Buying a condo is a huge financial step, one that actually begins long before you ever step foot in an open house. It all starts with taking a good, hard look at your finances, getting a mortgage pre-approval locked in, and truly understanding the full range of costs you're facing—from the down payment to taxes and closing fees specific to British Columbia.

Building Your Financial Foundation

Before you even think about scrolling through listings in Vancouver or the Fraser Valley, your first real move is to get your financial house in order. This isn't just about figuring out what you can afford; it's about positioning yourself as a serious, credible buyer in a market that moves incredibly fast. It’s the difference between being a window shopper and a prepared buyer ready to make a move.

The single most powerful tool you have at this stage is a mortgage pre-approval. This is a world away from a simple "pre-qualification," which is little more than a ballpark guess. A real pre-approval means a lender has dug into your finances—your income, debts, and credit history—to commit to a specific loan amount.

Why Pre-Approval Is Your Golden Ticket

In hot markets like Vancouver or Langley, walking in without a pre-approval letter is a non-starter. It’s the proof sellers need that you have the financial muscle to see the deal through. When you’re up against multiple offers, that letter can easily be the thing that pushes your offer to the top of the pile.

Before you even chat with a lender, do a little homework on your own. It's smart to pull your credit reports from Equifax Canada and TransUnion Canada to make sure everything is accurate. A healthy credit score isn't just about getting approved; it's about unlocking better interest rates that can save you a fortune over the life of your mortgage.

A mortgage pre-approval is your budget set in stone. It prevents the disappointment of falling for a property that's financially out of reach and gives you the confidence to act quickly when you find the right condo.

Calculating Your Down Payment And Initial Costs

Your down payment is the first big chunk of cash you'll need. In Canada, the minimum amount is tied to the purchase price:

- For the first $500,000: You need at least 5%.

- For the portion above $500,000 up to $999,999: You need 10%.

- For homes $1 million and over: A 20% down payment is mandatory.

If your down payment is less than 20%, you'll also have to pay for mortgage loan insurance (like CMHC insurance). This protects your lender in case you default on payments. While it's an added cost—which you can pay upfront or roll into your mortgage—it’s also what allows many people to get into the BC market much sooner.

To get a clearer picture of what your monthly payments might look like with different down payment amounts, you can use a helpful mortgage payment calculator to run various scenarios.

Your Upfront Condo Purchase Budget

Beyond your down payment, a handful of other costs pop up around closing time. To help you plan, here’s a quick checklist of the key expenses you'll need to budget for when buying a condo in the Lower Mainland.

Having a clear picture of these numbers ensures there are no last-minute financial shocks, letting you start your condo search with total confidence.

Finding the Right Condo for You

With your financing sorted, you’re ready for the fun part—the actual hunt for your new home. It’s easy to get swept up in beautiful online listings, but a little strategy here will save you a ton of time and keep the overwhelm at bay. This is especially true in the fast-moving real estate markets of Vancouver and the Fraser Valley.

Before you start scrolling, you need to get crystal clear on your priorities. Think bigger than just the number of bedrooms and bathrooms; consider how a property will actually fit into your day-to-day life. The key is separating your absolute must-haves from your nice-to-haves.

Defining Your Lifestyle Needs

A simple checklist can be your best friend here, guiding your search and keeping you focused. This isn’t just about the four walls of your unit, but the community and building you'll be calling home.

- Commute Time: What’s your realistic limit for getting to work? Think about how close you need to be to major routes like Highway 1 or SkyTrain stations in hubs like Coquitlam or Surrey.

- Neighbourhood Vibe: Are you picturing the vibrant, walkable streets of Vancouver's Mount Pleasant, or does the quieter, family-friendly atmosphere of Port Moody appeal more? Spend a weekend just walking around potential neighbourhoods to feel them out.

- Building Amenities: Is a gym, common room, or rooftop patio a deal-breaker? Just remember, more bells and whistles usually translate to higher monthly strata fees.

- Future Growth: It pays to look into municipal development plans. Is a new community centre or transit line in the works for the area? This could have a huge impact on your future property value and quality of life.

The Value of a Strata-Savvy Realtor

Working with a real estate agent is a must, but when you're buying a condo, not just any agent will cut it. You need a specialist—someone who lives and breathes strata properties in BC. These experts understand the ins and outs of strata corporations, can spot red flags in documents from a mile away, and know exactly what to ask about a building's history and financial health.

An experienced local agent brings insights you simply can't find online. They know which developers have solid reputations in the Lower Mainland, which buildings might be facing hefty assessments, and the subtle differences between neighbourhoods that can make or break your living experience. For a deeper dive, check out our guide on what to expect when buying a home.

A great real estate agent is your advocate and your detective. Their expertise in strata-titled properties is your best defence against buying into a building with hidden problems or a dysfunctional strata council.

It's also smart to get a handle on the bigger picture. Knowing how to analyze market trends helps you figure out if you're in a buyer's or seller's market, which is crucial for shaping your search and offer strategy.

Reading the Market and Listings

The market is always in motion, so staying informed is vital. According to the Real Estate Board of Greater Vancouver (REBGV), residential sales in the region in April 2024 were 12.5% below the 10-year seasonal average, indicating a slight cooling. However, the number of listed properties was up 42.1% from April 2023, giving buyers more selection.

When you're browsing listings, train your eye to look past the professionally staged photos. Zero in on the details: monthly strata fees, property taxes, and any listed restrictions (like pet or rental bylaws). A surprisingly low strata fee in an older building can be a major red flag—it might mean the contingency reserve fund is dangerously underfunded. Likewise, if you notice high agent turnover in one building, it could signal underlying issues.

This is where your agent becomes invaluable. They can help you read between the lines and figure out which properties are actually worth seeing in person.

Crafting a Winning Offer

You’ve toured the properties, weighed the pros and cons, and finally walked into a condo that just feels right. This is the moment the search gets real, turning your browsing into a concrete plan of action. It's time to put together a compelling offer—one that grabs the seller’s attention while keeping your own interests protected.

This isn’t just about picking a price. It’s about building a formal, strategic proposal. Here in British Columbia, we do this using a Contract of Purchase and Sale. This is a legally binding document that lays out every single detail of the deal, from the deposit amount to the critical deadlines both you and the seller have to meet.

Understanding the Key Parts of Your Offer

Think of the Contract of Purchase and Sale as the blueprint for your purchase. Getting familiar with its main components is crucial because each one shapes the deal and provides you with essential safeguards. Your real estate agent is there to guide you, of course, but knowing the language keeps you in the driver's seat.

Here’s what you’ll be looking at:

- Purchase Price: The straightforward dollar amount you’re offering for the condo.

- Deposit: This is your "good faith" money, typically 5% of the purchase price in BC. It’s held in a trust account and gets applied toward your down payment when the sale completes.

- Dates: The contract is built around a timeline. It will clearly state the offer acceptance date, the subject removal date, the completion date (when ownership legally transfers to you), and the possession date (when you get the keys!).

- Subjects (Conditions): These are your escape hatches. They are clauses that must be satisfied for the sale to become firm, giving you a way out if you uncover something unexpected.

An offer is a delicate balance. It needs to be attractive enough to catch the seller's attention, especially in a competitive market, but also structured with protective conditions that allow you to do your homework thoroughly.

Deciding on the Right Offer Price

Figuring out what to offer is part art, part science. It’s not just about what your pre-approval says you can afford; it’s about what the property is actually worth in today's market. Your agent will pull "comps"—hard data on what similar condos in the building or neighbourhood have sold for recently. This gives you a solid, evidence-based starting point.

The conditions in the Metro Vancouver market play a massive role. For instance, recent REBGV data from April 2024 shows the benchmark price for an apartment home hit $779,700. That figure reflects a 2.6% increase from April 2023, which tells us the condo market remains resilient. Knowing these trends helps you frame a realistic and competitive offer.

Don't forget to factor in the condo's unique qualities. Has the kitchen been beautifully renovated? Does it have a rare, oversized patio that no one else has? Features like these can justify a higher price. On the flip side, if the unit needs a lot of work or has a quirky layout, you might have some wiggle room to negotiate downward. Getting a sense of the seller's mindset, which you can learn about by understanding the nuances of selling your home, can also provide a strategic advantage.

The Power of Subjects: Your Safety Net

Subjects, or conditions, are your single most important tool for self-protection when buying a condo. They give you a defined period—usually seven to ten days—to perform your due diligence. If any of your conditions aren't met to your complete satisfaction, you can walk away from the deal with your deposit fully refunded. No questions asked.

For any condo purchase in BC, these three subjects are absolutely non-negotiable:

- Financing: This gives your lender the time they need to review all the property and strata documents and give you their final, unconditional mortgage approval.

- Inspection: A professional home inspector will go through the unit with a fine-tooth comb, looking for any potential issues from faulty wiring to hidden signs of water damage.

- Strata Document Review: This is the big one for strata properties and is absolutely vital. You'll receive a thick package of documents—meeting minutes, financial statements, engineering reports, and more—that reveals the true health of the building and its management.

Even when you find yourself in a bidding war, where the temptation to submit a "subject-free" offer is immense, it's a huge risk. Imagine finding out about a surprise multi-million dollar special levy after your offer is firm and you can't back out. The financial fallout can be devastating. A smart, well-advised buyer always keeps their subjects in place to ensure they're making a sound investment.

Decoding Strata Documents and Inspections

Your offer’s been accepted. This is the moment you’ve been waiting for, but hold off on popping the champagne just yet. Now the real detective work begins.

This is the subject removal period, often called due diligence. It's your window of opportunity to look under the hood of both the physical unit and the strata corporation you're about to join. For a condo, this breaks down into two critical investigations: a professional home inspection and a deep, thorough review of the strata documents. This is your chance to uncover the true health of the building and make absolutely sure you're making a sound investment.

The Professional Home Inspection

You might have a keen eye for scuff marks on the floor or a dated light fixture, but a professional home inspector brings a trained perspective to uncover problems you’d likely never spot. Their job is to methodically assess all the systems inside your unit—we’re talking about the electrical panel, plumbing fixtures, heating systems, and every single appliance.

They also examine common property elements that directly affect your unit. This could mean checking for subtle signs of water ingress around the windows, evaluating the condition of the balcony membrane, or looking for any visible structural issues. It’s an essential step to ensure the space you'll be personally responsible for is in solid shape from day one.

Diving Into the Strata Document Treasure Trove

This is, without a doubt, the most critical part of buying a condo in BC. You'll receive a hefty package of documents from the seller that essentially tells the entire story of the building's financial, physical, and even social health. Trust me, reading these documents is non-negotiable.

Here are the key documents you need to focus on and what to look for in each one:

- Form B (Information Certificate): This is a real-time snapshot of the unit in BC. It confirms the current monthly strata fees, shows if the owner is behind on payments, details the unit's share of the contingency fund, and discloses any pending lawsuits against the strata.

- Strata Meeting Minutes (AGM & Council): You need to read at least two years' worth of these. Look for recurring complaints about things like water leaks, elevator breakdowns, security issues, or heated disputes between owners. These notes reveal the day-to-day reality of living in the building.

- Financial Statements & Budget: These show you exactly where the money comes from and where it goes. You want to compare the proposed budget to the actual spending. Consistent deficits or a history of special levies are major red flags that could point to poor financial management.

- Bylaws and Rules: This is the community rulebook. Pay very close attention to any restrictions on pets, rentals, renovations, and even smaller things like BBQ usage or flooring types. You have to make sure these rules align with your lifestyle before you're locked in.

Think of the strata documents as the building's official biography. The story they tell—of proactive maintenance and fiscal responsibility, or of neglect and constant conflict—is the best indicator of your future experience as an owner.

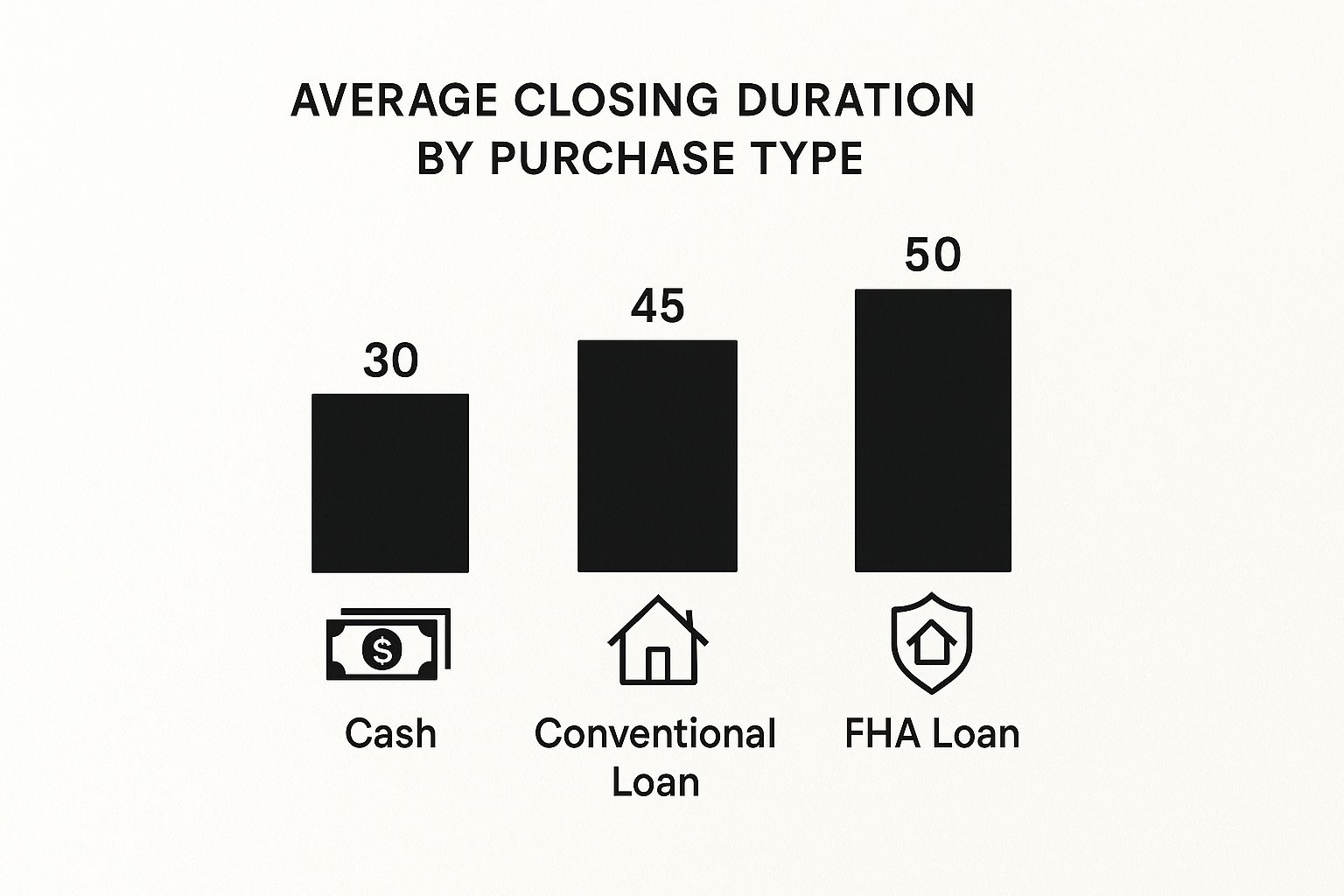

The image below gives you a sense of a typical closing timeline, which kicks off right after you've done your due diligence and removed subjects.

As you can see, transactions with financing take a bit longer to finalize. This really highlights why it’s so important to have all your ducks in a row—especially the strata review—well before your closing date.

Assessing the Building’s Long-Term Health

Beyond the day-to-day, you need to get a clear picture of the building's long-term plan. For this, two documents are absolutely essential: the depreciation report and the state of the contingency reserve fund (CRF).

The depreciation report is basically a 30-year forecast for major repairs and replacements of common property—think the roof, windows, pipes, and parkade membrane. It estimates when these big-ticket items will need work and what the projected costs will be. This report is your crystal ball, showing you the major expenses coming down the pipeline.

This ties directly into the contingency reserve fund (CRF), which is the strata's savings account for tackling those big projects. A healthy CRF is vital. A low fund paired with a depreciation report full of upcoming expenses is a recipe for a special levy—a large, one-time cash call that all owners have to pay.

As of November 2023, a significant regulatory change in BC now requires strata corporations to contribute a minimum of 10% of their annual operating budget to the CRF each year. This change is designed to prevent stratas from falling behind on their savings.

It's completely normal to find these documents overwhelming. If you do, hiring an expert to review them is a wise investment. The complexities of strata governance are why many owners turn to professional help; understanding the nuances of https://www.brookside-pm.ca/property-management can offer a valuable perspective even for a prospective buyer. For more insights on property research, the TitleTrackr real estate and title blog is a great resource.

This diligence ensures you’re not just buying a condo, but investing in a well-run community for years to come.

From Accepted Offer to Getting Your Keys

Once your subjects are removed, you’ve officially crossed the biggest hurdle in the condo buying journey. A huge congratulations is in order! You're now on the home stretch, and the focus shifts from investigation and negotiation to the administrative side of things. This is the closing process, where the legal and financial details get ironed out before the keys finally land in your hands.

The moment your deal becomes firm, your first call should be to a BC lawyer or notary public. This professional is your guide for the final leg of the journey, and their job is to protect your interests by handling all the complex legal work involved in transferring the property from the seller's name to yours.

The Role of Your Legal Team

Behind the scenes, your lawyer or notary gets to work on several critical tasks. They’ll perform a title search to make sure there are no hidden liens or claims against the property, work directly with your mortgage lender to get the funds ready, and prepare the all-important Statement of Adjustments. This document is a detailed financial breakdown of all your final costs.

Here’s a quick look at what your legal representative handles:

- Title Search: This is non-negotiable. They verify the seller has the legal right to sell the condo and that it’s free of any unexpected financial baggage.

- Mortgage Documents: They will review and prepare all the necessary mortgage paperwork for you to sign before your bank releases the funds.

- Transfer of Funds: Think of them as the secure hub for all the money. They manage your down payment, the mortgage funds from the lender, and all closing costs, ensuring everything goes to the right place at the right time.

- Property Registration: This is the final step that makes it official. They register the property and the mortgage in your name with the BC Land Title and Survey Authority.

Preparing for the Final Costs

The Statement of Adjustments will clearly lay out the final amount you need to bring to your lawyer before the completion date. This isn't just your down payment; it also includes all your closing costs. One of the biggest closing costs for anyone buying a condo in BC is the Property Transfer Tax (PTT).

To give you a real-world example, on a property valued at $779,700 (the benchmark condo price in Metro Vancouver as of April 2024), a buyer could face a PTT of $13,594. That’s a significant chunk of change.

Thankfully, there are programs to help. The First Time Home Buyers' Program, for instance, offers a full exemption for eligible buyers on properties with a fair market value up to $500,000, with a partial exemption up to $525,000. Knowing if you qualify is absolutely vital for budgeting accurately.

Your Final Walk-Through

Right before the completion date, you'll have a chance to do one last walk-through of the condo. This isn’t another home inspection. It's simply your opportunity to confirm that the property is in the same condition as when you made your offer.

You'll want to make sure all the agreed-upon inclusions (like appliances, blinds, etc.) are still there and in working order. Flip the light switches, run the faucets, and just make sure everything is as you expect it to be.

The final walk-through is your last chance to flag any issues before the deal is done. If you find a problem—like a big new scratch on the hardwood floor or an appliance that suddenly doesn't work—your REALTOR® can raise the issue with the seller's agent immediately.

Understanding Your Key Dates

In British Columbia, the closing process has two key dates that are often just a day or two apart. It’s crucial to know the difference.

The Completion Date: This is the day the money and title officially change hands. Your lawyer registers you as the new owner at the Land Title Office, and the seller gets paid. On this day, you legally own the condo—but you don’t get the keys just yet.

The Possession Date: This is the day you've been waiting for! Usually set for one or two days after completion, this is when your real estate agent can finally hand you the keys to your new home. You're now free to move in and start your life as a condo owner.

This final phase, while it feels like a lot of paperwork, is actually a very organized and straightforward process. By understanding each step, you can move confidently toward the finish line, ready for that amazing moment when you unlock your own front door for the very first time.

Common Questions About Buying a Condo in BC

Jumping into the BC condo market can feel like learning a new language, especially when you start hearing terms like "strata" and "special levy." To help you navigate it all with a bit more confidence, we've put together answers to the most common questions we get from buyers in Vancouver and the Fraser Valley.

What Is a Special Levy and Should I Worry About It?

Think of a special levy as an unexpected cash call for all owners in a strata building. It happens when a major, expensive repair is needed—like replacing the entire roof or fixing a leaky parkade—and the building’s main savings account (the contingency reserve fund) doesn't have enough cash to cover it.

Now, an upcoming levy isn't an automatic deal-breaker. In fact, it can be a huge bargaining chip. If the strata documents, particularly the depreciation report, show that a big project is on the horizon, that’s a red flag, but it's also leverage. You can often negotiate a lower purchase price because you’ll be the one footing that future bill.

How Much Money Should a Strata's Savings Fund Have?

There's no magic number here. The right amount for a contingency reserve fund (CRF) really depends on the building itself—its age, size, and what it’s made of. An older, sprawling low-rise in Langley is going to need a much bigger financial cushion than a five-year-old concrete tower in Burnaby.

The real test is comparing the money in the bank against the building's future needs. You do this by looking at the CRF balance and then reading the depreciation report, which lists all the major repairs and their estimated costs for the next 30 years. If the fund is low and the report is full of expensive upcoming projects, you can bet a special levy is just around the corner.

The real story is in the details. A well-managed strata will have a reserve fund that aligns with its long-term maintenance needs, ensuring financial stability for all owners.

Can I Renovate My Condo After I Buy It?

For the most part, yes—but you absolutely have to play by the strata's rules. Small cosmetic changes, like painting the walls or swapping out a light fixture, are usually no problem and don't require any permission.

Anything bigger, though, will mean getting formal written approval from the strata council. This is especially true for projects that involve:

- Flooring: Hardwood and laminate can be a major issue due to noise travelling to the unit below.

- Plumbing or Electrical: Any changes to the building's core systems need to be signed off on.

- Structural Changes: Thinking of taking down a wall? That's a definite "ask permission first" situation.

Always, always review the renovation bylaws during your due diligence period. It’s the only way to know for sure what you can and can't do before you commit to buying a condo you’re hoping to make your own. If you're looking for a property with great potential, getting a free home evaluation can provide valuable insight into its current market worth.

Market conditions can also influence your plans, and they vary wildly by area. For instance, the Fraser Valley Real Estate Board reported in April 2024 a benchmark apartment price of $559,700, a 5.7% jump from the previous year. This just goes to show how different the market is from Metro Vancouver and why digging into local data is so important. You can read more on Fraser Valley market statistics.

At Royal LePage Brookside Realty, our team lives and breathes the Fraser Valley market. We know the right questions to ask to make sure you find the perfect property. If you're ready to get started, connect with us today. Visit us at https://www.brookside-pm.ca.