Facing foreclosure is an overwhelming and deeply personal experience, but understanding the foreclosure process in BC is the absolute first step toward finding your footing. This isn’t a single, sudden event. It's a structured legal journey that kicks off when mortgage payments are missed, a situation that's become a growing concern in high-pressure markets like Vancouver and the Fraser Valley.

This guide will break down exactly how it unfolds, why it happens, and who the key players are.

The Reality of Foreclosure in British Columbia

The thought of losing your home can feel incredibly isolating, yet it's a reality confronting more British Columbians than you might think. Life happens. An unexpected job loss, a sudden illness, or major economic shifts can quickly turn manageable mortgage payments into an impossible burden.

The province's super-charged real estate landscape, especially in places like Metro Vancouver and the Fraser Valley, is particularly sensitive to these pressures. Recent economic trends have thrown fuel on the fire. The sharp, aggressive rise in interest rates since 2022 has put an immense strain on household budgets, causing what was once a comfortable monthly payment to swell into a source of serious financial stress.

This isn't just a feeling; the data tells a sobering story. A recent Equifax Canada credit trends report highlighted a significant national increase in mortgage delinquency rates. In British Columbia, the rate jumped by 62% year-over-year in the last quarter of 2023. As reported by news outlets like the Vancouver Sun, this surge puts BC among the provinces hardest hit by financial strain, underscoring the severe distress many homeowners are facing.

Key Players in the Foreclosure Process

Navigating the foreclosure landscape means knowing who you're dealing with. Getting a handle on each party's role will help you anticipate what comes next and make more informed decisions. You’ll be interacting with a few key individuals and institutions along the way.

- The Lender (Petitioner): This is the bank or financial institution that holds your mortgage. When payments fall behind, they're the ones who kick off the legal action by filing a petition with the Supreme Court of British Columbia. In all the court documents, they'll be called the "petitioner."

- The Homeowner (Respondent): As the owner of the property, you are the "respondent" in the legal proceedings. You have specific rights and responsibilities throughout this process, which we'll break down in detail later in this guide.

- The Court: Here in BC, foreclosures are a judicial process overseen by the Supreme Court. A judge makes all the final calls, from setting the timeframe you have to repay the debt (the redemption period) to approving the final sale of your home.

- The Real Estate Agent: Once the court orders the property to be sold, a real estate agent is chosen to list it and market it. Their job is to get the home sold and prove to the court that they have achieved fair market value for the property.

It's absolutely crucial to have an expert in your corner who understands the specific nuances of a court-ordered sale. A specialist can ensure your interests are protected and help you get the best possible outcome, even in a tough situation.

Why an Experienced Real Estate Agent Matters

Choosing the right real estate professional is absolutely vital when you're navigating a court-ordered sale. Experts like James and Nicole Isherwood specialize in these complex, high-stakes situations. Their experience goes far beyond a typical transaction; they understand the legal framework, the court's expectations, and how to effectively market a property under these unique conditions in the Vancouver and Fraser Valley areas.

They also bring much-needed clarity on things like commission structures. In a court-ordered sale, the commission is approved by the judge and is typically structured as 7% on the first $100,000.00 and 3.5% on the balance of the sale price. Understanding these costs upfront is important for homeowners. James and Nicole Isherwood work to make sure the process is as transparent and favourable as it can possibly be.

For more real estate insights, you can check out the latest news and updates from our team.

Navigating the BC Foreclosure Legal System

The foreclosure process in BC isn’t some quick, overnight event. It's a formal journey through the Supreme Court of British Columbia, designed with specific legal stages and timelines. It can feel intimidating, but understanding how it all works is the key to knowing your rights and options at every turn.

Things get official when the lender decides it's time to take legal action.

It all starts with a Demand Letter. This isn't a friendly reminder; it's a formal notice from the lender's lawyer stating that you're in default of your mortgage. The letter will lay out the exact amount you owe—including all the missed payments, interest, and penalties—and give you a firm deadline to pay up. Think of it as the final warning shot before the court gets involved.

If you can't pay the amount by the deadline, the lender’s next move is to file a Petition for Foreclosure with the court. This is the document that officially kicks off the legal proceedings. Once you’re served with this petition, the clock starts ticking, and you have a limited time to file a response.

The First Critical Court Date and the Order Nisi

After the petition is filed, things move to the first major court appearance. At this hearing, the lender is there for one main reason: to ask the judge for something called an Order Nisi. This is a massive moment in the foreclosure process.

The Order Nisi does a few key things all at once:

- Confirms the Debt: The court officially validates the total amount of money the lender says you owe.

- Sets the Redemption Period: The judge sets a specific timeframe, known as the redemption period, which is your window to pay off the entire mortgage debt and stop the foreclosure cold.

- Grants Judgment: The lender is granted a formal judgment against you for the full debt amount.

That redemption period is your most important opportunity. By default, it’s usually six months, but a judge can make it shorter or longer. It often comes down to the amount of equity you have in your home. If you have a lot of equity, the judge might grant a longer period. If there’s very little, it could be shortened significantly.

When the Redemption Period Expires

If you're unable to pay off the entire mortgage before the redemption period ends, the process moves into its next phase. The lender goes back to court, this time to request an Order for Conduct of Sale.

This court order is exactly what it sounds like. It gives the lender the green light to list your property for sale on the open market.

This is where having an experienced real estate professional becomes absolutely critical. The court needs to be sure the property is being marketed properly to get a fair price. Experts like James and Nicole Isherwood are invaluable at this stage, as they specialize in the specific marketing strategies and requirements that come with a court-ordered sale in the Vancouver and Fraser Valley markets.

An Order for Conduct of Sale marks a fundamental shift. The focus moves from just repaying a debt to actively selling the home. The court’s priority is now ensuring the sale process is fair and transparent for everyone involved.

It's also worth looking at the bigger picture. While recent interest rate hikes have everyone on edge, the mortgage delinquency rate in major BC markets has been historically resilient. Data from CMHC shows that in places like Vancouver, delinquency rates stayed relatively low for years, partly thanks to stricter mortgage qualification rules. However, the recent economic climate has shifted this stability, leading to the pressures many homeowners feel today. You can get more details in past editions of the CMHC housing market insights report.

Below is a quick summary of the key legal milestones you'll encounter.

Key Stages of the BC Foreclosure Legal Process

This table breaks down the critical legal steps in a typical BC foreclosure, giving you a clear look at the purpose and potential outcome of each stage.

Understanding these stages is the foundation for navigating this challenge. Knowing what to expect allows you to be proactive instead of reactive. For more real estate insights and resources, you can always explore our property management blog.

Understanding a Court-Ordered Sale

When a property in BC enters foreclosure, the selling process gets turned on its head. It’s no longer a straightforward deal between a buyer and a seller. Instead, it becomes a court-ordered sale—a completely different arena with its own set of rules, players, and pressures. This is especially true in competitive markets like Vancouver and the Fraser Valley, where every single step is closely watched by the legal system.

The whole point of a court-ordered sale is to make sure the lender gets the money they're owed, while also protecting the homeowner by selling the property for a fair market price. It’s not just about selling a house; it’s a legally supervised process where a judge has the final say on everything.

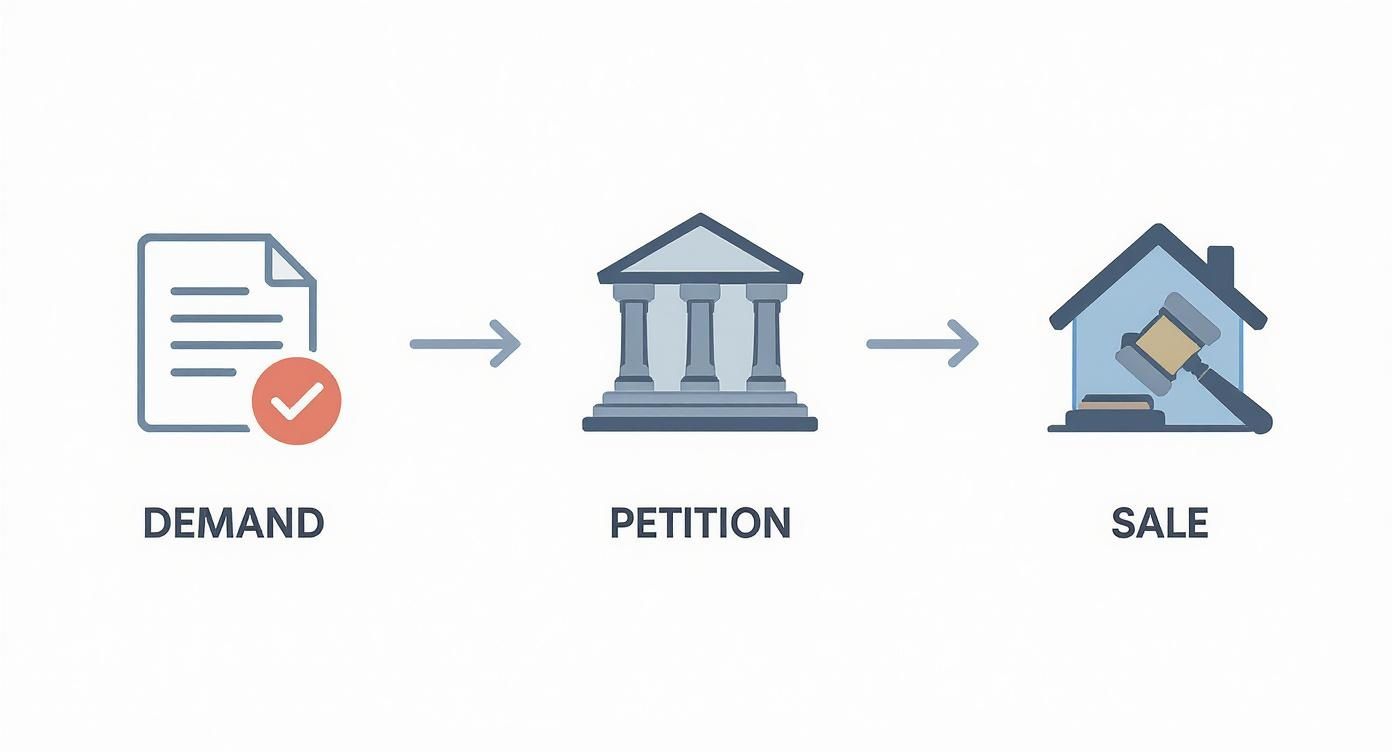

This infographic breaks down the typical foreclosure journey, from the first demand letter all the way to the final court-supervised sale.

As you can see, each step pulls the homeowner deeper into the legal system, eventually leading to the court taking direct control of the sale itself.

The Real Estate Agent's Crucial Role

In a normal sale, a real estate agent’s main duty is to the seller. In a court-ordered sale, that role expands in a big way. The agent, who gets appointed under what’s called an Order for Conduct of Sale, has to prove to the Supreme Court of British Columbia that they’ve done everything possible to market the property and attract the highest price.

This means doing a lot more than just listing the home on MLS®. An experienced agent, like James or Nicole Isherwood, will put together a comprehensive marketing strategy that includes professional photography, virtual tours, and targeted advertising. Crucially, they have to document every single part of this process—every showing, every inquiry, every offer—to present as hard evidence to the court.

The real estate agent’s report to the court is a critical document. It provides the judge with the proof needed to confirm that fair market value has been pursued, which is essential for protecting both the lender and the homeowner’s equity.

The Unique Offer Process

This is where things get really different. When you submit an offer on a court-ordered sale, it has to be completely free of any subjects, with one critical exception: 'subject to court approval'. This means that even if the seller (the homeowner) accepts an offer, it’s not a done deal. Not even close.

The accepted offer is then scheduled to be presented in court on a specific date. At that hearing, any other potential buyers who submitted an offer, or even brand-new buyers who just showed up, can present their own offers directly to the judge. It can turn into a sealed-bid auction right there in the courtroom. The judge will review every offer on the table and approve the one they feel is best—which is almost always the highest price.

For homeowners, this can be a nerve-wracking process, but it can also work in their favour. The competitive courtroom environment can drive the price up, which increases the chances of paying off the mortgage debt and maybe even walking away with some surplus funds. For anyone looking at selling their home under these tough circumstances, understanding how this works is absolutely key.

Understanding the Commission Structure

In a court-ordered sale, the real estate commission isn't just something the seller and agent negotiate. It has to be approved by the court as a reasonable expense of the sale.

The typical commission structure that is generally approved by the court here in British Columbia is 7% on the first $100,000.00 and 3.5% on the balance of the sale price. This standardized rate helps ensure fairness and transparency in a process that’s being overseen by a judge. Knowing this structure helps homeowners anticipate the costs involved and understand how the final proceeds will be split up.

Expert Guidance is Non-Negotiable

Trying to navigate a court-ordered sale on your own is something you should never do. The legal complexities and the financial stakes are just too high.

Real estate professionals like James and Nicole Isherwood specialize in these types of transactions. Their expertise is absolutely crucial for making sure the marketing plan meets the court's strict requirements, that offers are handled correctly, and that your financial interests are protected every step of the way. They bring the calm, experienced guidance needed to manage this high-stakes process and work towards the best possible financial outcome for you and your family.

Finding Alternatives to Foreclosure

Getting a demand letter or a foreclosure petition can feel like hitting a wall. It's a gut-wrenching moment, but it’s absolutely critical to understand that this is not the end of the road. Losing your home is not a foregone conclusion.

You have options. Taking proactive, decisive steps right now can completely change the outcome. The key is to act fast, before the legal process gains too much momentum and your choices start to narrow. Exploring the alternatives gives you a chance to get back in control, protect your credit, and find a resolution that works for you, not the court.

Communicating with Your Lender

Your very first move should be to get on the phone with your lender. It might feel intimidating, but remember this: banks and other financial institutions are in the business of lending money, not owning real estate. Foreclosure is a messy, expensive, and time-consuming headache for them, too.

In many cases, lenders are surprisingly willing to work with you if you're upfront and get in touch early. Two of the most common solutions they can offer are:

- Forbearance Agreement: This is a temporary pause. Your lender agrees to reduce or suspend your mortgage payments for a set period, giving you the breathing room to get back on your feet after a short-term financial hit, like a job loss or medical emergency.

- Loan Modification: If your financial situation has changed more permanently, your lender might agree to change the original terms of your mortgage. This could mean extending the loan's amortization period to drop your monthly payments or adjusting the interest rate.

Before you make that call, do your homework. Get a clear handle on your numbers so you can have a productive, realistic conversation. Using a tool like a mortgage payment calculator will help you figure out what you can actually afford moving forward.

Selling the Property on Your Own Terms

If a loan modification isn't in the cards, your most powerful alternative is to sell your home yourself—before the court orders it sold. This single move puts you right back in the driver's seat. A huge part of protecting your financial future is knowing how to sell your house before foreclosure on your own terms.

Selling proactively gives you several massive advantages over a court-ordered sale.

By selling on your own terms, you control the timeline, the marketing strategy, and the final sale price. This often results in retaining significantly more of your home's equity compared to the court process, where legal and administrative fees can quickly add up.

Working with a real estate agent who understands the urgency and nuances of this situation is non-negotiable. An expert like James or Nicole Isherwood can build a strategic plan to market your property quickly and effectively in the Vancouver or Fraser Valley market. Their goal isn't just to sell; it's to secure a price that pays off the mortgage and maximizes the equity you walk away with.

Keep in mind, in a court-ordered sale, the commission is typically set at 7% on the first $100,000.00 and 3.5% on the balance. In a private sale, you have far more control and flexibility to negotiate these terms.

This proactive approach is especially relevant in BC's current market. We're seeing a noticeable increase in mortgage defaults and foreclosure filings, particularly in urban centres like Greater Vancouver. High property values combined with rising interest rates have put a serious financial squeeze on many homeowners.

Taking control through a private sale lets you close this chapter with dignity and financial stability, giving you the power to move on to the next one.

Knowing Your Rights and Responsibilities

Even when you're deep in the foreclosure process in BC, it’s vital to remember that you still have legal rights that must be respected. The court system is designed to protect both the lender's financial interests and your rights as a homeowner. Understanding that balance is the key to making informed decisions and protecting your equity.

This isn't a one-way street; you have clear entitlements and specific obligations. Knowing where you stand legally empowers you to act, rather than just react, as the proceedings unfold in Vancouver, the Fraser Valley, or anywhere else in the province.

Your Fundamental Rights as a Homeowner

First and foremost, you have the right to participate in the legal process. This starts with your right to respond to the foreclosure petition and carries through every court appearance. Ignoring legal notices is like surrendering your ability to influence the outcome.

Here are some of your key rights:

- The Right to the Redemption Period: Established by the Order Nisi, this is your legal window to pay the entire outstanding mortgage debt and stop the foreclosure cold. This period, which is typically six months, is a cornerstone of homeowner protection in BC.

- The Right to Surplus Funds: If your home sells for more than the total amount owed (including the mortgage, legal fees, and commissions), that leftover money is legally yours. The court ensures all debts are paid before releasing these surplus proceeds to you.

- The Right to a Fair Sale Price: The court supervises the sale to ensure the property is marketed properly to achieve fair market value. This protects any equity you have in the home and prevents the lender from accepting an unreasonably low offer.

Your Obligations During Foreclosure

Along with your rights, you also have responsibilities that you must meet. Failing to uphold these can negatively impact how the court views your situation and could harm your financial outcome. Your main duties are to maintain the property and cooperate with the sale process.

It is crucial to maintain the home’s condition. Any damage or neglect can lower the property's value, reducing the potential for surplus funds and possibly leading to further legal action.

You are also required to provide access for showings once an Order for Conduct of Sale is granted. This cooperation is essential for the real estate agent to market the property effectively.

Protecting Yourself and Your Equity

Protecting your interests requires proactive engagement. Responding promptly to all legal notices is your first line of defence. For homeowners actively seeking to intervene, a comprehensive guide for homeowners on stopping the foreclosure process can provide actionable steps and strategies.

Most importantly, you need expert guidance. A lawyer specializing in foreclosure can explain your legal standing, while a real estate professional experienced in court-ordered sales can ensure your financial interests are protected.

Experts like James and Nicole Isherwood are indispensable here. They understand the court's expectations regarding marketing, fair value, and the standard commission structure (7% on the first $100,000.00 and 3.5% on the balance). Their guidance helps maximize your home's sale price, preserving as much of your hard-earned equity as possible.

Common Questions About BC Foreclosures

When you're facing foreclosure, the questions come fast and heavy. It's a confusing process, run through the Supreme Court of British Columbia, and it can feel overwhelming whether you're a homeowner trying to save your property or an investor looking for an opportunity. Let's cut through the noise and get you some clear, straightforward answers about how foreclosure works in BC, especially in the busy Vancouver and Fraser Valley markets.

How Long Does the Foreclosure Process Take in BC?

There’s no hard-and-fast timeline for a foreclosure in British Columbia; it's definitely not a quick process. The actual duration really hinges on a few key things: the court's own schedule, how you as the homeowner respond to the legal filings, and how fast a solid offer on the property comes in and gets approved.

As a general rule, you can expect the whole thing to take anywhere from six months to over a year. A critical part of this timeline is the redemption period, which is typically set at six months from the start. However, a judge has the final say and can shorten or extend that window based on the specifics of your case, like how much equity you have in your home.

Can I Stop a Foreclosure Once It Has Started?

Yes, you absolutely can stop a foreclosure, but your options start to narrow the longer you wait. The clearest path is to "redeem the mortgage" before that redemption period is up. This means paying off the entire outstanding balance—principal, interest, legal fees, and any other costs the lender has racked up.

If coming up with that much cash isn't realistic, you still have some very real alternatives:

- Work out a new payment plan with your lender. This is often called a forbearance agreement and can give you the breathing room you need.

- Refinance your mortgage with a different lender, assuming your financial picture has improved enough to qualify.

- Sell the property yourself on your own terms before the court steps in and orders a sale.

The single biggest advantage you have is acting quickly. The earlier you start exploring these options, the more control you'll have over the final outcome.

The most powerful tool a homeowner has is proactive engagement. By taking decisive action early, you can often find a path that avoids the finality of a court-ordered sale and protects your financial future.

What Happens If the Property Sells for More Than I Owe?

This is one of the most important things for homeowners to understand. If the property's final sale price is higher than the total debt you owe the lender (plus all the associated costs), that leftover money—known as surplus proceeds—is legally yours.

The funds are held by the court for a bit while it makes sure all the secured creditors, lawyers, and real estate salespeople have been paid. Once every bill is settled, the remaining surplus is released directly to you.

This is exactly why having an expert real estate salesperson in your corner is so critical. Professionals like James and Nicole Isherwood focus on marketing the property to get the highest possible price, which directly boosts the chances—and the amount—of any surplus funds you might get back.

What Are the Risks of Buying a Foreclosed Property?

Buying a court-ordered sale can be a great way to find value, but it comes with some significant and unique risks that you just don’t see in a normal real estate deal. You absolutely have to go into it with your eyes wide open.

Here are the main risks to be aware of:

- "As Is, Where Is" Condition: The property is sold exactly as it stands, with zero warranties. If you discover a leaky roof or a cracked foundation after the sale is final, you have no legal comeback against the seller or the court.

- Court Approval Uncertainty: Even if your offer is accepted by the lender, it’s not a sure thing. The deal isn't final until a judge approves it, and they can always reject your offer if a better one shows up at the court hearing.

- Potential for Occupants: Sometimes the previous owner is still living in the property after you take possession. If that happens, you become responsible for the legal eviction process, which can be both time-consuming and costly.

Navigating the complexities of real estate in the Fraser Valley requires experience and local knowledge. At Royal LePage Brookside Realty Property Management, James and Nicole Isherwood provide expert guidance for buying, selling, or managing your property. Contact us today to discuss your real estate goals.