how to write an offer that gets noticed and can skillfully handle counter-offers to get you the best possible terms.

Finding the right agent really comes down to connection and trust. Make sure you interview at least two or three people. You need to find someone whose style and personality click with yours, because this relationship will be pivotal to your success.

Your Financial and Legal Allies

While your agent is leading the house hunt, two other key players are working behind the scenes to make sure your purchase is secure. A mortgage broker and a real estate lawyer (or notary) are essential members of your team, protecting your financial and legal interests every step of the way.

A mortgage broker works for you, not for a specific bank. Their entire job is to take your application and shop it around to a wide range of lenders—from the big banks to smaller credit unions—to find you the best possible interest rate and mortgage terms. This can save you a ton of time and often gets you a much better deal than you could find on your own.

Your real estate lawyer or notary takes over once your offer is accepted. They handle all the complicated legal paperwork needed to officially transfer the property into your name. Their role is absolutely critical.

Here's what your legal expert will manage:

- Title Search: They dig into the property’s history to make sure there are no hidden liens, debts, or claims against it that could come back to haunt you.

- Document Review: They’ll meticulously review every contract and mortgage document to ensure your rights are protected and there are no nasty surprises.

- Transfer of Funds: On closing day, they manage the secure transfer of your down payment and mortgage funds from the lender to the seller.

- Registration: The final step. They register your name on the property title with the provincial Land Title Office, which officially makes you the new owner.

Putting together this "trifecta" of an agent, broker, and legal expert early on gives you a solid foundation. With them on your side, you can move forward with confidence and clarity, knowing you’re in good hands.

How to Find the Right Home in the Fraser Valley

You’ve got your financing lined up and a great agent by your side—now for the exciting part. The house hunt is where the abstract idea of a new home starts to feel real. It's incredibly easy to get swept up in beautiful listing photos and charming open houses, but a strategic approach will save you a ton of time and prevent headaches down the road.

The key is to move beyond a generic wish list. Instead of just saying "three bedrooms," dig deeper into why you need them. Is one for a home office, another for a growing family, or a third for frequent guests? Understanding the 'why' behind your list is what will truly guide your search.

Defining Your Must-Haves and Nice-to-Haves

Every home search starts with a dream list, but reality often demands a few compromises. The most effective way to start is by separating your absolute needs from your wants. This simple framework keeps you focused and prevents you from getting distracted by a newly renovated kitchen in a neighbourhood that adds an hour to your commute.

Grab a notepad and create two distinct lists:

- Must-Haves: These are your non-negotiables. If a property doesn't tick these boxes, you walk away, no matter how nice the countertops are. This could include a minimum number of bedrooms, a specific school catchment, or a main-floor primary bedroom for accessibility.

- Nice-to-Haves: These are the features you’d love but can live without. Think stainless steel appliances, a finished basement, or a south-facing garden. They’re fantastic bonuses, not deal-breakers.

Being brutally honest about these priorities from the get-go makes the entire process so much smoother. You and your agent can filter listings efficiently, ensuring you only spend your valuable time on properties that are serious contenders.

Exploring Fraser Valley Neighbourhoods

The Fraser Valley isn’t just one place; it’s a collection of unique communities, each with its own distinct character and lifestyle. A home in central Maple Ridge offers a completely different vibe than a property in rural Mission or a quiet corner of Pitt Meadows.

Get a feel for the local flavours:

- Maple Ridge: This is where you'll find a fantastic blend of city amenities and stunning natural beauty. There’s everything from family-friendly subdivisions near great schools to more secluded properties just a stone's throw from Golden Ears Provincial Park.

- Pitt Meadows: Known for its flat landscapes, agricultural roots, and a tight-knit community feel. It's ideal for those who appreciate a slightly slower pace but still need excellent commuter access via the West Coast Express.

- Mission: Often provides more affordability along with breathtaking views of the Fraser River. It attracts buyers looking for larger lots and a closer connection to the outdoors, with plenty of lakes and trails right at your doorstep.

Spend a weekend in your top-choice neighbourhoods. Don't just drive through—park the car. Grab a coffee at a local cafe, walk through the parks, and maybe even drive the commute during rush hour. The goal is to find a community that feels like home, not just a house that looks good online.

Looking Beyond the Staging

Home staging is powerful. It’s professionally designed to make you fall in love, but your job is to look past the cozy throw blankets and fresh paint. During a viewing, you need to train your eyes to spot the things that truly matter—the potential red flags that could cost you serious money and stress later on.

Pay close attention to the subtle clues:

- Signs of Water Damage: Look for faint discolouration on ceilings (especially under bathrooms), bubbling paint along baseboards, or a distinct musty smell in basements and closets.

- Foundation and Floor Issues: Are there large, spiderwebbing cracks in the foundation outside? Inside, do the floors feel sloped or uneven as you walk across them? These are not things to ignore.

- The Age of Major Systems: Take a peek at the furnace, hot water tank, and roof. If they look ancient, they’re likely nearing the end of their lifespan—a significant future expense you'll want to budget for.

Visiting a property at different times is also a smart move. That quiet street you saw on a Saturday morning might be a busy shortcut for commuters on a Tuesday afternoon. For a more detailed look into what we offer, you can review our comprehensive approach to buying a home.

The Canadian housing market is always on the move. Recent data from the Fraser Valley Real Estate Board shows a significant 46% increase in new listings in April 2024 compared to the previous year, giving buyers more options and helping to balance the market. This shift suggests a more favourable environment for purchasers compared to the intense seller's markets of the past. You can learn more about these trends and what they mean for your search by exploring the latest Canadian housing market outlook.

Crafting an Offer That Gets Accepted

After what feels like countless viewings, you’ve finally found it. That one home that just clicks, the one you can already picture your life in. Now for the make-or-break moment: turning that feeling into a formal, written offer. This is where the process gets real, blending strategy with a bit of finesse. Every single detail counts.

A winning offer is so much more than just the price tag. Think of it as a complete package designed to impress the seller while keeping you protected. Things like your deposit amount, your ideal closing date, and the conditions you include—they all shape how your offer lands.

The Anatomy of a Winning Offer

Your offer is essentially a business proposal. It needs to be clear, compelling, and built on a solid foundation. Your agent will draft the official Contract of Purchase and Sale, which lays out all the critical details.

Here’s a breakdown of what a strong offer in BC includes:

- Purchase Price: This is the big number—what you're offering to pay for the property.

- Deposit: A good-faith payment made once your offer is accepted. It's typically around 5% of the purchase price and is held in trust, showing the seller you’re serious.

- Dates: This is all about timing. You'll have a completion date (when the money and title change hands) and a possession date (when you get the keys). If you can align these with the seller's schedule, your offer instantly becomes more appealing.

- Subjects (Conditions): These are your escape hatches. Think of them as crucial safety nets that must be met for the deal to become final.

A well-crafted offer is a balancing act. Sometimes, being flexible on your dates or offering a slightly larger deposit can be just as powerful as a higher price, especially if the seller is hoping for a quick, hassle-free sale.

Using Subjects to Protect Yourself

In British Columbia, subjects are a buyer’s best friend. They give you a set amount of time, usually 7-10 business days, to do your homework without being locked into a deal you might regret. If any of your conditions aren’t met to your satisfaction, you can walk away and get your deposit back.

These are the most common subjects you’ll want to include:

- Subject to Financing: This gives you time to get the final, unconditional mortgage approval from your lender. A pre-approval is a great start, but the bank still needs to give the thumbs-up on the specific property.

- Subject to Home Inspection: This is non-negotiable. It allows you to bring in a professional inspector to give the home a top-to-bottom check-up. It's your single best defence against hidden nightmares like a leaky roof or foundation cracks.

- Subject to Property Disclosure Statement (PDS) Review: The PDS is a form where the seller discloses any known issues. This subject gives your lawyer a chance to comb through it for potential red flags.

- Subject to Title Search: Your legal representative will pull the property's title to make sure there are no surprise liens, claims, or other issues that could cloud your ownership.

Thinking about waiving these subjects to make your offer look better is incredibly risky. It’s a move you should only ever consider after a very serious conversation with your agent and lawyer.

Navigating Negotiations and Multiple Offers

Once your offer is submitted, one of three things will happen: the seller accepts it as is, rejects it outright, or sends back a counter-offer. A counter might tweak the price, shift the dates, or change other terms. This is where your agent’s negotiation chops really come into play, guiding you through the back-and-forth to land on a deal that works for everyone.

The Fraser Valley market often throws another curveball: multiple-offer scenarios. Finding yourself in a bidding war against other eager buyers can be nerve-wracking, but the key is to stay cool and strategic. Your agent will prepare a Comparative Market Analysis (CMA), which shows what similar homes nearby have recently sold for. This data helps you anchor your offer to the home's true market value.

Curious how this works for your own place? You can get a free home evaluation to see the process in action.

When you're in a competitive situation, you want to put your best foot forward, but you absolutely must have a walk-away price in mind. It's easy to get swept up in the emotion of "winning," but that's a fast track to overpaying. Trust your budget, rely on your agent’s advice, and be ready to let a property go if the numbers stop making sense.

Getting From an Accepted Offer to Keys in Hand

Getting that call—"they've accepted your offer!"—is a huge moment. It's when your dream home finally starts to feel real. But before you break out the packing tape, there's a crucial sprint ahead known as the subject removal period.

Think of this as your built-in safety net. It's a non-negotiable part of the process that gives you time to do your due diligence, ensuring you’re making a sound investment.

This period is your chance to finalize your mortgage, get a professional home inspection, and make sure the property is everything it appears to be, both on paper and in person. Let's walk through what happens in these final, critical days before closing.

Tackling Your Conditions

Once the seller accepts your offer, the clock starts ticking on your subject removal period. This is when you and your team get to work satisfying the conditions, or "subjects," you included in your contract. The two big ones are almost always financing and a home inspection.

Your mortgage broker will immediately send the lender all the property details, including the MLS® listing and the accepted purchase agreement, for their final sign-off. The lender will almost certainly order an appraisal at this point to make sure the home's value supports the price you’re paying. It's a key step that protects both you and them.

At the same time, you'll need to book a qualified home inspector to go through the house from top to bottom. Don't even think about skipping this, not even for a brand-new home in Pitt Meadows or a pristine-looking condo in Maple Ridge. An inspector is your unbiased expert, trained to find potential issues you’d never spot on your own.

The Home Inspection Report: Your Negotiation Superpower

The home inspector's report is one of the most powerful tools you have. It's a detailed breakdown of the home's major systems—roof, foundation, electrical, plumbing, you name it. It identifies existing problems and flags things that might need attention down the road.

Don't panic when the report comes back with a list of issues; no home is perfect. The real skill is learning to separate minor fixes from major red flags.

- Minor Issues: Think leaky faucets, a cracked window pane, or a sticky door. These are common and usually easy to fix.

- Major Red Flags: This is the serious stuff. Evidence of foundation trouble, an old roof that’s on its last legs, outdated knob-and-tube wiring, or signs of significant water damage.

If the inspection turns up something serious, that report becomes your leverage. You can go back to the seller and ask them to fix the issues before closing day or provide a price reduction so you can handle the repairs yourself. And if the problems are just too big? This subject gives you the power to walk away from the deal with your deposit fully intact.

The Final Stretch: Your Lawyer or Notary Takes Over

Once you've satisfied your conditions and provided written notice to remove subjects, the deal is officially firm. Now, all the paperwork heads to your real estate lawyer or notary. They handle all the complex legal work needed to transfer the property title into your name.

About a week before the completion date, you'll meet with them to sign what feels like a mountain of documents. One of the most important is the Statement of Adjustments. This document breaks down every dollar, showing you the exact amount of money you need to bring in for closing. It includes:

- The rest of your down payment.

- Your legal fees.

- Property Transfer Tax (if it applies to you).

- Adjustments for any property taxes or strata fees the seller already paid.

Careful financial planning here is essential. The shifting demographics of Canadian homebuyers show it's taking people longer to save for a home, with buyers over 35 now making up 39% of the market. You can read more about how the financial landscape for homebuyers is changing to understand the broader context.

After you've signed everything, your lawyer works with your lender and the seller’s lawyer to get the funds transferred and the title registered in your name on completion day. Once it's all official, you’ll get the call you've been waiting for: it's time to come pick up your keys!

If you have any questions about this stage of the process, our team is always ready to help; please feel free to contact us for guidance.

Your BC Home Buying Questions Answered

Even with a detailed roadmap, buying a home in BC can feel like you’re left with a handful of nagging questions. The real estate world—especially in fantastic communities like Maple Ridge, Pitt Meadows, and Mission—moves to its own beat, with its own set of rules. This section is all about tackling those common "what ifs" and "how does thats" head-on, giving you clear, straightforward answers so you can move forward with confidence.

Think of this as your personal FAQ for demystifying those final, critical details. Getting a solid grip on everything from provincial taxes to your rights during an inspection can be the difference between a smooth closing and a costly surprise.

What Is the BC Property Transfer Tax and Will I Have to Pay It?

The Property Transfer Tax (PTT) is a one-time tax the BC government charges whenever a property title changes hands. It's one of the biggest closing costs you'll encounter, so it's absolutely vital to budget for it right from the start.

The tax is calculated on a tiered basis, using the property's fair market value:

- 1% on the first $200,000

- 2% on the portion from $200,001 up to $2,000,000

- 3% on any amount over $2,000,000

But there’s some good news, especially for first-timers. The government's First-Time Home Buyers' Program offers a full or partial exemption from the PTT. To get it, both you and the property have to tick certain boxes, including price thresholds that change over time. It's so important to have your agent or lawyer check the latest government rules to see if you qualify for this huge saving.

How Long Is a Typical Subject Removal Period in the Fraser Valley?

In most deals here in the Fraser Valley, the subject removal period typically runs for 7 to 10 business days. This is your golden window to do all of your homework—your due diligence—without being legally locked into the purchase. It's the time you'll use to get your final mortgage approval nailed down and bring in a professional for a thorough home inspection.

That timeframe isn't set in stone, though. It’s a point of negotiation. If you’re in a hot market with multiple offers, your agent might advise a shorter period to make your offer shine. On the flip side, if you're looking at an older home that might need a closer look, you'd want to negotiate for a longer period to investigate properly.

What Happens to My Deposit If I Cannot Remove My Subjects?

Your deposit money is held safely in a real estate brokerage's trust account—it never goes directly to the seller. This is a critical layer of protection for you as a buyer. If you genuinely can't satisfy one of the conditions (or "subjects") in your offer, the contract becomes void, and you get your deposit back in full.

For example, if the bank won't give you final financing approval despite your best efforts, or an inspection uncovers a cracked foundation, you can walk away. The key is that you must show you acted in good faith to try and meet the conditions. This is exactly why subjects are your safety net. Our clients constantly tell us what a relief this protection was, and you can see what they have to say in our client success stories.

The subject removal period is your last chance to walk away from a deal without penalty. It’s your time to verify that the home and your finances are exactly what you thought they were, protecting you from making a decision you might regret.

Should I Get a Home Inspection on a New Build or Condo?

Absolutely. It’s tempting to think a brand-new home is perfect or that a condo strata council has everything covered, but an independent home inspection is still one of the smartest investments you can make. New construction can have deficiencies, sloppy finishing, or system issues that you'd never spot on your own.

For a new build in Mission, for example, an inspector can create a punch list of items the builder needs to fix under warranty before you take possession. With a condo in Maple Ridge, the inspector will focus on the systems inside your unit that are your personal responsibility—things like the electrical panel, plumbing fixtures, and appliances. The report gives you an unbiased, professional opinion, ensuring you start your homeownership journey with your eyes wide open.

At Royal LePage Brookside Realty, we live and breathe this stuff. We're here to guide you through every twist and turn of buying a home with clarity and the local expertise that only comes from experience. Whether you’re buying your first home or adding to your investment portfolio in the Fraser Valley, our team is ready to make your experience a success.

Ready to get started? Visit us at https://www.brookside-pm.ca to connect with one of our experienced agents today.