A typical home appraisal in Vancouver and the Fraser Valley will usually run you somewhere between $400 and $700 for a standard single-family home. But this isn't just a simple fee for a quick look-around. That cost reflects the appraiser's professional expertise and the detailed, meticulous work that goes into figuring out your property's true market value.

What Is the Real Cost of a Home Appraisal in Vancouver?

Think of a home appraisal not as a cost, but as a crucial investment in your real estate transaction. It's a fundamental piece of financial due diligence. Lenders absolutely depend on this unbiased, third-party valuation to confirm that a property is actually worth the amount of money they’re about to lend.

This professional opinion is critical for everyone at the table in the Metro Vancouver and Fraser Valley markets. An accurate appraisal protects the bank, the buyer, and the seller by making sure the price everyone agreed on is grounded in current market reality. Before we get into the nitty-gritty of the costs, it's really helpful to get a solid handle on what a property appraisal entails.

Why Appraisals Are Non-Negotiable in BC Real Estate

In a competitive and often heated market like ours, an appraisal acts as an objective, impartial referee. It cuts through the emotional attachment a seller might have or an overly ambitious asking price to deliver a valuation rooted in cold, hard data. It’s a required step for nearly all mortgage approvals and refinancing applications for a reason.

If you're getting ready for selling your home, a pre-listing appraisal can give you a realistic pricing strategy right out of the gate, preventing your home from languishing on the market. For buyers, it provides the essential peace of mind that you aren't overpaying.

An appraisal provides an independent, impartial, and objective opinion of value. It's a cornerstone of responsible lending and a vital tool for making informed decisions in BC's complex property market.

What an Appraisal Delivers

So, what are you actually paying for? The fee covers a comprehensive and detailed report that dives deep into a number of key factors.

- Recent Sales Data: The appraiser analyzes what comparable properties have recently sold for in your specific neighbourhood, whether that's in Maple Ridge or Yaletown.

- Property Condition: This involves a thorough inspection of the home's interior and exterior, taking into account its age, features, and overall condition.

- Market Trends: They'll assess the current local real estate climate, which can shift on a dime here in the Lower Mainland. According to the Real Estate Board of Greater Vancouver, market conditions can significantly influence property values, making this analysis critical.

- Location Specifics: The desirability of the area, how close you are to schools and parks, and other unique geographical factors all play a part.

Understanding this process makes it clear why the home appraisal cost isn't a one-size-fits-all number—it directly reflects the depth of research required to produce a valuation that is both reliable and defensible.

Key Factors That Influence Your Appraisal Fee

The final number on your appraisal quote isn't just pulled out of thin air. It’s a direct reflection of the appraiser's time, effort, and expertise needed to accurately value your specific property. Figuring out the variables at play helps make sense of why one home appraisal cost can be so different from another.

Think of it like hiring a contractor. Painting a simple, square room is straightforward. But painting a room with vaulted ceilings, intricate trim, and a bunch of alcoves? That takes more time, skill, and therefore costs more. An appraisal works on the very same principle—complexity dictates the price.

Property Size and Complexity

Right off the bat, the biggest factor is the sheer size and complexity of your home. It's only natural that a larger property with more rooms, outbuildings like a workshop or laneway house, or extensive grounds will take longer to inspect and measure than a standard three-bedroom home in a subdivision.

Unique architectural features also add layers to the job. An appraiser will need more time to research and find comparable sales for a custom-built home with a one-of-a-kind design or a waterfront property in Maple Ridge, compared to a cookie-cutter townhouse. The more unique the property, the deeper the investigation has to go.

Location and Property Type

Where your home is located plays a huge role in the process. An appraiser valuing a condo in a dense downtown Vancouver neighbourhood has a wealth of recent, highly comparable sales data within a few city blocks. This can often make the valuation process a bit more straightforward.

On the other hand, a rural property out in the Fraser Valley might have very few direct comparables. This forces the appraiser to expand their search area and make more complex adjustments to arrive at an accurate value. Travel time to these more remote properties also gets factored into the final fee.

At its heart, an appraisal is all about comparison. The easier it is to find directly comparable properties that have recently sold, the more straightforward the valuation becomes. A lack of good data means more in-depth analysis is required, and that means a higher fee.

Purpose of the Appraisal

Finally, the reason you need the appraisal changes the scope of work and the type of report required. Different situations demand different levels of detail, which has a direct impact on the cost.

- Mortgage Financing: This is the most common reason for an appraisal. It requires a full, detailed report for the lender to assess their risk before they hand over the money.

- Refinancing: Much like a purchase mortgage, refinancing usually requires a full appraisal to determine the property's current market value for the new loan.

- Estate Settlement or Divorce: These appraisals can be more complex. They might need to establish a historical value (like the value on a specific date in the past) and must be rock-solid enough to hold up in legal proceedings.

- Capital Gains Tax: This requires pinning down the property's value on a specific date to calculate tax liabilities accurately.

Each of these purposes requires a tailored approach, which influences the appraiser's research and the final report's format. All of this is reflected in the overall home appraisal cost.

Typical Appraisal Cost Ranges in BC's Lower Mainland

Now that we've unpacked the factors that shape an appraiser's fee, let's talk numbers. Budgeting for your home appraisal cost is a whole lot easier when you have a solid idea of the typical price ranges across the Lower Mainland, from Vancouver's dense urban core to the sprawling communities of the Fraser Valley.

Generally speaking, you can expect to pay somewhere between $400 and $700 for a standard appraisal report on a single-family home. Think of this as a starting point. The final fee will always circle back to the specific details of your property and where it's located, just as we discussed.

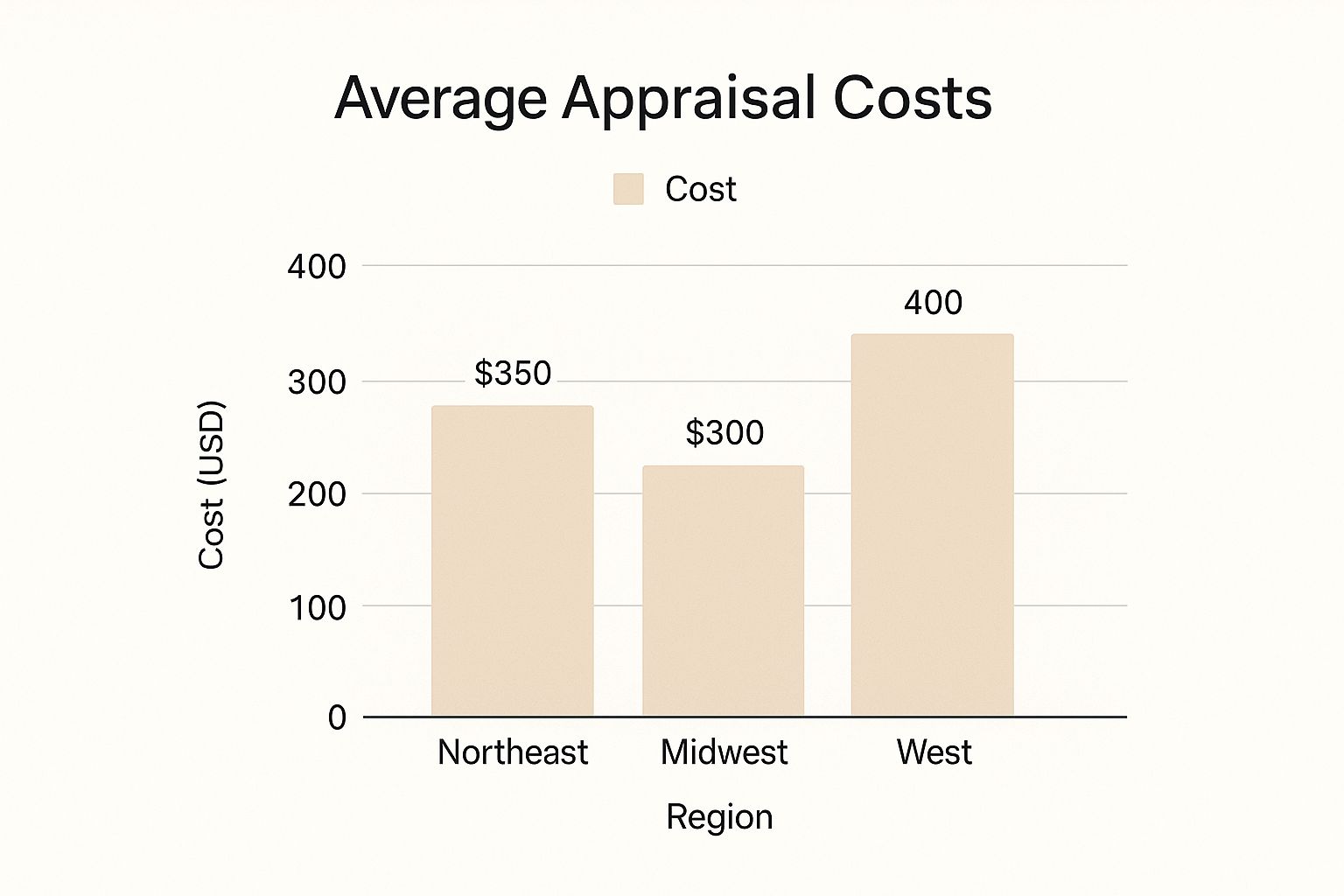

The image below gives you a quick visual on how appraisal costs can shift from one region to another, really driving home the point that location is a major factor.

As you can see, costs can vary quite a bit between major areas, and that's a trend we see right here within British Columbia as well.

To give you a clearer picture, here’s a breakdown of what you might expect to pay for different property types in Vancouver versus the Fraser Valley. This table outlines the typical fee ranges and the key variables at play.

Estimated Home Appraisal Costs in Vancouver & Fraser Valley

These figures help set a realistic budget, but remember that a unique or complex property will always command a higher fee due to the extra research and analysis required.

Diving Deeper into Costs by Property Type

The kind of home you own is easily one of the biggest variables. Each property type demands a different level of analysis, especially when it comes to finding comparable sales and navigating things like strata ownership.

Single-Family Detached Homes: These are the benchmark. Appraisals for detached homes in Vancouver and the Fraser Valley usually land in that $400 to $700 range. If your home has unique features or is in a more remote spot, expect the cost to be on the higher end of that scale.

Townhouses and Duplexes: The work involved here is often quite similar to a detached home, so the costs are comparable, typically running from $450 to $650. The appraiser has to consider not just your unit but also the shared property elements and how they add value.

Strata Condominiums: Appraising a condo can sometimes be a bit more straightforward, mainly because there are often plenty of similar, recently sold units in the same building or complex. This often brings their appraisal costs into the $375 to $550 range, assuming it's a standard unit.

How Location Impacts the Price: Vancouver vs. The Fraser Valley

Geography really matters. The cost of doing business, the time spent in traffic, and the availability of good comparable data can be worlds apart when comparing Vancouver to communities like Maple Ridge or Mission.

An appraisal for a home in West Vancouver might cost more than for an identical home in Abbotsford. This often comes down to higher property values, the added complexity of luxury features, and even more travel time for the appraiser stuck in a congested urban area.

In contrast, while a property in the Fraser Valley might mean more driving for the appraiser, the homes can sometimes be more uniform, which can make the valuation process a bit quicker.

Understanding these regional differences is a huge part of the process when you're buying a home in either market. By getting a localized quote, you can make sure your budget for closing costs is spot-on and avoid any unwelcome surprises.

Comparing Different Types of Property Appraisals

Not every property valuation is a full, top-to-bottom inspection. The kind of appraisal your lender asks for really depends on the situation, and the amount of work involved is what directly drives the home appraisal cost. Getting a handle on these differences helps make sense of what you're actually paying for.

The reason for the appraisal—whether it's for a brand-new mortgage, a straightforward renewal, or a refinance—dictates the level of detail required. Each type of report serves a different purpose and gives the lender a different degree of confidence in the property's value.

The Standard Full Appraisal

This is the big one—the most thorough and common type of appraisal you'll see, especially for new home purchases here in Vancouver and the Fraser Valley. A full appraisal, often called a Form 1004 in other markets, means a licensed appraiser conducts a complete interior and exterior inspection of your property.

The appraiser physically shows up, measures the home, checks out the condition of everything from the roof to the basement, and makes notes of any recent upgrades or potential issues. They’ll take plenty of photos, too. All this on-the-ground information is then crunched alongside data from recent comparable sales in your neighbourhood to pin down the property's market value. Because it’s the most hands-on and time-consuming, it naturally comes with the highest price tag.

Drive-By and Desktop Appraisals

Sometimes, a full-blown inspection just isn't necessary. For lower-risk situations, like certain mortgage renewals or a refinance where the homeowner has a ton of equity, a lender might give the green light for a quicker, more affordable option.

- Drive-By Appraisal: Just like it sounds, the appraiser assesses your property from the street. They'll confirm the house is still standing and get a feel for its exterior condition, but they won't step inside. For all the interior details, they rely on public records and other online data.

- Desktop Appraisal: This is the most remote approach. The appraiser never even visits the property. Instead, they piece together their valuation entirely from their desk, using public records, tax information, and Multiple Listing Service (MLS®) data.

These streamlined options are much faster and cheaper than a full appraisal. But they're only used in specific scenarios where the lender is comfortable with a less detailed level of due diligence.

Understanding the different appraisal types often means getting familiar with concepts like the true market value for property. Every appraisal method is trying to find this number, just with different levels of intensity.

While your lender will ultimately make the final call on which report is needed, it's always a good idea to have your own sense of your property's worth. Getting a free home evaluation beforehand can help make sure your expectations are in line with the current market, so you can walk into the formal appraisal process with confidence.

How to Prepare for a Smooth Home Appraisal

While you can’t wave a magic wand and change your home’s value overnight, a few simple steps can make a world of difference. Preparing for an appraisal isn't like staging for an open house; it’s about making sure the appraiser can do their job efficiently and accurately, reflecting your property’s true worth.

A smooth process isn't just about convenience—it helps support the final valuation. When an appraiser can easily move through every space and has all the key documents at their fingertips, they can build a complete and accurate picture of what your home is really worth.

Create a Home Improvement File

One of the most powerful things you can do is put together a simple package for the appraiser. Think of it as a highlight reel of all the valuable work you’ve poured into your home—details that could directly influence the final number.

Gather these key documents:

- A List of Upgrades: Make a clear, detailed list of all major improvements and renovations. Be sure to include when the work was finished and, if you have the records, how much it cost.

- Key Paperwork: Have your most recent property tax bill handy, along with a copy of your property survey. If you're part of a strata, include those documents and fee details as well.

- Major Replacements: Did you get a new roof in 2022? What about a new high-efficiency furnace last year? List these big-ticket items. They’re proof of your home’s excellent condition and ongoing maintenance.

This file gives the appraiser solid data to work with, making sure no valuable update is accidentally missed.

A well-organized list of upgrades does more than just show off your hard work; it provides the appraiser with verifiable data that can justify a higher valuation. It’s your chance to highlight value that might not be immediately obvious.

Ensure Full Access and a Tidy Space

The appraiser needs to see everything. That means they need clear, unobstructed access to all the rooms, the basement or crawlspace, the attic, and any other structures on the property, like a garage or shed.

A clean, uncluttered home helps them get a better look at important features like walls, floors, and structural elements. While a few cosmetic scuffs won't tank your appraisal, a tidy space just makes a better impression and helps the inspection go much more smoothly. Taking a few minutes to fix small things, like a leaky faucet or a sticky doorknob, also shows pride of ownership.

For anyone who owns an investment property, keeping it in top shape is a core part of effective property management. This kind of preparation is key to cementing your asset’s value, whether you're refinancing or getting ready to sell. At the end of the day, a seamless appraisal is a cornerstone of any successful real estate transaction.

Your Top Questions About BC Appraisal Costs, Answered

When you're navigating a real estate deal, the appraisal can feel like a bit of a mystery, especially when it comes to the cost. It's a critical step, but one that often brings up a lot of questions. We get it.

To help clear things up, we've put together straightforward answers to the most common queries we hear from buyers and sellers right here in Vancouver and the Fraser Valley. Let's tackle them one by one so you can move forward with total confidence.

Who Is Responsible for Paying the Appraisal Fee?

This is easily the most common question we get asked. In almost every single real estate transaction, the borrower pays for the appraisal. If you're buying a home, this fee is usually paid upfront when you apply for your mortgage. Your lender or broker will then order the report on your behalf from a licensed appraiser.

Even though you're footing the bill, the appraisal is technically for the lender. It’s their way of making sure the property is actually worth the amount they’re lending you. Think of it as an insurance policy for their investment, with the cost passed on to you as part of your closing expenses.

How Long Does a Home Appraisal Take in BC?

The whole process breaks down into two parts: the visit to the property and the work that happens back at the office.

- The On-Site Inspection: This is when the appraiser physically comes to the home to measure, take photos, and assess its condition. For a typical house in Maple Ridge, this visit usually takes somewhere between 30 to 60 minutes.

- The Report Completion: After leaving the property, the real work begins. The appraiser has to dig into market data, find recent comparable sales, and compile all that information into a detailed report. This behind-the-scenes analysis is the most time-consuming part.

From the moment you pay the fee to the time the final report lands in your lender's inbox, you can generally expect the process to take about a week. Of course, this can change depending on how busy appraisers are or if your property is particularly unique.

Can I Choose My Own Appraiser?

The short answer is no, not usually. When the appraisal is needed for mortgage financing, the lender has to be the one to order it. They work with a list of approved, third-party appraisal firms to ensure there's no funny business.

This rule is in place for a really important reason: to protect the integrity of the valuation.

An appraiser’s job is to provide a completely unbiased, objective opinion of a property's value. If a buyer or seller could choose their own appraiser, it could create a conflict of interest. Lenders manage the process to keep it independent.

So while you can't hand-pick your appraiser, you can rest assured that they will be a licensed professional in good standing with groups like the Appraisal Institute of Canada (AIC).

What Happens If the Appraisal Comes in Low?

A low appraisal—when the valuation comes in under your agreed-upon purchase price—can feel like a major setback, but it doesn't have to be a deal-breaker. In a competitive market like Vancouver, this situation isn't uncommon, and you have a few ways to handle it:

- The Buyer Covers the Difference: The simplest solution is for the buyer to make up the shortfall with cash at closing. For instance, if you agreed to pay $800,000 but the appraisal is only $780,000, the lender will only finance the lower amount. You'd need to come up with an extra $20,000 out of pocket.

- The Seller Lowers the Price: To save the deal, a motivated seller might agree to drop the sale price to match the appraised value.

- Meet in the Middle: Often, a compromise is the best path forward. The seller might reduce the price a bit, and the buyer brings a little more cash to the table.

- Challenge the Appraisal: This is a long shot, but if you have solid evidence that the appraiser made a factual error or overlooked key comparable sales, you can request a "reconsideration of value."

It's smart to understand how a potential shortfall could affect your budget. A great tool for this is a mortgage payment calculator, which can help you model different scenarios and see how changes to the purchase price or down payment impact your monthly costs.

For anyone buying their first place, the appraisal fee is just one piece of the puzzle. To see how it fits into the bigger financial picture, check out this excellent guide to first-time home buyer closing costs. A little planning goes a long way in making sure there are no surprises on closing day.

At Royal LePage Brookside Realty, we're committed to providing the local expertise you need to navigate every aspect of your real estate transaction in Maple Ridge and the Fraser Valley. If you have more questions or need guidance on buying or selling your home, visit us at https://www.brookside-pm.ca.